Displaced Palestinians ferry bags of food aid after storming a World Food Program warehouse in Deir el-Balah in the central Gaza Strip on May 28, 2025. The United Nations on May 28 condemned a United States-backed aid system in Gaza following a chaotic food distribution where 47 people were injured, after Israel allowed supplies in at a trickle last week, easing a full blockade imposed on the besieged Palestinian territory for over two months. — Photo by Agence France-Presse

Israel accused the United Nations Wednesday of seeking to “block” Gaza aid distribution, as the global body said it was doing its utmost to gather the limited assistance greenlighted by Israel’s authorities.

The humanitarian situation in Gaza, where Israel has imposed a two-month aid blockade, is dire, with food security experts saying starvation is looming for one in five people.

Article continues after this advertisement

“While the UN spreads panic and makes declarations detached from reality, the state of Israel is steadily facilitating the entry of aid into Gaza,” Israel’s United Nations Ambassador Danny Danon told the Security Council.

He said the assistance was entering by trucks — under limited authorization by Israel at the Kerem Shalom crossing since last week following the blockade — and via a “new distribution mechanism developed in coordination with the US and key international partners.”

Danon was referring to the Gaza Humanitarian Foundation (GHF), a private, US-backed aid group that has established its own distribution system, one the United Nations considers contrary to its humanitarian principles.

A chaotic distribution of aid at a GHF center Tuesday left 47 people wounded.

Article continues after this advertisement

Israel’s ambassador blamed Hamas for the tumult, saying the Palestinian group set up roadblocks and checkpoints to block access to the distribution center.

He accused the UN of “trying to block” the aid.

Article continues after this advertisement

The United Nations “is using threats, intimidation and retaliation against NGOs that choose to participate in the new humanitarian mechanism,” Danon added.

‘Will not participate’

Danon specifically accused the United Nations of having removed these nongovernmental organizations from a database listing groups working in Gaza, an accusation rejected by the UN.

“There are no differences between the current list and the one from before the launch of the GHF,” Stephane Dujarric, spokesman for UN Secretary-General Antonio Guterres, told AFP.

But the UN reiterated its opposition to coordinating with GHF.

“We will not participate in operations that do not meet our humanitarian principles,” insisted Dujarric.

He also said the UN was doing all it could to gather the aid arriving through Kerem Shalom.

Since last week 800 truckloads were approved by Israel but fewer than 500 made it into Gaza, according to Dujarric.

“We and our partners could collect just over 200 of them, limited by insecurity and restricted access,” he said.

“If we’re not able to pick up those goods, I can tell you one thing, it is not for lack of trying.”

Danon had said “more than 400 trucks” full of aid were already on the Gaza side of the crossing and that Israel had provided “safe routes” for the distribution.

“But the UN did not show up,” the Israeli envoy said. “Put your ego aside, pick up the aid and do your job.”

Israeli military operations in Gaza have killed at least 54,804 people, mostly civilians, according to the health ministry there. The UN considers the figures reliable.

The punishing offensive has reduced much of the Palestinian territory to rubble — including hospitals, schools and other basic infrastructure — and resulted in the displacement of almost all of its roughly two million people.

Your subscription could not be saved. Please try again.

Your subscription has been successful.

Israel launched its operations in response to the October 7, 2023, attack by Hamas, which killed 1,218 people, according to an AFP tally based on official figures. /das

This post is part of a series sponsored by IAT Insurance Group.

Motor vehicle crashes cost employers $60 billion annually — some of which are not actually “accidents.”

Staged auto accidents — in which fraudulent actors deliberately orchestrate collisions with commercial vehicles to earn the claims payout — are a significant and growing concern for the commercial transportation industry. These scams are not only costly for fleet carriers but also dangerous for everyone on the road. Fraudulent claims from staged accidents can lead to increased insurance premiums, legal battles and damage to a company’s reputation.

Organized crime rings often orchestrate these scams, targeting commercial trucks due to their high insurance claim payouts. They typically involve multiple participants, including fake witnesses, corrupt medical providers and unethical attorneys who inflate injury claims.

Understanding the common types of staged accidents is crucial for fleet carriers and truck drivers to protect themselves.

The swoop and squat – A vehicle quickly cuts in front of a truck and suddenly slams on the brakes, causing a rear-end collision. The scammer then claims severe injuries, leading to hefty insurance payouts.

The drive down – In this scenario, a fraudster waves a truck forward in a merging or parking lot situation and then intentionally collides with the truck, later denying they ever signaled.

The panic stop – Bad actors fill a vehicle with passengers, pull in front of a truck, and abruptly brake. The passengers all file exaggerated injury claims, increasing the cost of the fraudulent claim.

The sideswipe – Scammers take advantage of lane changes or tight spaces in intersections, ensuring a truck brushes against them. They later exaggerate damages and injuries.

The fake witness setup – A witness suddenly appears, claiming to have seen the accident and placing the blame on the truck driver. Often, these witnesses are accomplices in the scam.

How fleet carriers can protect themselves

Staged accidents can cause severe financial and operational disruptions for fleet carriers. Recognizing red flags and taking the following proactive measures is essential to mitigating risks.

1. Install cameras

Dash cameras and other recording devices provide irrefutable evidence of what actually happened in an accident. Some scammers will deliberately reverse into a truck (sometimes called a “swoop and squat”) to make it appear that the truck rear-ended them. Without a camera, proving innocence is difficult. Cameras expose these frauds by showing the sequence of events clearly. In most cases, video footage makes it obvious who was at fault, stopping fraudulent claims before they start.

2. Train drivers to spot the signs

Driver awareness is crucial in preventing staged accidents. Educating drivers about common scam tactics enables them to recognize red flags before an accident occurs. Some warning signs include:

Erratic or suspicious driving behavior

A vehicle with multiple passengers appearing ready to claim injuries

A bystander who conveniently appears to “witness” the accident and sides with the other driver

Situations where a truck gets deliberately wedged in, making movement difficult

Encourage drivers to trust their instincts. If something feels off, it likely is. Training programs should include real-life case studies and defensive driving techniques to help drivers mitigate risks.

3. Collect data at the scene

One of the hardest things for drivers to do after an accident is to remain calm and document everything. However, collecting data at the scene can make all the difference in disproving fraudulent claims. Key steps include:

Taking multiple photos of the scene, vehicles, license plates and surrounding conditions

Noting any suspicious behavior from the other driver or witnesses

Gathering witness statements from unbiased third parties

Documenting injuries (or lack thereof) with timestamped photos

Recording personal observations and details while they’re fresh

4. Work with law enforcement

If a driver suspects fraud, they should immediately notify the responding officer. Showing dashcam footage on-site can be a game-changer, as it provides indisputable evidence that can prevent false claims. Officers who recognize fraud can document it properly, strengthening the defense against a scam.

5. Communicate with your insurance company

Quick and clear communication with your insurance company is crucial. Fleet managers should provide all available evidence, including:

Dashcam footage

Driver statements

Witness information

Police reports

The sooner insurance companies receive this information, the faster they can begin investigating potential fraud, reducing claim costs and exposure to liability.

6. Document even minor incidents

Not every staged accident involves major damage. Sometimes scammers stage minor accidents, only to later claim severe injuries. A common scenario involves a minor rear-end collision where the other driver appears uninjured but later files a lawsuit claiming chronic back pain. The statute of limitations in many states is two years, meaning fraudulent claims can emerge long after the accident. Documenting even the smallest incidents ensures fleet carriers are prepared to counter false claims when they arise.

7. Follow proper accident reporting protocols

Fleet carriers must have a standardized accident reporting protocol that drivers follow after every incident. Best practices include:

Reporting all accidents immediately

Documenting everything thoroughly

Notifying insurance and legal teams about potential fraud

Retaining records and reports for the long term

If fraud is suspected, alerting insurance companies and investigators early allows for a more thorough investigation, potentially stopping fraudulent claims before they gain traction.

Awareness and defense driving

By leveraging technology, training drivers to recognize scams and maintaining thorough documentation, fleet operators can protect themselves against costly schemes. By staying vigilant and proactive, carriers will safeguard their business from the growing threat of staged accidents.

ASK A LOSS CONTROL REPRESENTATIVE

Have a question on how to mitigate risk? Email [email protected] for a chance to see your question answered in a future blog.

When we think about investing, we usually focus on things like returns, company performance, valuation, past track records, or the reputation of the asset management company. But today, as we witness the growing environmental degradation and climate change, there’s a shift in the mindset of many investors.

More and more individuals are beginning to care just as much about how a company operates as they do about how much it earns, by assessing how companies treat the environment, their employees, and society in general.

That’s why investors are considering investing in green funds, or as they are more commonly known here, ESG funds, as part of their financial planning. These funds are considered a kind of green investment as they focus on companies that act responsibly and follow sustainable business practices.

What Is a Green Fund?

When we talk about green funds, we’re talking about mutual funds that invest primarily in shares of companies that practise environmentally sustainable, socially responsible, and ethically governed business models, such as those involved in renewable energy, electric cars, clean tech, waste management, or companies with strong ESG (Environmental, Social, Governance) ratings.

The term is not commonly used in India, as here such funds are referred to as ESG funds.When fund managers select the stocks to invest in, they assess how companies handle:

The environmental impact of their operations: This includes evaluating factors like their carbon emissions, waste management systems, water conservation, pollution control, and energy efficiency. The higher the company scores in these aspects, the more ‘green’ they are considered. For example, a company manufacturing solar cells and wind turbines would score highly on environmental criteria as they help generate renewable energy. Similarly, a business focusing on electric cars will also be looked at favourably by fund managers.

Their social responsibility: Fund managers score companies on the basis of how they treat their employees, support community welfare, and promote education and healthcare. Other factors like gender equality, labour rights, fair wages, and safe working environments are also closely considered.

Governance standards: This part involves analysing the qualitative aspects of a company, like its leadership structure, how compliant it is with regulations, its transparency in financial reporting, ethical conduct, and how well it protects its shareholders.

How Do Green Funds Work?

Green funds work the same way as any other mutual fund. They are a pooled investment where a professional fund manager invests the corpus in a diversified basket of securities. What sets green funds apart is the way in which this portfolio is selected. Instead of just looking at financial metrics, managers assess companies on the basis of ESG scores.

While there is no set standard for ESG scoring, the general idea is to prioritise companies that align with the many ESG parameters. For individuals, investing in these funds also works the same as other mutual funds. You can buy units with a lump sum or through an sip investment plan if you want to take the regular contribution approach.

Purpose and Objectives of Green Fund

The main goal of a green fund investment is to deliver strong returns by investing in companies that score well on ESG parameters. Since these equity-oriented funds are actively managed, managers aim to outperform benchmarks like the Nifty 100 ESG Index. These are long-term vehicles which not only offer environmentally-conscious individuals the opportunity to invest in a diversified portfolio but are also well-positioned to benefit from the growing awareness around environmental sustainability and ethical business practices.

As more people and companies recognise the importance of environmental protection and honest governance, businesses that align with ESG principles will likely gain a competitive edge.

Since equity means ownership, the more socially aware investors these days try to prioritise and support companies that align with their values. If you too want to create long-term wealth but wish to do so by investing in ESG-responsible companies, consider consulting with a mutual fund investment planner first. They can help you identify the right green investment that matches your financial goals and values.

Types of Green Funds

The main type of green investment funds available in India today are the ESG funds. These funds gained significant popularity during the COVID-19 pandemic, so they are still an emerging category. Other than these, several thematic funds focus on specific sustainability-related sectors, like renewable energy and natural resources.

Thematic funds are considered very risky due to their sector concentration. As the name suggests, they focus on a narrow theme, which means their performance is highly dependent on the success of that particular industry. For example, a renewable energy fund can sometimes see peaks but can also face steep declines if the sector underperforms. A financial planner can assess your risk tolerance to help you understand whether or not such funds align with your financial goals and investment horizon.

Key Components of Green Funds

Fund managers assess companies based on their ESG scores to ensure they are making a genuine green investment. This ESG assessment forms the core of the fund’s selection process and helps align the portfolio with the values of its socially and environmentally conscious investors. Components include:

Environmental Responsibility

Funds evaluate how companies treat the environment by looking at factors such as:

How companies use and conserve water

Their efforts to control pollution

Waste management practices

Company’s impact on climate

Carbon emissions

Their use of renewable resources

Whether the company makes energy-efficient choices

Social Impact

This refers to how a company treats its employees and how responsible they are towards society as a whole. Includes factors like:

Gender diversity and equal pay

Labour rights

Employees welfare

Contributions towards public healthcare and education

Impact of business on the local communities

Governance Practices

Fund managers evaluate the following factors to ensure the company they’re investing in has ethical governance:

Board structure and compensation

Transparency in disclosing profits and income statements

How they treat their shareholders

History of corruption in the organisation

A company’s political contributions

ESG Ratings

Funds assess ESG scores made by independent agencies to ensure the companies they select score well on ESG compliance. As stated previously, there is no clear definition of ESG, so different agencies, like Morningstar, MSCI, and Sustainalytics have different ESG scoring criteria. A qualified investment planner can help you understand how these components work together to form a green portfolio.

Benefits of Green Funds

By investing in green funds one can reap many benefits:

Diversification and professional management: A green fund invests in an expertly selected basket of stocks to lower risk. Some green funds, like thematic funds revolving around green energy, can be very risky as their diversification is only spread across a handful of industries.

Long-term investment: Most green funds are equity-oriented and thus perform better over the long term. Also, ESG companies keep up with sustainability trends, so they are expected to grow as awareness around ESG factors increases. For example, an electric car company can potentially benefit greatly as governments push for cleaner transportation and consumers shift towards eco-friendly vehicles. That’s why a retirement planner might recommend green funds to clients with a long investment horizon.

Moral satisfaction: By investing in a green fund, you are investing in companies that align with your personal values. Just knowing that your money is invested in forward-thinking and sustainable companies can bring satisfaction along with returns.

SIP option: Like other mutual funds, green funds allow you to make fixed and regular contributions through SIPs. This option offers many advantages like building financial discipline, affordability, convenience and flexibility, and rupee cost averaging.

Tax benefits: Equity-oriented funds are more favourably taxed compared to debt-oriented funds. A tax consultant can help you understand the capital gains tax implications of your investments and advise you on how you can keep more of your hard-earned money through personalised strategies.

Challenges and Barriers to Green Funds

Now that we’ve discussed the advantages, it’s only fair to understand the challenges green funds face:

Limited universe: One of the main challenges is the relatively small pool of companies that meet ESG standards, which limits the number of stocks fund managers can choose from when building a diversified portfolio.

Lack of definition: What a green or ESG fund is, is not clearly defined by regulatory bodies. ESG scores also vary across independent agencies which makes it hard for funds to find companies that are ESG-compliant. Some ESG funds also invest heavily in companies that make substantial profits from tobacco, cigarettes, and fossil fuels.

Inadequate historical data: ESG funds are relatively new in India, so the availability of long-term performance data is limited. This lack of information makes it hard for investors to assess consistency and whether these funds are capable of providing better risk-adjusted returns in the future.

Higher risk: Since most green funds are equity-oriented and generally concentrated in select sectors like clean energy, banking, or technology, they carry higher risk.

Greenwashing: When companies exaggerate or even falsely claim their practices are sustainable and environment-friendly, they are said to be engaging in greenwashing. Some companies use manipulative marketing or selective reporting to come across as more responsible than they actually are, which is a problem for funds and investors alike.

Creating and Managing a Green Fund

If you’re looking to make a green fund investment, ESG funds are your best option at the moment, followed by high-risk green energy thematic funds. While the number of such funds is still limited, rising awareness around sustainability can maybe drive both demand and long-term value in the future.

Before you invest, consider several factors such as the fund manager’s track record, fund history, the asset management company’s reputation, the fund’s AUM, risk-adjusted returns, alpha, and beta.

You should also review the fund’s holdings to make sure its investments truly reflect your values and that the fund isn’t investing in companies that are greenwashing. As always, make sure the fund’s philosophy matches your own, and that your investment aligns with your goals and tolerance for risk.

Conclusion

ESG and green investment funds are a relatively new category of funds in India. They are designed to combine financial growth with environmentally sustainable and ethical business practices. Every day, more and more investors become conscious of the impact their money can make, so these funds give them a viable route to align their personal values with long-term wealth creation.

While these funds face many challenges, increasing regulatory focus and growing awareness around issues such as climate change can help strengthen them in the future. Several factors should be assessed before investing in mutual funds. Get personalized investing advice by giving our experts a call today!

Devices that monitor our heart rates based on a measurement at the wrist are pretty prevalent nowadays, including Fitbit, Garmin watches, and Apple Watches. There are also devices that promise more sophisticated results such as heart rate variability from Whoop. These devices then tell us insightful things about our recent workouts or our activity throughout the day, how long we should recover before our next hard workout, and even how well we are sleeping.

The trouble is that the accuracy of the data all this information is based on is suspect. I first noticed this back when I had a Fitbit. It would often read higher than I suspected was correct, based on how hard I felt I was working. The same is now true of my Garmin watch. I can be just warming up, and it will tell me my heart rate is in the 130’s, which I know can’t be true because I’d really be huffing and puffing. I recently put it to a test. I happen to also have a Polar H10 heart rate strap. And a separate device (my Garmin bike computer). So on the same ride, I made sure my watch was not paired to the strap, and only had wrist data available for heart rate. My bike computer was paired to the strap so it was a chest-based measurement. In such a comparison, we expect the chest measurement to be more accurate, but I was blown away how much the two differed. The two charts from a three-hour ride are shown below. The max heart rate from the wrist measurement was 41 beats two high, and suspiciously showed up when I was just warming up. There are various other places in the charts where the wrist results are just not right.

Chest Average Heart rate 80 Max 103Wrist Average Heart rate 96 Max 144

I had been reading up on optimum training techniques based on heart rate, all of which sound quite scientific. But I now know that the data I was basing this on was untrustworthy (I usually just use wrist-based because it’s an extra step to put on the strap). In the future I will make sure I use the strap when I really want to check heart rate. I will also put more trust in how my workout feels (perceived level of exertion).

Share this:

Related

Published by BionicOldGuy

I am a Mechanical Engineer born in 1953, Ph. D, Stanford, 1980. I have been active in the mechanical CAE field for decades. I also have a lifelong interest in outdoor activities and fitness. I have had both hips replaced and a heart valve replacement due to a genetic condition. This blog chronicles my adventures in staying active despite these bumps in the road.

View all posts by BionicOldGuy

As AI adoption accelerates across industries, businesses face an undeniable truth — AI is only as powerful as the data that fuels it. To truly harness AI’s potential, organizations must effectively manage, store, and process high-scale data while ensuring cost efficiency, resilience, performance and operational agility.

At Cisco Support Case Management – IT, we confronted this challenge head-on. Our team delivers a centralized IT platform that manages the entire lifecycle of Cisco product and service cases. Our mission is to provide customers with the fastest and most effective case resolution, leveraging best-in-class technologies and AI-driven automation. We achieve this while maintaining a platform that is highly scalable, highly available, and cost-efficient. To deliver the best possible customer experience, we must efficiently store and process massive volumes of growing data. This data fuels and trains our AI models, which power critical automation solutions to deliver faster and more accurate resolutions. Our biggest challenge was striking the right balance between building a highly scalable and reliable database cluster while ensuring cost and operational efficiency.

Traditional approaches to high availability often rely on separate clusters per datacenter, leading to significant costs, not just for the initial setup but to maintain and manage the data replication process and high availability. However, AI workloads demand real-time data access, rapid processing, and uninterrupted availability, something legacy architectures struggle to deliver.

So, how do you architect a multi-datacenter infrastructure that can persist and process massive data to support AI and data-intensive workloads, all while keeping operational costs low? That’s exactly the challenge our team set out to solve.

In this blog, we’ll explore how we built an intelligent, scalable, and AI-ready data infrastructure that enables real-time decision-making, optimizes resource utilization, reduces costs and redefines operational efficiency.

Rethinking AI-ready case management at scale

In today’s AI-driven world, customer support is no longer just about resolving cases, it’s about continuously learning and automating to make resolution faster and better while efficiently handling the cost and operational agility.

The same rich dataset that powers case management must also fuel AI models and automation workflows, reducing case resolution time from hours or days to mere minutes, which helps in increased customer satisfaction.

This created a fundamental challenge: decoupling the primary database that serves mainstream case management transactional system from an AI-ready, search-friendly database, a necessity for scaling automation without overburdening the core platform. While the idea made perfect sense, it introduced two major concerns: cost and scalability. As AI workloads grow, so does the amount of data. Managing this ever-expanding dataset while ensuring high performance, resilience, and minimal manual intervention during outages required an entirely new approach.

Rather than following the traditional model of deploying separate database clusters per data center for high availability, we took a bold step toward building a single stretched database cluster spanning multiple data centers. This architecture not only optimized resource utilization and reduced both initial and maintenance costs but also ensured seamless data availability.

By rethinking traditional index database infrastructure models, we redefined AI-powered automation for Cisco case management, paving the way for faster, smarter, and more cost-effective support solutions.

How we solved it – The technology foundation

Building amulti-datacenter modern index database clusterrequired a robust technological foundation, capable of handling high-scale data processing, ultra-low latency for faster data replication, and carefuldesign approach to build a fault-tolerance to support high availability without compromising performance, or cost-efficiency.

Network Requirements

A key challenge in stretching an index database cluster across multiple datacenters is network performance. Traditional high availabilityarchitectures rely on separate clusters per datacenter, often struggling with data replication, latency, and synchronization bottlenecks. To begin with, we conducted a detailed network assessmentacross our Cisco datacenters focusing on:

Latency and bandwidth requirements – Our AI-powered automation workloads demand real-time data access. We analyzed latency and bandwidth between two separate data centers to determine if a stretched cluster was viable.

Capacity planning – We assessed our expected data growth, AI query patterns, and indexing rates to ensure that the infrastructure could scale efficiently.

Resiliency and failover readiness – The network needed to handle automated failovers, ensuring uninterrupted data availability, even during outages.

How Cisco’s high-performance data center paved the way

Cisco’s high-performance datacenter networkinglaid a strong foundationfor building the multi-datacenterstretch singledatabase cluster. The latency and bandwidth provided by Cisco datacenters exceeded our expectation to confidently move on to the next step of designing a stretch cluster.Our implementation leveraged:

Cisco Application Centric Infrastructure (ACI) – Offered a policy-driven, software-defined network, ensuring optimized routing, low-latency communication, and workload-aware traffic management between data centers.

Cisco Application Policy Infrastructure Controller (APIC) and Nexus 9000 Switches – Enabled high-throughput, resilient, and dynamically scalable interconnectivity, crucial for quick data synchronization across data centers.

The Cisco data center and networking technology made this possible. It empowered Cisco IT to take this idea forward and enabled us to build this successful cluster which saves significant costs and provides high operational efficiency.

Ourimplementation – The multi-data center stretch cluster leveraging Cisco data center and network power

With the right network infrastructure in place, we set out to build a highly available, scalable, and AI-optimized database cluster spanning multiple data centers.

Cisco multi-data center stretch Index database cluster

Key design decisions

Single logical, multi-data center cluster for real-time AI-driven automation – Instead of maintaining separate clusters per data center which doubles costs, increases maintenance efforts, and demands significant manual intervention, we built a stretched cluster across multiple data centers. This design leverages Cisco’s exceptionally powerful data center network, enabling seamless data synchronization and supporting real-time AI-driven automation with improved efficiency and scalability.

Intelligent data placement and synchronization – We strategically position data nodes across multiple data centers using custom data allocation policies to ensure each data center maintains a unique copy of the data, enhancing high availability and fault tolerance. Additionally, locally attached storage disks on virtual machines enable faster data synchronization, leveraging Cisco’s robust data center capabilities to achieve minimal latency. This approach optimizes both performance and cost-efficiency while ensuring data resilience for AI models and critical workloads. This approach helps in faster AI-driven queries, reducing data retrieval latencies for automation workflows.

Automated failover and high availability – With a single cluster stretched across multiple data centers, failover occurs automatically due to the cluster’s inherent fault tolerance. In the event of virtual machine, node, or data center outages, traffic is seamlessly rerouted to available nodes or data centers with minimal to no human intervention. This is made possible by the robust network capabilities of Cisco’s data centers, enabling data synchronization in less than 5 milliseconds for minimal disruption and maximum uptime.

Results

By implementing these AI-focused optimizations, we ensured that the case management system could power automation at scale, reduce resolution time, and maintain resilience and efficiency. The results were realized quickly.

Faster case resolution: Reduced resolution time from hours/days to just minutes by enabling real-time AI-powered automation.

Infrastructure cost reduction: 50% savings per quarter by limiting it to one single-stretch cluster, by completing eliminating a separate backup cluster.

License cost reduction: 50% savings per quarter as the licensing is required just for one cluster.

Seamless AI model training and automation workflows: Provided scalable, high-performance indexing for continuous AI learning and automation improvements.

High resilience and minimal downtime: Automated failovers ensured 99.99% availability, even during maintenance or network disruptions.

Future-ready scalability: Designed to handle growing AI workloads, ensuring that as data scales, the infrastructure remains efficient and cost-effective.

By rethinking traditional high availability strategies and leveraging Cisco’s cutting-edge data center technology, we created a next-gen case management platform—one that’s smarter, faster, and AI-driven.

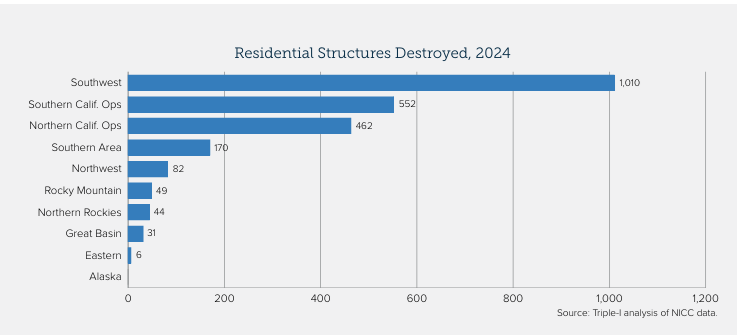

Wildfire risk is strongly conditioned by geographic considerations that vary widely among and within states. The latest Triple-I Issues Brief shows how that fact played out in 2024 and early this year and discusses the importance of granular local data for underwriting and pricing insurance in wildfire-prone areas, as well as for much-needed investment in resilience.

The 2024 wildfire season in the South and Southwest was particularly severe, marked by such events as the Texas and Oklahoma Panhandle fires in February and March and significant blazes in Arizona and New Mexico. The Southwest accounted for the largest number of residential structures destroyed by wildfire, and three of the top five areas for homes destroyed were in the South.

California accounted for the largest number of homes at risk for extreme wildfires. In the first half, the state experienced an above-average number of fires, though most were contained before growing to “major incident” size. Subsequent rains suppressed subsequent wildfire conditions – and caused substantial flooding.

But this rain contributed to an accumulation of fuels so that, when hurricane-force Santa Ana winds whipped through Los Angeles County in early January 2025, the conditions were right for fast-moving blazes to tear through Pacific Palisades and Eaton Canyon.

Temperature, humidity, wind, and topography vary too widely for a single “one size fits all” mitigation approach. This underscores the importance of granular data gathering and scrupulous analysis when underwriting and pricing insurance. It is also important that insurers proactively engage with diverse stakeholder groups to promote investment in mitigation and resilience.

A recent paper by Triple-I and Guidewire – a provider of software solutions to the insurance industry – uses case studies from three California areas with very different geographic and demographic characteristics to go deeper into how such tools can be used to identify properties with attractive risk properties, despite their location in wildfire-prone areas.

Can you gift mutual funds in India? Discover the legal ways, tax rules, and the best method to gift mutual fund units to your family or friends with ease.

In Indian families, gifting is often a heartfelt tradition. But today, beyond gold or gadgets, people are also looking to gift financial assets, like mutual funds, to their loved ones. A natural question arises—can mutual funds be gifted in India, and if so, what’s the proper way to do it?

Let’s walk through the legal, procedural, and tax-related aspects of gifting mutual funds, based on guidelines from AMFI, SEBI, and IT Department rules and regulations.

Can You Gift Mutual Funds in India?

Yes—but not as freely as you might think. Mutual fund units are not like jewellery or cash, which you can hand over easily. The transfer of mutual fund ownership is regulated, and depends on how the units are held—demat or physical.

As per SEBI and AMFI, mutual fund units: – Can be transferred as a gift only if held in demat form, via off-market transactions. – Cannot be transferred if held in non-demat (physical) form—except on death (i.e., transmission). – Cannot be transferred just by executing a Gift Deed.

1. Best Option: Invest Directly in Recipient’s Name The simplest way to “gift” mutual funds is by investing directly in the name of your family member.

Example: You want to gift your daughter a mutual fund. Instead of buying it in your name and trying to transfer it later, you: – Use her PAN, KYC, and bank details. – Invest directly into a mutual fund in her name.

For minor children, the investment will be made under their name, with a guardian (parent) managing the account until the child turns 18.

The cleanest approach is to directly invest in your child’s name. However, be aware that once your child turns 18, they gain full control over the investments, as it becomes their money. This means you’ll have no authority over the funds once they reach adulthood. So, it’s important to exercise caution, as their future decisions might not align with your expectations.

According to the clubbing provisions, if you withdraw the investment before your child turns 18, the gains will be taxed under your income, as the investment is still considered part of your financial assets. In the case of gifting mutual funds to a spouse, if the funds come from your earnings, the income generated from the mutual fund will be taxed under your income, not your spouse’s. This is because the source of the income matters for tax purposes.

2. Gifting via Demat Transfer (Off-Market) If you hold mutual fund units in demat form, and your recipient also has a demat account, you can transfer them via an off-market gift transaction.

Steps: 1. Ensure both donor and recipient have demat accounts (CDSL or NSDL). 2. Submit a Delivery Instruction Slip (DIS) to your Depository Participant. 3. Specify the recipient’s demat details and indicate it’s a gift.

This is the only SEBI-approved method for gifting existing units. Here’s a simple example of an off-market transaction:

Imagine you want to gift some mutual fund units to your brother, who has a demat account. Here’s how an off-market transaction would work:

Step 1: You have mutual fund units in your demat account, and your brother also has a demat account.

Step 2: You fill out a Delivery Instruction Slip (DIS), which is like an instruction to transfer the units from your demat account to your brother’s demat account. You’ll mention the mutual fund units and his demat account details.

Step 3: You submit the DIS to your Depository Participant (DP), which is the financial institution managing your demat account.

Step 4: The transfer happens off-market, meaning it’s a private transfer between two parties and does not happen through the stock exchange.

Step 5: Your brother now owns the mutual fund units in his demat account, and the transfer is complete.

This is an off-market transaction because the transfer occurs directly between you and your brother, outside of the stock exchange, with the help of a DIS form.

3. Why a Gift Deed Alone Won’t Work

A Gift Deed, though legally valid for movable property, does not serve as a tool to transfer mutual fund units. Mutual funds in physical form are non-transferable, and AMCs or RTAs do not accept gift deeds for ownership change.

You may use a gift deed as a supporting document when doing an off-market transfer via demat, but on its own, it’s not effective.

4. Use a Will for Post-Death Transfer (Transmission)

If your intention is to pass on mutual funds after your death, then a Will is the correct instrument.

Transmission Process: – Units are transferred to nominee or legal heir after submission of required documents (death certificate, KYC, Will copy, etc.). – If there’s no nomination, transmission is more complex and may require legal heir certificates or probate.

A nomination ensures quicker access, while a Will provides legal clarity on inheritance.

Do note that nominees by default will not be considered as asset owners. They act like trustees to transfer the assets to the legal heirs.

5. Can You Gift via Online Platforms?

Some fintech platforms like Kuvera or Zerodha Coin allow you to gift mutual funds where: – You choose a scheme. – Pay from your bank account. – The recipient receives a link to accept the gift and complete their KYC.

Units are then directly allotted to the recipient, just like a fresh purchase.

Convenient, but not a “transfer”—it’s a new investment on behalf of someone else.

Income Tax Implications of Gifting Mutual Funds

Here’s where things become critical—especially if you’re gifting to spouse or minor children.

1. Gift Tax – Section 56(2)(x) – Gifts from relatives (as defined under the Income Tax Act) are fully tax-exempt, regardless of amount. – Gifts from non-relatives exceeding Rs.50,000 in a year are taxable in the recipient’s hands as “Income from Other Sources”. Who are considered relatives? – Spouse, parents, children, siblings, lineal ascendants/descendants, etc.

2. Capital Gains Tax – Who Pays and When? When the recipient sells the mutual fund units later, capital gains tax will apply. The cost and holding period of the donor (you) will be considered for tax calculation.

Example: – You bought a mutual fund in 2020, gifted it to your spouse in 2024. – They sell it in 2026. – For tax purposes, the investment is considered from 2020, and capital gains will be long-term or short-term accordingly.

3. Clubbing of Income – Section 64 This is extremely important and often overlooked.

If you gift mutual funds to: – Your spouse, or – Your minor child (not a disabled child),

Then any income or capital gains generated from that investment is clubbed with your income.

You gift Rs.1 lakh in mutual funds to your wife. She redeems it later with a gain of Rs.10,000. This Rs.10,000 gain will be taxed in your hands, not hers.

Exception: – Clubbing does not apply if gifted to: – Adult children – Parents – Siblings – Disabled minor child – Other relatives (as long as not spouse/minor)

Takeaway: Gifting is tax-free, but income arising from it may come back to you under clubbing provisions. So plan accordingly.

Summary: Can Mutual Funds Be Gifted?

Method

Allowed?

Tax Implications

Notes

Direct Investment in Recipient’s Name

Yes

May invoke clubbing if spouse/minor

Most recommended

Demat Transfer (Off-Market)

Yes

Clubbing applies if spouse/minor

For existing units in demat

Gift Deed (Physical Mode)

No

N/A

Not accepted by AMCs

Will

Yes

Tax applies after transmission

For inheritance only

Online Platform Gifting

Yes

Treated as direct investment

Easy for beginners

Final Thoughts

Mutual fund gifting in India is legally allowed, but comes with conditions:

Gift mutual funds through direct investment or demat transfer.

Don’t rely on a Gift Deed to change ownership—it won’t work.

For legacy planning, always draft a Will and align it with your nominations.

Understand clubbing rules before gifting to your spouse or minor children, or you may end up paying tax on their gains.

As SEBI-registered financial planners, we often advise clients to gift mindfully—not just for tax-saving, but for long-term wealth-building within the family.

For Unbiased Advice Subscribe To Our Fixed Fee Only Financial Planning Service

Happy almost Fall, friends! I can’t believe how quickly time flies. As much as I love summer, once I embrace that Fall is closer, I do get excited for cozy weekends, crisp sunny days, soccer season, football season, and getting outside even more since it’s not as hot.

With my soccer season starting up, I started to get back into some track workouts and running workouts for the season.

For those that know me, they know I’m not much of a “long distance girlie”. I’m more of a sprint and mid-distance girlie while still using the word distance lightly.

After some treadmill and track runs, I quickly found that I was going to need some actual women’s running shoes if I wanted to train efficiently and honestly with comfort and support.

I did some research and ended up going with the Ultraboost 5X Shoes by adidas and thought I’d give you a review as “what shoes should I buy?” is a one of the top questions I get asked most as a Trainer. Since I’ve been wearing these for a few months now, hopefully my review can help!

First let’s just talk about the COLOR as I happen to be matchy-matchy with my nails too!

I usually go for a neutral shoe all day every day but when I saw this color combo and wanted my “running shoes” to feel special that I wore for a specific goal, I couldn’t pass these up.

The toe of the shoe is spacious enough for all of my toes and doesn’t cause any friction. I like to train 400’s and 200’s on the track, so I strike with the ball of my foot often, and these provide awesome support and bounce for my foot in my sprints.

The heel of the shoe allows for comfortable ankle support and motion whenever I hit any longer distances.

I was worried at first that I wouldn’t love the higher flap behind the ankle but it truly didn’t rub on my skin or hit weirdly in any way.

The PRIMEKNIT upper tongue of the shoe lays smooth on the top of my foot and doesn’t bother me in any way.

The saddle of the shoe, which is the reinforced area around the instep, provides me with good support without being too tight.

I also went with my true to size 8.5 and feel that they are very true to size!

I recently was at a foot specialist for tendinitis of my left foot and often if any shoe is too narrow or tight, my tendonitis will flare causing pain. These shoes do not flare up my tendonitis which is such a plus for me!

When it comes to the weight of the shoe, this shoe shocked me on how light it is! I even had a client who wanted to try them on and she loved how light they were.

I don’t think you can go wrong with an Ultraboost of any kind from adidas but if you’re looking to hit some sprints or distance, I do think this is a great shoe choice that will last you and support your training!

Next post we’ll be chatting all things “cozy” with my cozy collection top outfit picks so stay tuned on the blog! Did someone say oversized womens hoodies and crewnecks??

SentinelOne IncS reported financial results for the first quarter after the market close on Wednesday. Here’s a look at the key metrics from the quarter.

Q1 Earnings: SentinelOne reported first-quarter revenue of $229.03 million, beating the consensus estimate of $228.35 million, according to Benzinga Pro. The cybersecurity company reported first-quarter adjusted earnings of two cents per share, in line with analyst estimates.

Total revenue increased 23% year-over-year. Annualized recurring revenue (ARR) increased 24% year-over-year to $948.1 million as of April 30. Customers with ARR of $100,000 or more grew 22% to 1,459 in the quarter.

The company ended the period with $1.2 billion in cash, cash equivalents and investments. SentinelOne’s board also authorized a $200 million share repurchase program.

“Our top-tier growth and margin improvement reflect continued platform momentum and customer success,” said Tomer Weingarten, CEO of SentinelOne.

“Our innovation engine is fueling adoption across AI, Data, Cloud and Endpoint. With Singularity, we’re leading a transformational shift toward AI-powered security for the future.”

Guidance: SentinelOne expects second-quarter revenue of approximately $242 million versus estimates of $244.88 million. The company also lowered its full-year 2026 revenue guidance from $1.007 billion to a range of $996 million to $1.001 billion. Analysts were expecting full-year revenue of $1.01 billion.

Shares appear to be selling off in reaction to the soft outlook. SentinelOne executives are currently discussing the quarter on a conference call with investors and analysts that kicked off at 4:30 p.m. ET.

S Price Action:SentinelOne shares were down 11.44% in after-hours, trading at $17.42 at the time of publication Wednesday, according to Benzinga Pro.

Cisco multi-data center stretch Index database cluster

Cisco multi-data center stretch Index database cluster

![Ultraboost 5X Running Shoe [review]!](https://i0.wp.com/www.powercakes.net/wp-content/uploads/2024/09/IMG_6329-1.jpg?w=1200&resize=1200,0&ssl=1 "Ultraboost 5X Running Shoe [review]!")

![Ultraboost 5X Running Shoe [review]!](https://www.powercakes.net/wp-content/uploads/2024/09/IMG_6329-1.jpg "Ultraboost 5X Running Shoe [review]!")

")