‘EAT’S FINALLY BACK!’ Worldbex Services International (WSI) welcomes all food lovers and food businesses to attend this event and see how the Philippine F&B industry continues to grow and innovate, happening from June 11 to 15, 2025, at the World Trade Center Metro Manila!

The Manila Foods and Beverages Exposition (MAFBEX) returns this year to bring you the 19th edition of the biggest and tastiest food & beverage expo in the Philippines! Unlike other F&B events, MAFBEX sets itself apart with its unique activities and highlights. These highlights will serve as a great introduction to the world-class potential of the Philippine food & beverage industry, attracting not only the Filipino market but also internationally. It is also proven by its ever-growing foot traffic, reaching 52,000 quality audiences!

Chefs of the World

Located at the Main Lobby of the World Trade Center, the Chefs of the World stage shines a spotlight on the famous local and international chefs of the Philippines who will demonstrate how to make gourmet dishes and 5-star cuisine through simple techniques and easy steps that anyone can follow.

MAFBEX Culinary Cup: Home Chef Edition

The MAFBEX Culinary Cup returns this year, now more competitive than ever! The Culinary Cup highlights the saying that “Anyone can be a gourmet chef in their way”, bringing ordinary people together and giving them a chance to showcase their best cooking in this competition. The best home chef gets to win the title of “Grand Home Chef” and a chance to further improve their cooking skills!

The Brew District

A place for coffee lovers to mingle and enjoy the fresh scent of coffee beans and tea leaves, the Brew District features the Philippines’ best local breweries while shining a spotlight on the local growers and farmers, highlighting their hard work and sacrifice to provide the best produce.

And for the first time, MAFBEX is partnering with the Philippine National Coffee Competition to bring you two National Championship competitions for coffee lovers: The are the National Barista Championship and the National Brewers Cup. These competitions will take the coffee industry of the Philippines to the next level.

MAFBEX Scoop

An exhibit that champions innovation, MAFBEX Scoop showcases the best innovative food equipment, materials, and food services that will make your food journey a whole lot easier.

MAFBEX Talks

A series of talks and seminars for those who want to get into the food business. MAFBEX Talks offers a wide range of topics that will help you get the edge you need to start your own food business and have a better understanding of food theory.

MAFBEX Flair Cup Competition

A show of skill and flair, the MAFBEX Flair Cup Competition is a show to see who will mix the best drinks while displaying their skills of flairtending.

YHE Competitions

MAFBEX is once again partnering with the Young Hoteliers’ Expositions from the College of St. Benilde to bring you even more shows and competitions for the young students who are looking to make a name for themselves in the F&B industry.

MAFBEX Bites

Missing out on the on-ground activities and shows of MAFBEX? Now, you don’t have to miss much! MAFBEX Bites is the online live platform of MAFBEX, showcasing the latest happenings on ground while giving exhibitors an avenue to advertise and show their latest products tot the digital world.

MAFBEX 2025 is looking to be the biggest F&B event of the year, bringing only world-class cuisine and event experiences to visitors who want to satisfy their cravings. You too can have a taste of what’s to come and more when you get your tickets now at https://mafbex.com/. You can also avail of the 5+1 promo that’s available until May 27, 2025! Don’t miss out and buy now!

MAFBEX 2025 is organized by Worldbex Services International and is for the benefit of the ABS-CBN Foundation Inc.

This post is part of a series sponsored by AgentSync.

P&C market summary

It’s no secret the property and casualty (P&C) market is full of struggle. After years of premium increases and market withdrawals, the right sizing of risk-to-profit is … a work in progress.

Some areas of the market have seen the necessary improvements to lift underwriting above water. Auto insurance, for instance, has buoyed the profiles of the carriers who write it, thanks to the post-pandemic years of sharp premium increases.

Some markets are notoriously difficult. Florida and California, for instance, are both still on a journey of legislative reform and market changes. And wildfire risk across the country has insurers rethinking their approach to underwriting this risk.

Shareholder expectations are their own force within the industry, and carriers and agencies that hope to spread their risks while exploring new avenues for profitability will necessarily be on the lookout for good partners for merging or acquisition.

That brings us to the following: For P&C carriers that hope to deliver on their bottom line, McKinsey reports four common factors that can make the difference in the coming year:

Clear strategies to capture profitable growth and focused execution

Modernized underwriting

Cost-effectively acquiring businesses that solve for distribution

Operational efficiencies that lower internal administrative costs

Clear strategies to capture profitable growth and focused execution

If you read the McKinsey report and it seemed like the summary was, “to win, you need a plan to win,” you’ll be forgiven. But if you’ll indulge us, there’s a little bit of nuance.

Sure, it may seem like it goes without saying that you need a strategy to grow, but here’s why all those adjectives matter:

Clear strategies: If it takes some mental gymnastics to tie your current tactics to your business objectives, then your message is muddy and your team can’t possibly be aligned and rowing in the same direction.

Profitable growth: Growth that just takes your current reality and makes it bigger isn’t growing profit, because it grows your challenges alongside any new business you bring in. You’re looking for growth that puts more money in your business coffers, not the same problems at a different scale.

Focused execution: Yes, everyone looks busy at your business. But if everyone’s spending their time putting out a million little fires and working on side projects and things that don’t move the needle, then your effort is just a lot of noise (which takes us back to those clear strategies).

The McKinsey report champions the idea that most strategies will involve some sort of M&A plans. But again, the principles of clear, profitable, and focused apply. If your acquisitions are scattershot affairs of snapping up partners without evaluating their overlap with your existing pipeline or how they align with your growth strategies, you may find yourself in a morass of a merger with no clear line on profitability. I.e., bigger ain’t always better.

Modernized underwriting

Telematics. Internet of Things devices. Underwriters have more tools at their disposal than ever before in collecting data about insureds. Yet, this overwhelming mass of data is only helpful if you know what to do with it and have the processes in place to support it.

AI can be instrumental in assessing a risk even as applications and information comes from multiple varied sources. But this is only useful if you can ensure you’re falling in line with various states’ regulations of AI in underwriting and plugging what you can use into a comprehensive and holistic system.

In the end, your business may have a very tailored definition of what “modernized” underwriting means to you or your business partners. But if you don’t have a way to activate it, it’s still just data collection for the sake of data collection instead of delivering lower business risk for you and right-sized premiums for your customers.

Cost-effectively acquiring businesses that solve for distribution

M&A is the lifeblood for many P&C carriers and agencies alike. But the margins on your new ventures—and the long-term ROI—vary. A lot.

What makes a new acquisition cost effective? You get the most ROI out of an acquisition that:

Adds opportunities without significantly increasing your business or regulatory risk

Brings on more blood without significant duplications or overlaps in internal operations

Has a clean and understandable balance sheet

Unfortunately, businesses that have low internal operations costs, are streamlined, and are clearly profitable are rarely just sitting on the market with a “Buy Me” nametag. Instead, you may not really know whether a business can be purchased and cleaned up to be a profitable add until after you’re already too deep.

Businesses that solve for distribution are businesses that may have relationships you want to add to your network. Or they may have impressive downstream agents. Or they may have an innovative way of going to market. Whatever it is, focus your time and effort on acquiring businesses that are an add for you, not just businesses that make you “bigger.”

The cost-effectiveness of an acquisition really comes down to the way you handle your internal administrative costs. Businesses that purchase another company and then let that company continue to operate in a bubble often see the risks of M&A (agent churn, regulatory risks, bloat) with the barest of skinny-margin rewards.

Operational efficiencies that lower internal administrative costs

The real payoff for you and for any M&A activity in your business comes from your internal operational efficiencies. When you streamline your internal administrative costs, you make it easier for a handful of employees to manage lots of complexity.

Onboarding new partners, new agents, and new acquisitions necessarily means a high volume of data. But most of it is the same data, every time. So having every single onboard turn into a special snowflake is a waste of time and money (and since time is money, it’s a waste of more money).

By streamlining your internal processes, you lower your administrative costs and make your M&A activities far more successful. It adds up to more money in your pocket and the ability to be more reactive and proactive when the P&C market gets turbulent.

AgentSync and your M&A success

AgentSync helps agencies and carriers in P&C stay abreast of regulatory changes and shifting market conditions. By streamlining internal processes, our clients can make their M&A activity more profitable while also improving their reputations with their distribution partners, from agencies to carriers and everyone in between.

Onboarding portals make it easy for agency partners and individual producers to onboard and maintain their own data without staff babysitting the process.

Hierarchies that can handle complexity make it easier to accurately reflect business relationships and maintain accurate commission payments no matter what state or business structure an agent is affiliated with.

Integrated data from the industry source of truth makes it abundantly clear which subordinate businesses are selling policies (and which ones cost more than they’re worth).

Easy, accurate reporting cuts down hours of personnel time to hunt information, and makes regulatory audits a breeze.

If you’re ready to level up your M&A activity, see what else AgentSync can do for you; schedule a demo today.

April 22, 2025 Posted By: growth-rapidly Tag:

Uncategorized

Achieving a perfect credit score of 850 (on the FICO or VantageScore scale) is rare but possible with disciplined financial habits. A score of 850 requires near-perfect management of credit factors over time. Below is a concise, actionable guide to maximize your credit score, tailored to the key factors that influence it, based on current credit scoring models.

Key Factors Affecting Your Credit Score

FICO and VantageScore models weigh similar factors, though exact weightings vary slightly:

Payment History (FICO: 35%, VantageScore: ~40%): Paying all bills on time is critical.

Credit Utilization (FICO: 30%, VantageScore: ~20%): The ratio of credit card balances to credit limits.

Length of Credit History (FICO: 15%): Average age of accounts and age of oldest account.

Credit Mix (FICO: 10%): Managing both revolving (credit cards) and installment (loans) accounts.

New Credit (FICO: 10%): Recent credit inquiries and new accounts.

Amounts Owed (VantageScore: ~20%): Total debt relative to available credit.

Derogatory Marks: Bankruptcies, collections, or foreclosures (heavily weighted in both models).

An 850 score requires optimizing all these factors consistently, as even minor missteps can prevent perfection.

Steps to Raise Your Credit Score to 850

Pay All Bills On Time, Every Time:

Why: Payment history is the largest factor. A single missed payment can drop your score by 100+ points and stay on your report for 7 years.

How:

Set up autopay for at least the minimum payment on all credit cards and loans.

Use calendar reminders or budgeting apps (e.g., Mint, YNAB) to track due dates.

Pay off credit card balances in full each month to avoid interest and ensure reported payments are timely.

If you’ve missed payments, bring accounts current and maintain perfect payment history moving forward. Older late payments (e.g., 2+ years) have less impact.

Keep Credit Utilization Below 10%:

Why: Utilization is the second-largest factor. Scores peak when total and per-card utilization is under 10% (e.g., $100 balance on a $1,000 limit = 10%).

How:

Pay credit card balances multiple times per month to keep reported balances low. Check when your issuer reports to bureaus (often at statement closing) and pay before this date.

Request credit limit increases from issuers every 6–12 months to lower utilization, but don’t use the extra credit.

Avoid closing old credit card accounts, as this reduces total available credit and raises utilization.

If utilization is high, pay down balances aggressively, starting with cards closest to their limits.

Example: If you have three cards with $5,000 total limits, keep total balances below $500.

Maintain a Long Credit History:

Why: A longer credit history boosts scores, as it demonstrates reliability. The average age of accounts and age of your oldest account matter.

How:

Keep your oldest credit card open and active with small, recurring charges (e.g., a $10 subscription) paid off monthly.

Avoid opening multiple new accounts in a short period, as this lowers the average age of accounts.

If you’re younger or have a thin file, become an authorized user on a trusted person’s long-standing, well-managed credit card to inherit their account’s history.

Note: It takes years to maximize this factor, so patience is key for an 850 score.

Diversify Your Credit Mix:

Why: Handling both revolving (credit cards) and installment (auto, mortgage, student loans) accounts shows financial versatility.

How:

If you only have credit cards, consider a small personal loan or a secured loan (e.g., through a credit union) and pay it off on time. Avoid unnecessary debt, though.

If you have loans but no credit cards, open a secured credit card with a low limit and use it responsibly.

Don’t take on debt solely for credit mix unless necessary, as this factor has less weight.

Limit New Credit Inquiries and Accounts:

Why: Hard inquiries (from new credit applications) can ding your score by 5–10 points each and stay on your report for 2 years. Too many new accounts signal risk.

How:

Apply for new credit sparingly—only when needed (e.g., for a mortgage or major purchase).

Space out applications by at least 6 months to minimize impact.

Check prequalification offers (soft inquiries) to gauge approval odds without affecting your score.

If shopping for a loan (e.g., auto or mortgage), cluster applications within a 14–45-day window, as FICO and VantageScore count these as a single inquiry.

Monitor and Dispute Errors on Your Credit Report:

Why: Errors like incorrect late payments or accounts that aren’t yours can lower your score.

How:

Check your credit reports from Equifax, Experian, and TransUnion for free at AnnualCreditReport.com (weekly access is still available post-2023).

Use services like Credit Karma or Experian’s free monitoring for real-time alerts, but verify data against official reports.

Dispute inaccuracies online or by mail with the bureaus, providing documentation (e.g., payment records). Bureaus must investigate within 30 days.

Common errors: wrong balances, duplicate accounts, or fraudulent accounts from identity theft.

Resolve Derogatory Marks:

Why: Bankruptcies, collections, or foreclosures can prevent an 850 score. These stay on your report for 7–10 years but lose impact over time.

How:

Pay off or settle collections accounts. Request a “pay-for-delete” agreement in writing, though not all agencies comply.

For accounts in collections, negotiate to pay in full or settle for less, and ask for removal from your report.

If derogatory marks are old (5+ years), focus on perfecting other factors, as their impact fades.

Avoid new negative marks at all costs, as recent issues are heavily penalized.

Use Advanced Strategies for Fine-Tuning:

Authorized User Status: If your score is close to 850 (e.g., 800+), being added as an authorized user on a card with a perfect payment history and low utilization can nudge you higher.

Balance Reporting Timing: Pay off credit card balances before the statement closing date, not just the due date, to report a $0 or near-$0 balance to bureaus. A small balance ($5–$10) on one card can slightly boost scores, as it shows activity.

Credit Builder Loans: For those with thin files, a credit builder loan (offered by credit unions or platforms like Self) can add positive installment loan history.

Experian Boost: Opt into Experian Boost to add on-time utility, phone, or streaming payments to your Experian report. This may not directly lead to 850 but can help if your score is lower.

Timeline and Expectations

Starting Score Matters:

300–600: Focus on paying bills on time, reducing debt, and resolving derogatory marks. Reaching 850 may take 2–5 years.

600–750: Optimize utilization (<10%), avoid new inquiries, and build credit history. Expect 1–3 years to reach 800+, then fine-tune for 850.

750–800: You’re close. Perfect payment history, keep utilization under 10%, and maintain old accounts. Reaching 850 could take 6 months to 2 years.

800+: You’re in the top tier (FICO scores 800–850 are “exceptional”). Maintain perfect habits and avoid any negative actions. Minor tweaks (e.g., lowering utilization to 1–5%) can push you to 850 in months.

Time Factor: An 850 score often requires 10+ years of credit history, multiple accounts, and no recent negative marks. Younger people or those with thin files may need to build history first.

Practical Tips for Austin, Texas

Local Resources: Austin has credit unions like University Federal Credit Union (UFCU) or Amplify Credit Union that offer secured credit cards or credit builder loans to boost scores. These are ideal for thin files or recovering from derogatory marks.

Cost of Living: Austin’s high cost of living (e.g., median rent ~$1,800/month) can strain finances. Budget carefully to avoid missed payments or high credit card balances.

Job Market: If you’re in a field like runway modeling (per your prior question), irregular income may make autopay and low utilization harder. Use a budgeting app to smooth cash flow and prioritize credit card payments.

Common Pitfalls to Avoid

Missing even one payment can reset your progress toward 850.

Closing old accounts reduces credit history length and available credit, raising utilization.

Maxing out cards, even if paid off monthly, can hurt if high balances are reported.

Applying for multiple credit cards or loans in a short period signals risk.

Ignoring credit reports can miss errors or fraud that lower your score.

Monitoring Progress

Use free tools like Credit Karma (VantageScore) or Experian’s app (FICO) to track your score monthly.

Pull full credit reports from AnnualCreditReport.com quarterly to verify accuracy.

Sign up for alerts from your bank or credit card issuer to catch missed payments or high balances early.

Why 850 May Not Matter

Diminishing Returns: Scores above 760–800 qualify for the best loan rates and credit card offers. An 850 score offers no additional practical benefits for most purposes (e.g., mortgages, auto loans).

Focus on 800+: If 850 feels out of reach, aim for 800, which is still exceptional and achievable with slightly less perfection.

Example Plan (Starting at 700)

Month 1: Check credit reports for errors and dispute inaccuracies. Set up autopay for all accounts. Pay down credit card balances to <10% utilization.

Month 3: Request a credit limit increase on one card to lower utilization further. Keep oldest card open and active.

Month 6: Avoid new credit applications. If needed, add a small installment loan to diversify credit mix.

Year 1: Maintain perfect payments and low utilization. Become an authorized user on a trusted person’s card if history is short.

Year 2: Fine-tune by reporting near-$0 balances and ensuring no derogatory marks. Score should approach 800–850 if all factors are optimized.

Final Notes

Achieving an 850 credit score requires:

Perfect payment history (no missed payments, ever).

Very low utilization (<10%, ideally 1–5% across all cards).

Long credit history (10+ years, with old accounts kept open).

Diverse, well-managed accounts (cards and loans).

No recent inquiries or derogatory marks.

Start by checking your current score and reports to identify weaknesses (e.g., high utilization, short history). Focus on the highest-impact actions first: timely payments and low utilization. If you’re in Austin, leverage local credit unions for tools like secured cards. For personalized advice, share your current score or specific issues (e.g., collections, high debt), and I can tailor recommendations further. If you need help accessing credit reports or finding local resources, let me know!

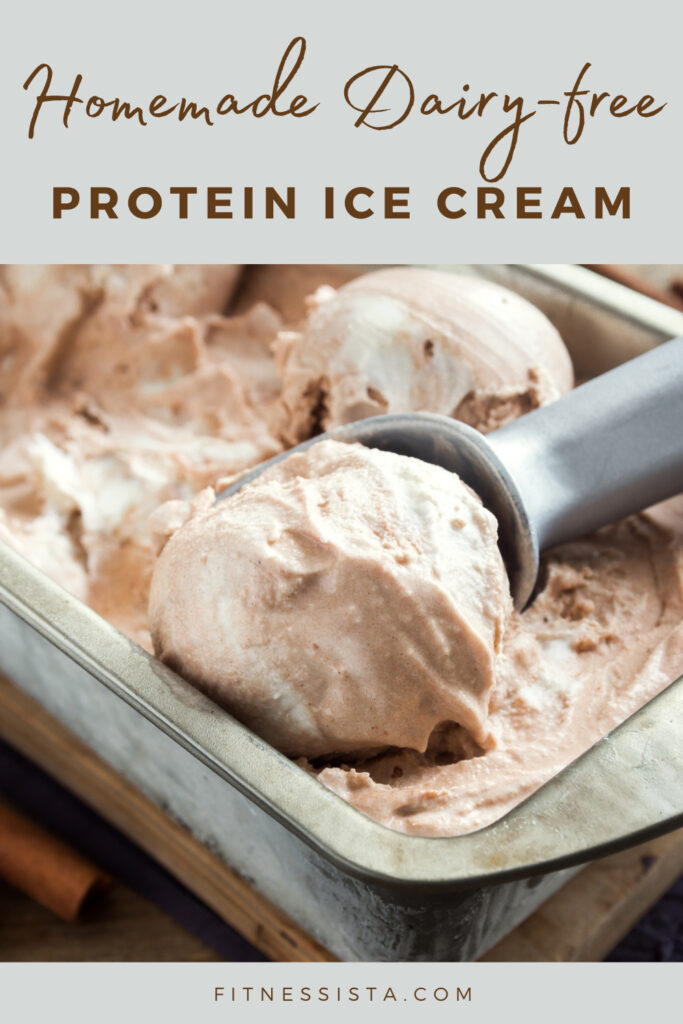

Why not sneak a lil protein in with our sweet treats?

Hi friends! I hope you’re having a lovely day! We’re back in Barcelona and living that Spain life. If you have any questions while we’re here, please let me know, and please send any recs my way!

Today, let’s talk about protein desserts. TBH, I feel like if you’re going to have a dessert… have a DESSERT. Like a real one. No protein powder, no chickpeas, just give me chocolate and real sugar.

But I understand that those options aren’t the best for blood sugar and that every desserts can have a little extra nutrition added in. For these occasions, I’ve rounded up eight high-protein dessert recipes that are not only delicious, but packed with good ingredients to keep you feeling fueled and satisfied. Whether you’re gluten-free, dairy-free, or just want some new post-workout treats, I’ve gotchu.

This one’s a favorite at our house! Made with frozen bananas, your favorite protein powder, and a splash of almond milk, this dreamy, creamy treat comes together in minutes—and you don’t even need an ice cream maker. Totally customizable and kid-approved.

These brownies are rich, fudgy, and packed with protein thanks to collagen peptides and almond flour. They’re also gluten-free, dairy-free, and perfect for meal prep. Bonus: collagen is great for your skin, joints, and hair.

This is the best of all dessert worlds—a giant cookie meets protein-packed cake. It’s soft, chewy, and made with oat flour, peanut butter, and protein powder. Perfect for celebrations or just because.

This creamy cheesecake is made with cottage cheese and Greek yogurt, naturally sweetened with maple syrup, and packed with protein. It’s a lighter take on the classic dessert that still delivers on flavor.

This mug cake is ready in just a few minutes and uses ingredients like protein powder, cocoa powder, almond milk, and almond butter. It’s gluten free, naturally sweetened and super satisfying.

These no-bake protein balls are made with oats, peanut butter, flaxseed, and a scoop of your favorite protein powder. Easy to make ahead and great to grab on the go for a snack that

This banana bread is a cozy, protein-packed twist on a classic. It uses Greek yogurt, eggs, almond flour, and protein powder to give you a hearty slice that works for breakfast or dessert.

This one doubles as breakfast or dessert and is made with almond milk, cocoa powder, protein powder, and chia seeds. It’s rich, chocolatey, and great to meal prep ahead of a busy week.

Whether you’re post-workout or just need a little sweet treat that won’t spike your blood sugar, these high-protein desserts are all winners. Let me know which one you try first, or if you have a fave, please shout it out in the comments section below!

xo,

Gina

Success! Check your email for a free 30-day meal and fitness cheat sheet

“I want to be unequivocally clear: I have never drugged anyone, nor have I ever given anyone pills to take,” she wrote in a post captured by Onsite.

Dawn Richard is responding to ex-boyfriend Que’s shocking claims of her drugging him at the request of their Bad Boy boss Sean “Diddy” Combs.

The Danity Kane singer shared a since-deleted statement on X denying the Day26 singer’s claims, which he revealed on Aubrey O’Day’s Do You Believe Me Now? podcast.

“I want to be unequivocally clear: I have never drugged anyone, nor have I ever given anyone pills to take,” she wrote in the post captured by Onsite.

Richard said Que’s claims are “categorically false” and don’t coincide with their continued relationship after the alleged drugging took place.

“If such a belief were genuine,” she wrote, “it would be inconsistent with the actions that followed—like inviting me into your home, introducing me to your family, and continuing a relationship.”

Her statement has faced backlash online, with many siding with Que and pointing to her recent court testimony against Diddy as a reason to question her denial.

“Her response makes no sense,” one critic wrote. “She said she didn’t drug him, and if she did, then why would he continue the relationship, but she didn’t she just testify how she watched Diddy abuse Cassie multiple times and she continued working with him?”

As details of the horrors surrounding Diddy’s behavior continue to emerge in his trial for federal sex trafficking and RICO charges, many of his artists and affiliates are receiving added attention on what they might say or reveal about the disgraced music mogul.

Que claims Richard gave him what he believes was a horse tranquilizer, which triggered a psychotic episode that took time to recover from.

“Whatever ritual, spell, or manipulation that pill carried, it hijacked my autonomy,” Que shared in a lengthy Instagram caption. “I began isolating myself. Sleep became my only escape from the pressure in my skull. I truly believed it was orchestrated by her boss—a display of power meant to destabilize a ‘weak’ mind and instill fear.”

Richard said she remained silent about their breakup out of respect and is now calling for compassion toward everyone affected by Diddy’s alleged abuse. “This isn’t about one person,” she wrote. “My intention has always been to move forward with integrity.”

More and more parents are choosing plant-based drinks for their toddlers, often because they think they’re making a healthier or more sustainable choice. Whether it’s almond, oat or soy, these alternatives are showing up in sippy cups across the U.S. — and often replacing cow’s milk entirely. But just because something is labeled “plant-based” or “dairy-free” doesn’t mean it’s nutritionally complete, healthy or developmentally appropriate for young children.

This is especially important during the vulnerable window between 12 and 24 months, when a child’s brain, bones and body are growing at a rapid pace. Every bite and sip matters. And when key nutrients are missing, it quietly undermines that growth in ways most parents don’t see coming.

If you’ve ever questioned whether a plant-based drink is a safe swap for milk — or if you’re already relying on one without knowing the full impact — you’re not alone. That’s exactly what researchers have started to investigate, and the findings are eye-opening. Let’s take a closer look at what happens when plant-based drinks replace cow’s milk in toddlers’ diets.

Most Plant-Based Drinks Fail to Meet Toddlers’ Nutritional Needs

A German study published in the Journal of Health, Population and Nutrition set out to understand what happens when you swap cow’s milk for plant-based alternatives in children’s diets.1 Researchers substituted only the daily serving of cow’s milk with common plant-based options like soy, oat and almond drinks, while keeping the rest of the diet unchanged. Their goal was to measure the nutritional fallout from this single swap.

• The study included common store-bought drinks and child-specific formulas — Six drinks were analyzed: basic soy, oat and almond drinks; fortified versions of soy and almond drinks; and two products marketed specifically for toddlers.

This included a soy-based “growing-up” drink and a dietetic soy formula for infants with milk intolerance. These represented typical items found in German markets and closely mirrored what parents actually purchase for young children.

• Most plant-based drinks caused a sharp drop in important nutrients — Daily intake of calcium, vitamin B2 (riboflavin), vitamin B12 and iodine fell by around 50% when non-fortified plant-based drinks were used.2 That means swapping out cow’s milk cut these important nutrients in half, even in an otherwise well-balanced meal plan.

• Nutrient bioavailability is a problem in many plant-based drinks — Even when drinks are fortified, the minerals and vitamins added are often less bioavailable than those found naturally in milk. That means your body absorbs less of what’s listed on the label. So, even if numbers on the label seem high, the actual amount your child’s body uses is often far lower.

• Parents need better tools to assess these swaps — Researchers warned that parents can’t accurately assess the impact of swapping cow’s milk for plant-based alternatives.

Most drinks look healthy on the surface and include marketing claims like “dairy-free” or “source of calcium,” but few truly match milk’s nutritional profile. Even a small change in a toddler’s daily diet has ripple effects on their long-term growth, bone health, immune function and brain development.

For clarity, this study didn’t involve physically swapping milk for plant-based drinks and then checking nutrient levels in children. Instead, it used a theoretical model based on the Optimized Mixed Diet (OMD), which is a guideline diet for children in Germany.

The researchers created scenarios where they replaced all fluid cow’s milk (219 g/day) in the OMD’s 7-day menu with different plant-based drinks (soy, oat, almond, fortified or non-fortified). They then calculated the nutrient intake for that 7-day menu to see the immediate effect of the swap.

In other words, this wasn’t a real-world experiment measuring levels in children over time — it was a nutritional analysis of what would happen to nutrient intake if milk was fully replaced in the diet, based on the nutrient content of the drinks.

Doctors Urge Parents to Rethink Plant-Based Drinks for Toddlers

A 2021 commentary published in JAMA Pediatrics reviewed recommendations on plant-based beverage intake for infants and young children and found widespread agreement among health authorities: most plant-based drinks are not suitable substitutes for cow’s milk in children younger than 2.3

• Most pediatric guidelines advise against plant drinks for toddlers — Across high-income countries, including the U.S., Canada and Australia, official dietary guidance strongly advises parents not to use plant-based beverages as replacements for milk in kids under 2.

• Frequent or total replacement of milk with plant-based drinks is a red flag for nutrient deficiencies — Doctors were urged to ask parents directly how often plant-based drinks are used and whether they fully replace cow’s milk. This is because frequent substitution raises the risk of serious nutritional gaps.

• Dozens of real-world cases showed serious consequences from plant-based diets in infants — A report cited in the commentary examined 30 case studies of infants and toddlers, ranging from 4 to 22 months old, who were fed plant-based drinks, either by themselves or along with foods like fruits and vegetables.

All of the children developed serious nutrition-related illnesses, including rickets (caused by soft, weakened bones), scurvy (a result of vitamin C deficiency), protein deficiency or metabolic alkalosis, a dangerous condition that disrupts the body’s acid-base balance and impairs breathing and organ function.

• Soy contains antinutrients — Although soy drinks have the highest protein content among plant-based options, soy’s bioavailability — or how much protein the body actually uses — is reduced by plant-based antinutrients.

Why Soy Formula Is One of the Worst Choices for Your Baby

If you’re relying on soy infant formula as a dairy-free alternative, you need to know what that decision means for your baby’s long-term health. Soy infant formula is often promoted as a safe option for lactose-intolerant individuals or vegan households, but research says otherwise.

• Soy formula changes the way DNA works in babies — A study published in the journal Environmental Health Perspectives looked at girls who were fed soy formula.4 Researchers found differences in DNA tags, specifically in vaginal cells, compared to girls who were fed cow’s milk formula.

These DNA tags are like tiny switches that tell genes whether to be active or inactive. In this study, the tag affected a gene that responds to the hormone estrogen. This is a significant concern because hormones like estrogen are important for how girls’ bodies develop, especially their reproductive systems.

• So, why is soy such a problem? Soy milk and soy formula contain significantly more phytoestrogens — plant compounds that mimic estrogen in the body — than cow’s milk or breast milk. No developing child should be exposed to that level of hormonal disruption.

Plant-Based Milk Is Just Another Ultraprocessed Food

It’s also important to realize that plant-based drinks are ultraprocessed foods, meaning they’ve been heavily modified from their original form and typically contain additives like gums, emulsifiers, synthetic vitamins and artificial flavorings. While many people switch to plant-based drinks thinking they’re more natural, the processing involved strips away beneficial compounds and introduces additives your child doesn’t need.

• Eating ultraprocessed plant foods increases your disease risk — A study published in The Lancet Regional Health Europe followed 126,842 people and examined the health impact of different types of plant-based foods.

While every 10% increase in whole, unprocessed plant foods, like fruits and vegetables, lowered cardiovascular disease risk by 7% and heart disease-related death by 13%, plant-based ultraprocessed foods had the opposite effect. Each 10% increase in these foods was linked to a 5% higher risk of heart disease and a 12% increase in the risk of dying from it.5

• Cow’s milk is a minimally processed whole food with real health benefits — Unlike ultraprocessed plant drinks, milk from grass fed cows is naturally rich in essential nutrients and requires minimal processing — especially when it’s raw.

Whole milk contains healthy fats, protein, calcium and fat-soluble vitamins in a form your child’s body can actually use. It’s a complete food, not a lab-engineered imitation. When you compare ingredient labels, it becomes obvious which product is closer to what nature intended.

Whole-Fat Dairy Delivers Rare Nutrients That Support Total-Body Health

Whole dairy products from grass fed cows are a primary source of odd-chain saturated fatty acids (OCFAs). These unique fats are not produced by your body and must be obtained through food.

• Unique dairy fats are linked to lower risks of chronic diseases — Higher blood levels of OCFAs have been associated with reduced risks of Type 2 diabetes, cardiovascular disease, obesity, fatty liver, inflammation and even overall mortality.6 You don’t get these benefits from almond, soy or oat drinks.

• Raw, grass fed milk boosts gut and immune health naturally — When sourced from organic, pasture-raised cows, raw milk also offers living enzymes, beneficial bacteria and immune-supporting compounds that support digestion and help protect against illness. That’s something no ultraprocessed product delivers. Just be sure to choose milk from farmers who don’t use iodine-based disinfectants to avoid excess iodine in your child’s diet.

What to Do if Your Toddler Is Drinking Plant-Based Milk

If you’ve been giving your toddler plant-based drinks thinking they’re just as good as — or better than — cow’s milk, you’re not alone. It’s a common choice, especially if you’re avoiding dairy yourself or assuming organic almond or oat milk is safer. But as you’ve seen in the research, most of these drinks don’t supply the nutrients your child needs to grow strong and stay healthy. The good news? It’s easy to fix this starting today by making a few changes.

1. Stop using plant-based drinks as milk replacements — Avoid using plant-based drinks in place of real milk. This is especially important during the growth window between 12 and 24 months. Most of these drinks lack the calcium, B12 and B2 toddlers need — and they don’t absorb nutrients from plants as easily as from milk. Plus, soy milk adds another layer of risk due to exposure to estrogenic compounds that affect reproductive development.

2. Avoid using soy, oat, almond or other plant-based drinks as a base for infant formula — If you’re formula-feeding or supplementing, I do not recommend using commercial infant formula — especially not soy-based. Absolutely nothing compares to breast milk in terms of nutrition, so if you are a new mother and still lactating, breastfeeding is the best choice for both you and your child. However, I understand that not all moms can breastfeed.

In this case, I recommend making your own infant formula using this recipe based on nutrient-rich animal foods like raw grass fed cow’s milk, organic raw cream and grass fed beef gelatin. For children who are unable to tolerate milk proteins, I recommend trying this hypoallergenic meat-based formula instead.

If you’ve already been giving plant-based drinks daily, don’t panic. The body responds quickly to good nutrition. The sooner you make the switch, the more support you give your child’s bones, brain and immune system during the years they need it most.

FAQs About Plant-Based Milk for Toddlers

Q: Are plant-based milks safe for toddlers as a replacement for cow’s milk?

A: No. Most plant-based drinks fail to provide the essential nutrients found in cow’s milk. These include calcium, vitamin B12 and vitamin B2, and iodine, all of which are needed for proper growth, brain development, and immune function during early childhood.

Q: What makes soy infant formula risky?

A: Soy formula exposes infants to high levels of phytoestrogens, which are plant compounds that mimic estrogen. Research has shown that girls fed soy formula have altered DNA tags in estrogen-sensitive genes, which could interfere with reproductive development. Soy also contains antinutrients that reduce the body’s ability to absorb protein and minerals.

Q: What’s the problem with plant-based milks being ultraprocessed?

A: Ultraprocessed foods are heavily altered and often loaded with gums, emulsifiers and synthetic nutrients. A study found that plant-based ultraprocessed foods were linked to a 5% higher risk of cardiovascular disease and a 12% increase in death from heart disease. In contrast, unprocessed whole foods, like raw, full-fat milk, lower disease risk and support total-body health.

Q: How does raw, grass fed milk support gut and immune health in toddlers?

A: Raw milk from grass fed cows contains natural enzymes, beneficial bacteria and immune-boosting compounds that are destroyed during pasteurization. These elements support healthy digestion, nutrient absorption and immune function. It’s a living food, unlike plant-based drinks that rely on synthetic additives to mimic nutrition. Choosing raw milk from farms that avoid iodine-based disinfectants also prevents unnecessary iodine overload in your child’s diet.

Q: What’s a better alternative for my toddler?

A: If breastfeeding is not an option, homemade infant formula made from raw grass fed milk, raw cream, beef gelatin and other whole ingredients is a far better choice than any store-bought soy or plant-based formula. If your toddler cannot tolerate cow’s milk, a meat-based hypoallergenic formula is a safer and more nutrient-dense option.

What happens to your platelets when you eat high-fat foods?

They become less active, contributing to cancer cell growth

They shrink, making it harder for cancer cells to spread

They become overly sticky, helping cancer cells attach to organs

High-fat foods activate your platelets, making them overly sticky. This stickiness helps cancer cells attach and grow rapidly in vital organs like your lungs, promoting cancer spread. Learn more.

They multiply, boosting your immune system against cancer

Louisiana’s Senate passed five tort reform bills last week to curb legal system abuse driven by billboard attorneys in the Pelican State. The legislative success represents the culmination of sustained advocacy efforts – including a Triple-I-backed awareness campaign, StopLegalSystemAbuse.org – to build public support.

The new legislation addresses Louisiana’s longstanding challenges with high insurance premiums and the state’s reputation for being plaintiff-friendly in civil litigation. The reforms include stricter limits on damages, clearer standards for expert testimony, and other procedural changes designed to restore balance to the courts while reducing financial burdens on Louisiana families and businesses.

However, an additional measure intended to change state regulations for approving rate filings for auto and home insurance overshadowed the positive actions taken by lawmakers, the Times-Picayune reported.

House Bill 431, which would prevent drivers who are at least 51 percent at fault in an accident from receiving any compensation for their own injuries, requires final House approval due to Senate amendments. So do Senate Bill 231, which would allow insurers’ lawyers to present jurors with the actual amount paid for medical bills, rather than the total billed, and House Bill 436, which would ban undocumented immigrants injured in car accidents from receiving general (non-economic) damages.

House Bill 434, which would increase the threshold from $15,000 to $100,000 for uninsured drivers to collect medical expenses for bodily injuries in accidents, and House Bill 450, which would require plaintiffs in car accident lawsuits to prove their injuries were actually caused by the accident, are awaiting Gov. Jeff Landry’s signature.

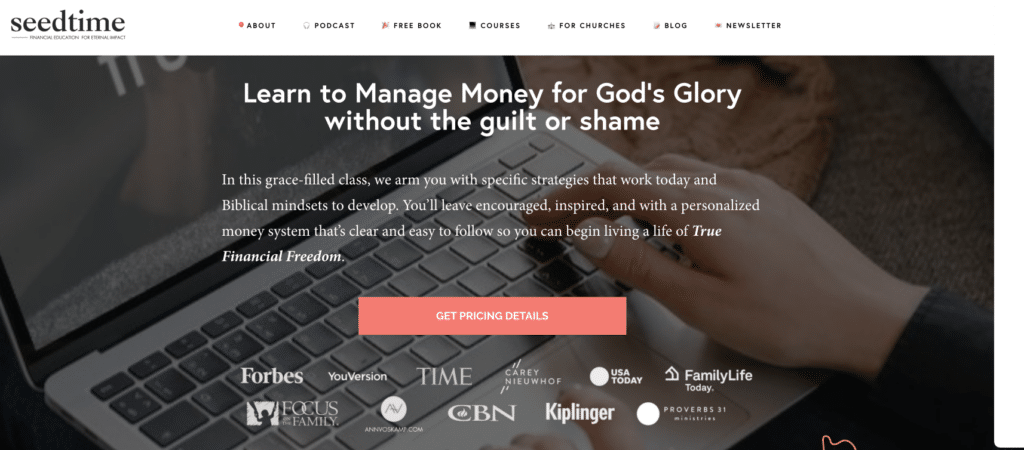

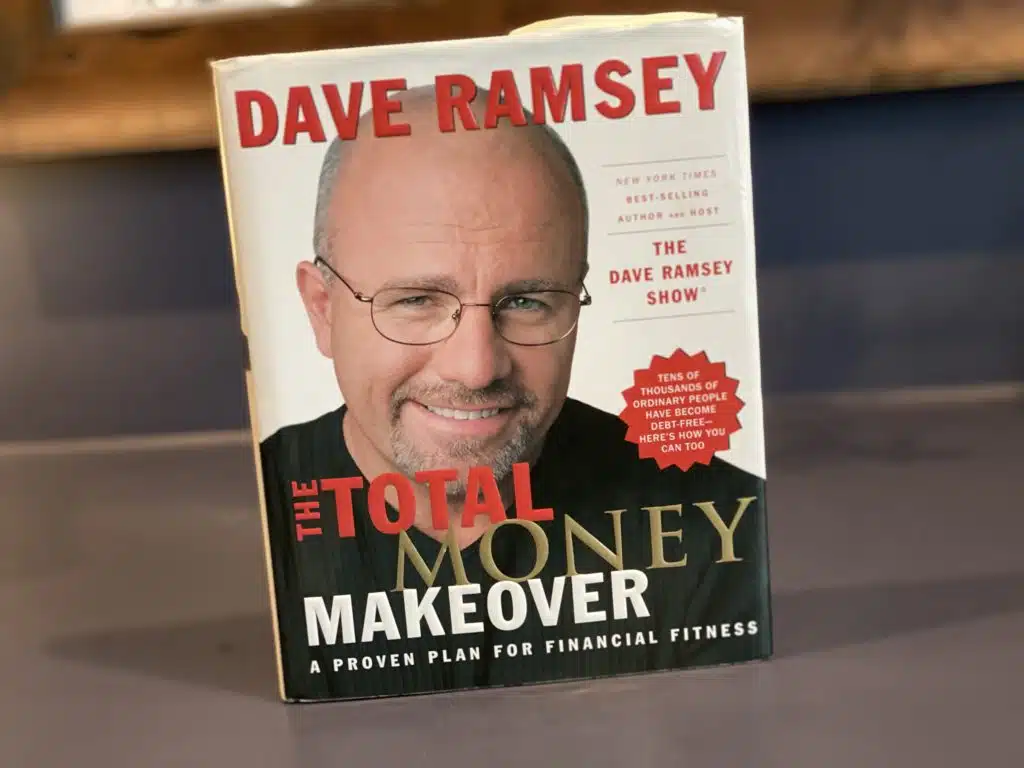

Home » Debt » Financial Peace University vs. True Financial Freedom vs. Crown Financial MoneyLife

I recently completed three of the top Christian financial education programs for churches: SeedTime’s True Financial Freedom, Dave Ramsey’s Financial Peace University, and Crown Financial’s MoneyLife.

These popular programs all claim to help you get control of your finances from a biblical perspective. However, they go about it in different ways with varying teaching styles and philosophies.

In this post, I’ll provide an in-depth look at each program – breaking down the unique features, strengths, weaknesses, and what’s actually included when you buy in.

My goal is to give you the real deal on these courses so you can determine which one (if any) is the best fit for transforming your financial life in a way that aligns with your faith. Whether you’re deep in debt, building wealth, or simply trying to honor God with your money, this comparison will help guide your journey.

Let’s dive into the nitty-gritty details of each program:

Pricing

When it comes to pricing, Financial Peace University from Dave Ramsey sits in the middle. For an individual membership, it’s $69.99. They also offer bulk pricing for churches starting at around $800 for 10 memberships.

On the higher end, Seedtime’s True Financial Freedom charges $149 for an individual/couple license with regular deals making it available as low as $74. But they have some solid deals for Churches – you can get a bulk student license for as low as $48 per person if you buy multiple licenses. Or there’s an annual church subscription starting as low as $750 per year based on average attendance.

The most affordable option is Crown Financial’s MoneyLife course at just $29.95 for an individual purchase. I couldn’t find any publicly listed bulk pricing for churches, but being a non-profit, I’d expect them to be the cheapest route for congregations.

But as you’ll see, there are plenty more differences beyond just the price tags when comparing what’s actually included in each program.

True Financial Freedom (SeedTime)

True Financial Freedom, created by Bob Lotich and his wife Linda from SeedTime, is a financial literacy video course designed for churches that strikes a beautiful balance between biblical wisdom and practical money management strategies. The program’s goal is to equip Christians with the tools and mindset they need to experience true financial freedom while making an eternal impact for God’s Kingdom.

One of the standout features of True Financial Freedom is the engaging and relatable teaching style of Bob and Linda. They share their own financial struggles and triumphs with humor, transparency, and grace, making participants feel like they’re learning from wise, caring friends rather than aloof experts. This approach creates a safe, non-judgmental environment where participants can openly discuss their financial challenges and celebrate their progress.

The program offers several unique benefits, such as the “Never 100” rule (their ‘done-is-better-than-perfect’ approach to adjust spending) and the “Straight A” strategy for automating finances. These concepts are not only memorable but also highly actionable in helping participants take control of their money and build lasting wealth.

Another strength of True Financial Freedom is its emphasis on creating a personalized financial strategy. Through interactive workshops, participants are guided in developing a custom blueprint that fits their unique situation, goals, and values. This approach recognizes that there’s no one-size-fits-all solution to personal finance and empowers participants to take ownership of their financial journey.

True Financial Freedom is perfect for Christians who want to learn how to thrive financially while staying grounded in the Bible. The program teaches participants how to avoid the extremes of being “so heavenly-minded they’re no earthly good” or becoming so focused on building worldly wealth that they lose sight of what truly matters.

With its grace-filled approach and practical tools, True Financial Freedom helps Christians find the balance needed to change their financial life and make a lasting difference in the world in the process.

Included:

6 on-demand video sessions (around 60 mins each)

Printable worksheets, tools, and calculators (physical workbook also available)

Access to their Real Money Budgeting course (their popular (un)Budgeting approach)

Interactive exercises and a workshop-style approach

Course Outline:

Hope & Vision – Find new hope for your finances through Biblical financial principles, break free of defining your worth by your net worth.

Design Your Blueprint – Learn the building block for your new plan, the “Never 100” rule to control income/spending.

Straight A Strategy – Automate your finances using a simple 4-step ‘set it and forget it’ process.

Earn More – Unlock your God-given gifts and talents to earn more in the digital era.

Eternal Impact – Redefine giving as an eternal investment and epic adventure (not an obligation).

Multiply & Enjoy – Simple investing strategies that can change your life, your family, and the world.

Financial Peace University (Ramsey Solutions)

Financial Peace University, created by Dave Ramsey and his team at Ramsey Solutions, is a highly popular financial education program that has helped countless individuals and families get out of debt and build wealth. The program’s primary goal is to guide participants through a proven, step-by-step approach to taking control of their money and achieving financial peace.

Dave Ramsey, the face of Financial Peace University, is known for his high-energy, tough love teaching style. He delivers hard-hitting truths about money with a sense of urgency and conviction that inspires participants to take action. However, some may find his approach a bit intense or even abrasive at times, likening it to going through bootcamp. While this style resonates with some, it may not be everyone’s preferred learning environment.

The cornerstone of Financial Peace University is the “Baby Steps” system, a clear, prescriptive plan for getting out of debt and building wealth. The program heavily emphasizes the debt snowball method, which involves paying off debts from smallest to largest, regardless of interest rates. This approach has proven highly effective in keeping participants motivated and helping them experience quick wins on their debt-free journey.

While Financial Peace University does incorporate some biblical principles, its overall approach is more secular in nature. The program focuses primarily on the practical nuts and bolts of money management, with less emphasis on exploring the deeper spiritual implications of financial stewardship.

Financial Peace University is best suited for individuals and families who are drowning in debt and need a clear, actionable plan to get back on track. The program’s structured approach and intense motivation can be a lifeline for those feeling overwhelmed by their financial situation. However, those seeking a more personalized, grace-filled approach that deeply integrates biblical wisdom may find other programs more appealing.

Included:

9 video lessons walking through the 7 Baby Steps

1 year access to the video lessons

3 months access to EveryDollar budgeting app

Group financial coaching for 1 year

1 free one-on-one coaching session

Digital workbook

Course Outline:

Baby Step 1 & Budgeting – Build your $1,000 emergency buffer and gain control through budgeting

Baby Step 2 – Learn the debt snowball method to eliminate all non-mortgage debt fast

Baby Step 3 – Save 3-6 months’ expenses for a fully-loaded emergency fund

Baby Steps 4-7 – Invest 15% for retirement, save for college, pay off home, build wealth

Wise Spending – Outsmart marketing tactics to curb impulsive spending

Understanding Insurance – The 8 essential and unnecessary insurance types explained

Building Wealth – Simplify retirement investing to build lasting wealth

Buying & Selling Your Home – Avoid mortgage missteps – rent vs buy wisdom

Outrageous Generosity – Discover the joy of outrageous generosity

MoneyLife (Crown Financial)

MoneyLife, offered by Crown Financial, is a financial education program that takes a deeply biblical approach to money management. The program’s primary goal is to guide Christians in understanding and applying God’s financial principles to their lives, emphasizing the importance of seeing God as the ultimate provider and owner of all resources.

One of MoneyLife’s distinguishing features is its strong focus on biblical teachings and spiritual practices related to money. The program dives deep into exploring how our financial decisions can reflect our faith and values, encouraging participants to align their money management with biblical principles. This emphasis on the spiritual aspects of finance sets MoneyLife apart from other programs that may focus more heavily on practical strategies.

The teaching style in MoneyLife tends to be more academic and classroom-like compared to other programs. Participants can expect a significant amount of reading materials and written assessments throughout the course. While this approach may appeal to those who prefer a studious learning environment, it may not be as engaging for individuals who thrive on interactive, video-based content.

MoneyLife offers some unique elements, such as personality assessments that help participants understand how their natural tendencies impact their financial decisions. The program also includes exercises like the transfer of ownership, which guides participants in acknowledging God’s ultimate ownership of their resources. These introspective activities can be powerful tools for reshaping participants’ mindsets and habits around money.

However, one potential drawback of MoneyLife is that its emphasis on biblical principles and spiritual practices may come at the expense of providing highly actionable, practical financial strategies.

MoneyLife is ideal for Christians who are seeking a deeply biblical understanding of money management and are willing to engage in a more studious, reflective learning process. The program is well-suited for those who want to explore the spiritual foundations of financial stewardship and align their money habits with their faith. However, those primarily looking for a simple and easy financial strategy or a more interactive learning experience may find other programs that better fit their needs.

Included:

10 self-paced video lessons

MoneyLife Indicator financial assessment

Lots of reading materials, PDFs, homework

Course syllabus and schedule

Spiritual practices like prayer logs

Course Outline:

MoneyLife (Crown Financial)

Unwavering Hope – Find unshakable hope in God as the true provider

The Plan – Develop a realistic spending plan aligned with God’s perspective

Ditching Debt – Achieve debt freedom using biblical truth and practical tools

Saving – Set short and long-term savings goals to steward resources well

Investing – Build an investment portfolio to create a legacy of generosity

Good Work – Identify your purpose to experience fulfillment in your career

Generous Living – Overcome obstacles to experience the joy of committed giving

Paying It Forward – Discover strategies to transfer wisdom to future generations

True Riches – Align spending with needs vs. wants to pursue true wealth

The Choice – Commit to choose God’s path for money to experience freedom

Quick Comparison:

Feature

True Financial Freedom (SeedTime)

Financial Peace University (Ramsey)

MoneyLife (Crown Financial)

Goal

To give Christians a Biblical framework and practical tools so they can manage money wisely, experience true financial freedom, and make an eternal impact for God’s Kingdom.

To help individuals and families get out of debt, build wealth, and take control of their money using a proven, step-by-step approach.

To guide Christians in understanding and applying God’s financial principles, seeing Him as the ultimate provider, and aligning their finances with Biblical values.

Approach

-Strikes an effective balance between biblical wisdom and practical, actionable guidance. -Helps you manage money in a way that honors God and sets you up to thrive financially.

-Heavily focused on getting out of debt using a proven system of “Baby Steps”. -Incorporates some biblical principles but is more secular in its overall approach.

-Leans deeply into the biblical and spiritual side of money management. -Emphasizes seeing God as the ultimate provider.-Can feel a bit more theoretical at times.

Teaching Style

-Engaging, relatable, and empowering (feels up-to-date with the modern ‘YouTube’ era of online learning). -Real-life stories with humor and grace, making the course feel like a conversation with wise, caring friends.

-A lot of energy and motivation, but his style can come across as a bit harsh or stern at times, which doesn’t resonate with everyone. -Comes across as more of a lecture than a workshop.

-More academic and classroom-like, with a heavy emphasis on reading materials and assessments. -May not be as engaging for all learning types.

Personalization

-The interactive workshop style guides you in creating a personalized money strategy tailored to your unique situation and goals. -No one-size-fits-all plans, you build a blueprint that truly fits your life.

-Provides a clear, prescriptive set of “Baby Steps” to follow for getting out of debt and building wealth. -While proven, it may not allow as much flexibility for individual circumstances.

-Offers some helpful personalized tools like the MoneyLife Indicator assessment-Emphasis on “God as provider” means the program has a very specific outline to achieve that goal which may feel rigid.

Unique Benefits

-The simple “Never 100” rule for a done-is-better-than-perfect approach to saving. -“Straight A” strategy for automating your finances. -A strong focus on leveraging your unique God-given talents to increase your income. -Eternal Impact as the ultimate goal (giving, investing in the Kingdom, etc..)

-Iconic “debt snowball” method for accelerating debt payoff and staying motivated. -Access to EveryDollar budgeting app. -Financial coaching resources.

-Scripture memory-The “transfer of ownership” exercise to help align your mindset and habits with biblical financial principles. -Personality assessment to find and leverage your gifting.

Perfect for…

-Those who want to learn how to truly live and thrive in the ways of the Kingdom (not being so heavenly-minded that they’re of no earthly good, but also not getting caught up in building their own earthly kingdom) -A grace-filled, practical approach to experience true financial freedom and make an eternal impact!

-Individuals and families who are drowning in debt and need a clear, proven, step-by-step plan to get out of debt and start building wealth, with some biblical grounding and intense motivation.

-Those who desire a deeply biblical exploration of God’s role in our finances, with a focus on spiritual practices and mindset shifts. -Those who don’t mind a more academic, reading-heavy approach.

Personal Experience and Recommendations

Having gone through all 3 programs, here is my personal experience and recommendations:

I can honestly say that True Financial Freedom was a life-changing experience. Bob and Linda’s warm, relatable teaching style made me feel like I was learning from trusted friends who truly cared about my success. The program’s emphasis on creating a personalized financial strategy was a game-changer for me, as it helped me develop a plan that fit my unique situation and goals.

The “Never 100” rule and “Straight A” strategy have become cornerstones of my financial habits, helping me live below my means and automate my savings and giving. It was perfect for someone like myself who didn’t want a complicated, jargon-filled financial class – and wasn’t going to sign up for an intense ‘shame & blame’ session either.

Personally, True Financial Freedom struck that balance better than any of the other programs on the list and gave me the strategy to move forward. My savings, giving, and earning have all increased in significant ways since taking the program.

For those who are drowning in debt and need a clear, structured plan to get out, I highly recommend Financial Peace University. Dave Ramsey’s no-nonsense approach and the step-by-step “Baby Steps” system can provide the motivation and direction needed to tackle debt head-on. The debt snowball method, in particular, has helped countless people experience quick wins and build momentum on their debt-free journey. Just be prepared for a more intense, boot camp-style learning environment.

If you’re seeking a program that deeply explores the biblical principles behind money management, Crown’s MoneyLife might be the right fit for you. The program’s emphasis on spiritual practices and aligning your finances with your faith can be incredibly powerful for those who want to grow in their understanding of God’s perspective on wealth. However, be prepared for a more academic, reading-intensive learning experience and less focus on highly practical, actionable strategies.

Ultimately, the best program for you will depend on your unique financial situation, learning style, and personal goals. If you’re looking for a grace-filled, practical approach that helps you thrive in God’s Kingdom while making an eternal impact, I highly recommend True Financial Freedom. If you need a structured, intensive plan to get out of debt fast, Financial Peace University could be your best bet. And if you desire a deep dive into the biblical foundations of money management, MoneyLife is worth considering.

Regardless of which program you choose, the most important thing is to take action and invest in your financial education. By doing so, you’ll be better equipped to handle the resources God has entrusted to you and experience the joy and freedom that comes from aligning your finances with your faith.

Starbucks is hiring a “Captain – Pilot-in-Command” for its company Gulfstream aircraft.

According to the job posting, the role pays between $207,000 and $360,300 a year. (Business Insider notes that theaverage airline pilot earned around $250,000 in 2024.)

“The captain is one of the company’s most visible representatives to the passengers and serves as a Starbucks ambassador both at home and abroad,” the listing reads. “They model Starbucks’ guiding principles and act with tact and decorum, while providing the utmost in service and safety.”

Starbucks reportedly has at least two Gulfstream G550 jets.

While the job description doesn’t specifically say you’ll be helping the CEO get to the office so he can comply with the company’s return-to-office policy standards, it wouldn’t be a far-fetched idea. It’s been widely reported that Starbucks CEO Brian Niccol commutes over 1,000 miles multiple days a week from Newport Beach, California, to Starbucks’s headquarters in Seattle, Washington.

A Gulfstream G550 from a private company (not Starbucks) lands at Barcelona airport in Barcelona, Spain, on August 30, 2024. Smith Collection/Gado/Getty Images

The pilot role has numerous responsibilities, including managing the flight and crew. Applicants should have a valid Airline Transport Pilot Certificate, a current 1st Class Medical Certificate, an FCC Restricted Radio Operator Certificate, and other FAA-based requirements.

Candidates should also have at least five years of experience operating as a captain with a corporate flight department and at least 5,000 hours of flight time, plus other certificates. See the job listing for the full slate of required items.

When you’ve coached as long as I have, you end up learning a lot of lessons. But most of them didn’t come from certifications, courses, or textbooks.

They came from experience—coaching others, coaching myself. And honestly? From getting things wrong more than once.

One thing I look back on now and think, What was I thinking?! is something I used to believe was helpful…

Something I saw a lot of other coaches do, too: using exercise as a form of punishment.

Ever trained a little harder after a weekend of indulgence? Added an extra round at the gym because you skipped a workout yesterday? Felt the need to “make up for” something?

That was exactly the approach I took with clients when I first started out.

You ate more than you were “supposed to” over the weekend? Let’s burn it off. You’re late for your session? Guess what—we’ll make it “hurt” a little more.

It reinforced a message that’s been echoed for decades: No pain, no gain.

Somewhere along the way, movement stopped being a celebration of what our bodies could do and a way to increase their capacity—and started becoming a tool to fix what was “wrong” with them and something we only do when we did something ‘bad.”

Food became the reward. Exercise became the punishment.

And that, right there, is the problem.

Using Exercise as Punishment Changes Everything—Quietly and Deeply

Every time we treat movement as “the stick” for doing something wrong, we plant a seed. A seed that says: Exercise is something to be avoided.

Because no one looks forward to being punished.

Even when a workout isn’t meant to be punishment, that’s the association we’ve built. We’re not moving because we want to—we’re moving because we feel we “have to.” And that’s how something positive becomes something we dread. That’s how we go from wanting to move to forcing ourselves to move.

You can’t build something positive from something your brain has learned to fear.

And then we wonder why we’ve lost the motivation, the energy, the excitement we used to feel.

It Damages Our Relationship With Food—and With Ourselves

In the punishment model:

Cake = extra cardio. Lazy weekend = Monday burpees.

But here’s the truth: Food isn’t something you need to earn. And your workout isn’t a “get out of jail free” card.

It’s also not a solution to cravings or overeating.

When we reinforce that food = guilt and exercise = punishment, we strip away the opportunity to build an empowered, healthy relationship with either.

I remember a client who overindulged almost every weekend. And every Monday, I’d push them through an extra-tough session to “burn it off.”

What I didn’t do? Ask them why it kept happening.

I failed to see that my job as a coach wasn’t just to “make up for” the behavior…

It was to help them understand it. To get curious about what was really going on. To work together to find a more supportive way forward.

We didn’t change anything. We just kept repeating the cycle.

That’s not coaching. That’s damage control.

It Embeds Shame—And Shame Doesn’t Create Lasting Change

Shame might get someone to show up. It might push them to do one more round, one more sprint, one more cleanse.

But it doesn’t build confidence. It doesn’t create consistency. And it definitely doesn’t foster self-trust or long-term motivation.

What it does is make the coach the driver.

Now the client shows up not because they see value in the process—but because they want to avoid guilt, embarrassment, or disappointing someone.

That’s not empowerment. That’s fear.

And when fear is your main motivator, burnout, resentment, or avoidance easily follows.

Shame disconnects us from the why behind movement. It strips exercise of its joy, its purpose, and its real benefits.

Why would we tie something as essential and nourishing as movement to guilt, pain, or performance anxiety?

And more importantly: Shouldn’t we be doing it for ourselves—not to please someone else?

What I’d Tell My Younger Coach-Self Today

I’d tell her:

I know you thought you were helping. But you were reinforcing the same stories your clients already believed:

That they had to earn their right to eat.

That their body was a problem to be fixed.

That being shamed into change was effective.

I’d show her there’s a better way.

Because if a client “slips up” on their eating plan, the solution isn’t to punish them with sweat. It’s to ask:

What made that choice feel like the right one at the moment? How can we support you next time to make a choice that feels more aligned to your goals and values?

If someone misses a week of workouts, the answer isn’t to crush them when they return. It’s to help them reconnect to their why. To remind them what movement does for them—not what it takes from them.

Movement Should Be a Partnership, Not a Punishment

As coaches, our job isn’t just to correct. It’s to get curious. To listen. To guide. To create a safe space for self-discovery. To offer support and accountability—but from a place of respect and compassion, not control.

You don’t need to move to make up for what you did—or didn’t—do.

You move to build something: A stronger body. A calmer mind. A deeper connection with yourself.

That shift—from punishment to partnership—is where real, lasting health begins.

What would you tell your younger self about using exercise as punishment?—Marlene

A Gulfstream G550 from a private company (not Starbucks) lands at Barcelona airport in Barcelona, Spain, on August 30, 2024. Smith Collection/Gado/Getty Images

A Gulfstream G550 from a private company (not Starbucks) lands at Barcelona airport in Barcelona, Spain, on August 30, 2024. Smith Collection/Gado/Getty Images