As with any new technology, as well as the opportunities it opens up, there are concerns about unintended consequences of generative AI and the need for responsible implementation. We were delighted to be in the hotspot usually claimed by Kenneth Saldanha in this episode of Insurance News Analysis to discuss this important topic and were delighted to be joined by Bruce Hentschel, a luminary in the industry.

We discussed a story about a 76-year-old man in the UK who had his claim denied recently after a house fire because he failed to tick a box on his policy application. This unfortunate incident emphasizes the importance of insurers understanding their customers, including the significant changes in population demographics, and designing application processes that effectively convey the significance of the information being collected and how Gen AI can play a role.

We discussed how instead of relying on customers to identify previous claims, generative AI can analyze data and present customers with validated information for confirmation.

We also discussed the opportunity in providing insurance policies to cover the ways in which generative AI can go wrong. Responsible AI is the key to harnessing the power of generative AI while mitigating risks. Insurers must keep humans in the loop and use AI as a tool to drive insights, automation, and higher levels of service. Learning from the framework of cyber insurance, insurers can focus on specific types of losses initially and gradually expand coverage as the market evolves. Striking a balance between risk management and leveraging the capabilities of generative AI is crucial for long-term success.

Disclaimer: This content is provided for general information purposes and is not intended to be used in place of consultation with our professional advisors.

Disclaimer: This document refers to marks owned by third parties. All such third-party marks are the property of their respective owners. No sponsorship, endorsement or approval of this content by the owners of such marks is intended, expressed or implied.

Increased legislative involvement in regulating homeowners’ insurance pricing and rates – as recently called for by some officials in Illinois – would hurt insurance affordability in the state, rather than helping consumers as intended, Triple-I says in its latest Issues Brief.

Rising premiums are a national issue. They reflect a combination of costly climate-related weather events, demographic trends, and rising material and labor costs to repair and replace damaged or destroyed property. Average insured catastrophe losses have been increasing for decades, fueled in part by natural disasters and population shifts into high-risk areas. More recently, these and other losses to which the property/casualty insurance industry is vulnerable were exacerbated by inflation related to the pandemic and Russia’s invasion of Ukraine. Tariffs and changes in U.S. economic policies have since put even more upward pressure on costs.

These increasing costs – if not addressed – threaten to erode the policyholder surplus insurers are required to keep on hand to pay claims. If surplus falls below a certain level, insurers have no choice but to increase premium rates or adjust their willingness to assume risks in certain areas.

To avoid this, many insurers have filed with state regulators for rate increases – requests that often meet with resistance from consumer advocacy groups and legislators. Illinois would not be the first state to try to ease consumers’ pain by constraining insurers’ ability to accurately set coverage prices to reflect increasing levels of risk and costs.

Practicality, not politics

Such efforts, while perhaps politically popular, confuse one symptom (higher premiums) of a growing risk crisis with its underlying cause (increasing losses and rising costs). Using the blunt instrument of legislation to address the complexities and sensitivities of underwriting and pricing would tend to disrupt the market and further hurt insurance affordability – and, in some areas, availability.

Rather than target insurers with misguided legislation, the brief says, states would be wiser to work with the industry to improve their risk profiles by investing in mitigation and resilience. The brief describes the causes of higher premium rates nationally and in Illinois and how other states have successfully collaborated to address those causes and reduce upward pressure on – and eventually bring down –premium rates.

“Triple-I welcomes the opportunity to collaborate with state policymakers to develop constructive approaches to risk mitigation and resilience that will benefit communities and consumers,” the brief says.

Four senior executives are departing United Services Automobile Association (USAA) as the financial services company undergoes organizational restructuring, the company announced.

The executives leaving include Brandon Carter, president of USAA Life Insurance Co.; Ameesh Vakharia, executive vice president and chief strategy and brand officer; Amala Duggirala, executive vice president and chief information officer; and Tom Troy, executive vice president and chief transformation officer.

USAA described the leadership changes as part of meeting evolving member needs. “Leadership change – to meet the evolving needs of our members and the association – is a natural occurrence in any large, dynamic organization,” the company said in an email statement, as reported by BestWire.

The company did not provide information about potential successors for the departing executives.

New member value organization created

As part of the restructuring, USAA established a “member value organization” primarily led by military veterans “to ensure everything we do begins and ends with the member in mind,” according to the company.

Several functions across USAA are being moved under this new organizational structure. The company stated it maintains “a deep bench of qualified senior leaders,” with some executives being reassigned to different areas within the organization.

USAA membership is restricted to military members, veterans, and their close family members.

The restructuring comes after a year of significant financial growth for USAA. The company’s annual attributable net income in 2024 tripled to $3.89 billion from $1.21 billion in the previous year, driven by revenues increasing more than losses, benefits, and expenses.

Total assets rose to $220.58 billion, primarily due to strong investment performance and increased property/casualty premiums, according to a BestWire report.

USAA ranked as the third-largest homeowners’ multiperil insurer and fifth-largest all-private passenger auto insurer in the United States in 2024, based on direct premiums written, according to BestLink data.

What are your thoughts on the latest announcement? Share your insights in the comments below.

The legal profession has experienced many transformations over the past year, but perhaps none as dramatic as the fundamental shift in how legal professionals approach insurance coverage. In a stunning reversal from previous years, 45% of legal professionals are now upgrading their insurance policies, a staggering jump from just 14% who had such plans in 2024. While other law firm trends have surprised us this year, this one may take the cake.

This shift reflects a reimagining of how legal professionals view protection, risk, and strategic business planning. The law firm trends from our 2025 Legal Risk Index reveal a profession that is shifting from reactive coverage purchasing to proactive risk management, treating insurance not as a necessary operational expense but as a strategic enabler of growth and innovation.

From Underinsured to Strategic

The shift is remarkable when viewed against the backdrop of previous years. Legal professionals historically reported feeling underinsured while simultaneously lacking concrete plans to address coverage gaps. The industry appeared caught in a cycle of knowing they needed better protection but struggling to translate that awareness into action.

That cycle is showing signs of breaking. The threefold increase in professionals upgrading their policies signals a major change in how legal professionals understand the relationship between protection and opportunity. This appears to be driven by the recognition that comprehensive insurance coverage doesn’t constrain business growth; it enables it.

The confidence level accompanying this shift is equally striking. An impressive 77% of legal professionals now express confidence that their current insurance policies cover their greatest business risks, representing a dramatic improvement in both coverage adequacy and professional awareness of what that coverage actually provides.

The Perfect Storm of Awareness

So, what drove this trend? It appears to be a combination of factors that created both urgency and opportunity for coverage enhancement.

The rapid adoption of AI technologies, jumping from 22% to 80% usage among legal professionals, introduced new liability exposures that existing policies may not have adequately addressed. As firms began integrating AI tools into their daily operations, the potential for professional liability claims related to over-reliance on technology or data privacy breaches became real concerns rather than theoretical risks.

Simultaneously, the shift in internal risk priorities from financial pressures to reputational and employment-related challenges highlighted coverage areas that many firms had previously overlooked or undervalued. Employment practices liability insurance, for instance, gained new importance as workplace-related claims tied for the top internal risk at 47%.

The economic stabilization that allowed legal professionals to focus beyond immediate financial survival also created the foundation for strategic insurance planning. With inflation concerns dropping from 52% to 28% as a primary worry, firms could redirect attention and resources toward comprehensive risk management rather than crisis-driven cost cutting.

Cyber Insurance: From Optional to Essential

Perhaps nowhere is the insurance awakening more evident than in the evolution of cyber insurance coverage. The data reveals a dramatic shift in both awareness and implementation of cyber protection, with uncertainty about coverage dropping significantly across the profession.

In previous surveys, 23% of legal professionals admitted they didn’t know if their current insurance policies would cover against data breach risks. That figure has plummeted to just 3% in 2025, indicating not just improved coverage but enhanced understanding of what protection firms actually have in place.

The percentage of firms without dedicated cyber insurance has also dropped, from 22% to 14% year-over-year. More significantly, the number of legal professionals who believe their policies would fully cover against cyber risks has increased from 26% to 33%, while those confident in partial coverage jumped from 30% to 50%.

This reflects the legal profession’s recognition that cyber threats aren’t hypothetical future concerns but present-day operational realities. The integration of AI tools, increased digital operations, and the sensitive nature of legal information have made cyber insurance as fundamental to law firm operations as malpractice coverage.

Does your law firm use AI?

In this webinar with Reminger Law Firm and Everest, we explore the use-cases of AI in legal practice, the best tools for the job, the risks, and the benefits for lawyers.

One of the most intriguing aspects of this trend is its correlation with increased risk-taking behavior among legal professionals. Rather than being defensive reactions to perceived threats, coverage upgrades appear to be enabling bolder business strategies.

The data reveals that 37% of legal professionals now view risk as a growth opportunity, more than doubling from the 18% who held this perspective just one year prior. This shift toward embracing risk coincides directly with the expansion of insurance coverage, suggesting that comprehensive protection is providing the confidence foundation that enables strategic risk-taking.

This dynamic represents a sophisticated understanding of risk management that goes beyond simple loss prevention. As a result, legal professionals seem to increasingly view insurance coverage as a strategic asset that enables them to pursue opportunities they might otherwise avoid due to potential downside exposure.

The correlation extends to AI adoption as well. The dramatic surge in AI usage from 22% to 80% occurred alongside the insurance coverage expansion, with many firms likely recognizing that new technologies require new protections. Rather than avoiding AI due to liability concerns, legal professionals appear to be addressing those concerns through enhanced insurance coverage while proceeding with strategic implementation.

Strategic Coverage Planning

This insurance trend has created opportunities for legal professionals to approach coverage planning more strategically than ever before. The key is understanding that insurance purchasing decisions should align with business strategy rather than simply meeting minimum requirements or industry standards.

Successful coverage planning begins with comprehensive risk assessment that goes beyond traditional categories to include emerging threats like AI liability, reputational damage, and evolving employment practices exposures. This assessment should consider not just current operations but planned business developments and growth strategies.

The correlation between insurance coverage and risk-taking behavior suggests that coverage decisions should be integrated into strategic planning processes rather than treated as separate administrative functions. Firms planning to expand AI usage, enter new practice areas, or pursue aggressive growth strategies should ensure their insurance programs can support those initiatives.

Regular coverage reviews have become essential given the rapid pace of change in both legal practice and risk exposure. The legal professionals who are thriving in the current environment are those who treat insurance as a dynamic business tool rather than a static protection mechanism.

Law firm trends 2026: Looking Forward

This trend positions legal professionals to navigate future challenges with greater confidence while pursuing opportunities that might previously have seemed too risky to attempt. The firms that have embraced this are building competitive advantages that extend far beyond simple loss protection.

The correlation between enhanced insurance coverage and increased business confidence suggests that the awakening will continue to drive positive business outcomes for legal professionals who understand insurance as a strategic enabler rather than a necessary cost.

This shift represents just one facet of how legal professionals are fundamentally reimagining their relationship with risk, transforming protection strategies while embracing unprecedented opportunities for growth and innovation.

Read the complete Legal Industry’s 2025 Risk Index to access comprehensive insights, detailed coverage analysis, and strategic recommendations for navigating the evolving legal landscape with confidence and competitive advantage.

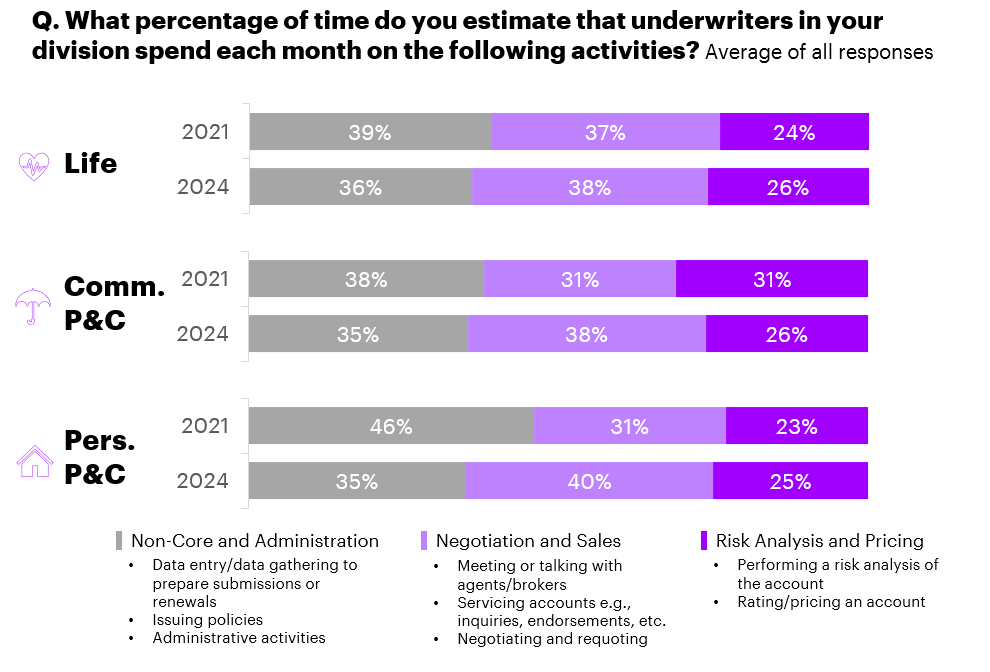

We have periodically conducted surveys on underwritingformore than 15 years to understand the state of the function and how technology is—or isn’t—helping it to evolve. In our most recent reportUnderwriting rewritten, we asked what percentage of time underwriters are spending on non-core tasks. This time, we saw some incremental improvement year–over–yearcompared to our 2021 survey but still more than a third of an underwriter’s time is spend on non-core activities such as data collection or administrative activities.

But more than that, our 2024 survey overall expresses the hope for the future that new automation and AI technologies could help change the role of underwriting and truly reduce the time spent on non-core tasks.

I’ve been around long enough to remember other waves of new ideas and technologies such as knowledge management, the internet of things, and analytics. And while each has found a place within the overall insurance business and technology ecosystem, one could argue that none truly changed the underwriting function entirely. But in all the time that we have done our industry surveys over my 30-year career, I personally have never seen numbers like this:

Embracing automation and AI

According to the data above, the percentage of time underwriters spend on non-core tasks is set to decrease much more than just incrementally with AI and automation going forward. Across Life, Group, Personal, and Commercial Insurance, insurance executives are convinced that AI and automation tools will change underwriting significantly and will change it relatively quickly.

Over the last 3 years carriers have been experimenting with these technologies—doing e.g., pilots in data collection, data synthesis, and advice for underwriting. And while not all of these pilots might have been successful, the overall conclusion seems to be now that this time there is a justification for optimism in tackling the non-core share of actuarial tasks. In fact, if you aren’t pursuing some sort of AI Underwriting driven strategy already, then you are probably already behind according to our survey.

Here are some key data points from our recent Underwriting Executive Survey:

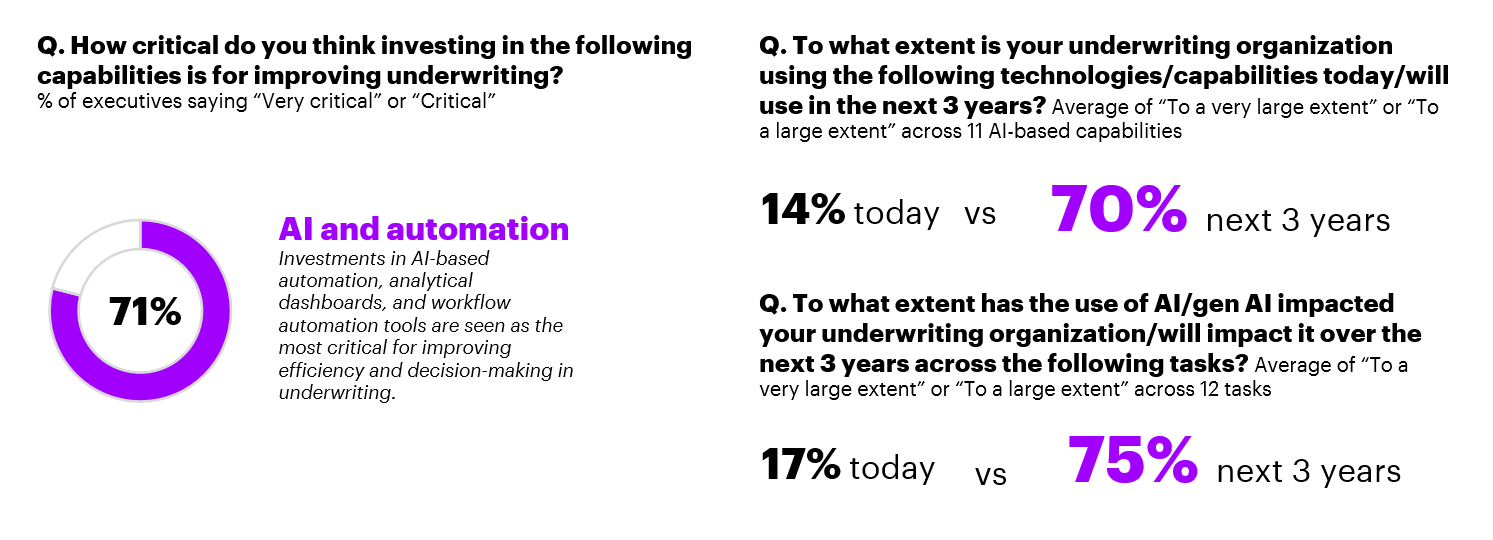

81% of underwriting executives surveyed believe AI and gen AI will create new roles “to a large extent” or “to a very large extent”.

65% of executives believe their workforce will require upskilling as AI becomes integral to creating new roles and augmenting existing ones.

42% of executives think they will need to access external talent pools to fully leverage the potential of the technology

Empowering the AI-led underwriter

Combined with modern automation tools and advanced data ingestion capabilities, AI is perhaps the most transformative force in modern underwriting, balancing both efficiency and complexity within controlled areas. It can enable natural language processing to interact with customers and brokers to address issues and to understand requests so that they can be routed to the correct solution automations. Advanced decision elements and pattern recognition also allow for processing of a wider array of self-service requests without direct intervention. Plus, AI has the ability to orchestrate automations to provide complete self-service solutions.

Let’s be clear: the underwriting role isn’t going away, but it will be transformed as each carrier charts the best way to blend human plus machine decision-making to improve both the speed and efficiency of underwriting outcomes.

Your next steps as gen AI augments your workforce

To be successful in any AI journey, carriers need to be thinking through three things from my perspective:

An AI-led strategy that lays out a plan for taking advantage of these new tools within your existing environment. It needs to be grounded in a strong digital core. As AI technology evolves to become more agentic, underwriters could even enhance their productivity further by breaking down their workflow and delegating tasks to these AI agents.

A talent strategy that reimagines work and is redesigning workflows to prepare management teams and underwriting organizations to take advantage of the new capabilities these solutions provide. A skills-based approach will be key and in tandem, insurers will need to align AI integration with process reinvention, ensuring responsible AI principles are adhered to throughout.

A culture that is able to explore and experiment while protecting core decision making. Insurers probably need to take a bottom-up rather than a top-down approach to AI adoption, capitalizing on employee willingness and eagerness to experiment with AI.

If you want to learn more about Accenture’s Insurance Underwriting Executive Survey, explore at Underwriting rewrittenor feel free to reach out to me directly.

By William Nibbelin, Senior Research Actuary, Triple-I

Motor vehicle tort cases in federal and state courts generated $42.8 billion in “excess value” from 2014 to 2023, according to new analysis by Triple-I.

“Excess value” may sound like a good thing, but it’s not. It represents an additional cost of motor vehicle civil litigation – above and beyond what it would have been if prior trends in court filings had continued. From 1995 to 2007, filings declined, and from 2007 to 2014 they were flat.

The report illustrates the impact of litigation inflation on insurance premiums for all drivers. It also underscores the challenges related to accurately quantifying and comparing state-by-state experience.

Lawsuits push premium up

As Triple-I has previously reported, litigation trends are a major force driving up auto insurance premiums. As claims costs rise – whether due to rising repair costs, litigation, or other factors – premiums must increase to ensure that insurers have enough policyholder surplus to pay future, higher claims.

Policyholder surplus is not a nice-to-have extra. It is the money state regulators require insurers to maintain so they will be able to keep their promises to pay policyholders. In addition, credit rating agencies expect insurers to keep even larger surpluses than the states mandate to enable the insurers to borrow at more favorable interest rates when needed.

Interestingly, motor vehicle tort settlement amounts appear to have decreased on average between 2014 and 2023. While actual settlement amounts are not reported, the “amount in controversy” – legalese for the amount demanded by the plaintiff – serves as a proxy for filings disposed as settlements. The average amount in controversy decreased from $748,000 in the first of the three decades under consideration to $674,000 in the third.

However, the increased volume of cases during the period drove the overall excess value to $984.6 million at the federal level alone.

State courts present a challenge

The report estimates that state courts handled approximately 5.0 million motor vehicle tort cases from 2014 to 2023, generating an excess value of $41.8 billion – dwarfing the federal court impact. This analysis, however, is challenged by the state-by-state variety of definitions and criteria for data collection.

“Because states maintain different definitions and criteria for data collection, most state civil case data is either unavailable or incomplete,” the report says.

The report concludes that its findings align with previous research by Triple-I and the Casualty Actuarial Society, which quantified increasing inflation on auto liability insurance at $118.9 billion for 2014-2023, representing both litigation and economic inflation.

“As we continue to analyze the evolving landscape of motor vehicle litigation, it’s clear that a deeper, data-driven understanding of both national and state trends is crucial,” said Patrick Schmid, Triple-I’s chief insurance officer. “Only with more transparent and comprehensive data can we craft effective solutions that benefit both policyholders and the broader insurance market. Future research should focus on bridging the gaps in state-level information and exploring the causal factors behind rising litigation and its impacts.”

Florida, with nearly 370,000 agents serving a population of 23.4 million, is by far the most crowded market in the country. That’s no surprise – hurricanes, floods, and an aging population drive demand across homeowners, health, and life, representing an interesting opportunity for agents willing to mix personal and commercial lines. Doing so could help to mitigate risk, and cross-selling other lines like life and flood could also help to bolster revenue. But with this high demand comes fierce competition. For agents operating in the Sunshine State, specialization is survival: Medicare Advantage, high-net-worth coastal property, or boutique risk consulting can help you stand out.

Texas, meanwhile, is home to about 355,000 agents and its population is fast growing, at around 2% per year since 2021. Its diverse economy – stretching from energy and agriculture to technology – has become fertile ground for agents able to expand into commercial, special risks, and excess and surplus lines such as oil and gas, construction, and cybersecurity and tech-related risks. These segments are growing in Texas and tend to carry higher margins if agents can navigate the underwriting complexities. Throw in the lack of state income tax – a feature it shares with Florida – and you’ve got one of the hottest markets for agents. Those who can balance commercial and personal lines are especially well-positioned.

California – despite being the nation’s most populous state, with 39.4 million residents – has only 189,035 agents, roughly half as many as Florida. The reason? Growth has slowed, people and businesses are leaving, and insurers are pulling back on homeowners due to wildfire risks and regulatory hurdles. But it’s not all bad news. Agents who can leverage technology and automation to reduce compliance burdens and broaden offerings beyond standard lines can still thrive. Think cyber insurance, pet insurance, or specialty liability to attract diverse client needs and hedge against natural disaster-induced market volatility. It’s less about volume and more about finding value pockets where clients still need trusted advice.

Where agents are scarce

At the other end of the spectrum, states like Alaska and Montana have far fewer boots on the ground compared to the rest of the country, at 2,138 and 2,503 agents, respectively. Even South Dakota, the “biggest” of the small states, only counts 7,134 agents.

As we look ahead to 2024, while we see many challenges for the insurance industry, we meet these with optimism. Insurance is a resilient industry with a deep sense of purpose—offering people, families and businesses protection and a more secure future.

What’s the macro-economic outlook?

Global macroeconomic forecasts for 2024 indicate both slowing GDP growth and continuing inflationary pressure. Talent shortages are most pronounced in the U.S. where unemployment is below 4% overall and hovering around 2% for the insurance sector.

Major markets are feeling consumer sentiment headwinds. Our research shows consumers in the U.S. are largely pessimistic due to lingering recessionary concerns. Meanwhile in the U.K., consumer pessimism is coming from uncertainties caused by recent tax changes and their potential impact on public services.

What can the industry expect?

Top-line revenues for P&C insurance carriers move with GDP. Revenue growth for P&C carriers is expected to slow to 2.6% on average for 2024 and 2025—down from 3.4% in 2023 (Swiss Re Sigma).

On the flip side, the Life insurance segment is seeing stronger demand for savings and retirement products. In emerging markets revenue growth is expected to reach 5.1% on average in 2024 and 2025. This revenue growth may soften the impact of the ongoing profitability and liquidity challenges the segment faces.

Claims volumes and costs across lines of business remain elevated in most major markets. While some of this is inflation-driven and cyclical, systemic risks such as social inflation, increasing NatCat claims and demographic shifts in aging, health and mental health are here to stay.

While we remain optimistic about the insurance industry, the challenges we face going into the year ahead are real. Here are five predictions for 2024:

1. Monetizing AI

Since the launch of ChatGPT this time last year, there has been copious Generative AI discussion and speculation—dare we say hype? The reality is that leading insurers have been on the journey of advancing data, analytics and AI for years. In 2024, we will see excitement about the possibilities of GenAI give way to growing demand for material economic impact from AI/GenAI solutions. Insurers who have invested in data, analytics and AI capabilities will incorporate more GenAI as a natural next step on that journey. They will also need to elevate responsible/ethical usage risk controls as AI takes a more autonomous role.

2. Alternative human capital strategies

AI/GenAI has proliferated to decision support, processes and interactions across the insurance value chain. Fortunately, this comes at a time when the industry is under pressure to address looming workforce gaps in both Underwriting and Claims. In 2024, we will see AI/GenAI treated more as supplementary talent. Insurers will also test sourcing models for “complex” work that was closely held and traditionally developed. Making these changes a reality will require the industry to migrate away from traditional talent development through apprenticeship and standard practices of knowledge management.

3. Cost pressures boil over to drive operating model change

Continued, sustained cost pressures are driving heads of divisions and business units to ask, “Whose fault is it anyway?” In 2024, demands for greater autonomy and direct control of costs will increase as mounting internal frustrations and questions about allocation methodologies of centralized costs (and stranded cost from shifts in the portfolio) boil over.

4. Risk portfolio shifts and capital reallocation

While industry convergence isn’t a new phenomenon, more industry players are looking over the fence for greener pastures in P&C, health and wealth management. Automakers want to offer P&C insurance. P&C carriers are getting into health products and services, and health insurers are offering voluntary and supplemental benefits. For many insurers, the greenest pasture is in the retirement space. Millennials and Gen Z will become the beneficiaries of the greatest wealth transfer in history over the next two decades. Their values-driven approach to investing will disrupt retirement and create new opportunities for Life/Annuities carriers who offer a value proposition in alignment with their values.

5. Service revenues climb while risk capital declines

To raise RoE and ease demands on capital as new loss patterns drive up indemnity and volatility, insurance carriers will go beyond traditional product offerings and deeper into advice/services. Tele-health, care navigation and risk mitigation services will become a greater area of focus for carriers in 2024 and beyond.

GenAI has taken the world by storm. You can’t attend an industry conference, participate in an industry meeting, or plan for the future without GenAI entering the discussion. As an industry, we are in near constant discussion about disruption, evolving market factors – often outside of our control (e.g., consumer expectations, impacts of the capital market, continued M&A) – and the most optimal way to solve for them. This includes use of the latest asset / tool / capability that has the promise for more growth, better margins, increased efficiency, increased employee satisfaction, etc. However, few of these solutions have achieved success creating mass change for the revenue generating roles in the industry…until now.

Technology has largely been developed to drive efficiencies, and if properly adopted, there have been pockets of achievement; however, the individuals required to use the technology or enter in the data that powers the insights to drive the efficiencies are often the ones who reap little to no benefit from the solution. At its core, GenAI has increased the accessibility of insights, and has the potential to be the first technology widely adopted by revenue generating roles as it can provide actionable insights into organic growth opportunities with clients and carriers. It is, arguably, the first of its kind to provide a tangible “what is in it for me?” to the revenue generating roles within the insurance value chain giving them not more data, but insights to act.

There are five key use cases that we believe illustrate the promise of GenAI for brokers and agents:

Actionable “clients like you” analysis: In brokerage businesses that have grown largely through amalgamation of acquisition, it is often difficult to identify like-for-like client portfolios that can provide cross-sell and up-sell opportunities to acquired agencies. With GenAI, comparisons can be done of acquired agencies’ books of business across geographies, acquisitions, etc. to identify clients that have similar profiles but different insurance solutions, opening up material insight for producers to revisit the insurance programs for their clients and opening up greater organic growth opportunities powered by insights on where to act.

Submission preparation and client portfolio QA: For brokers and/or agents that don’t have national practice groups or specialized industry teams, insureds within industries outside of their core strike zone often present challenges in terms of asking the right questions to understand the exposure and match coverage. The effort required to identify adequate coverage and prepare submissions can be dramatically reduced through GenAI. Specifically, this technology can help prompt the broker/ agent on the types of questions they should be asking based on what is known about the insured, the industry the insured operates in, the risk profile of the insured’s company compared to others, and what’s available in 3rd party data sources. Furthermore, GenAI can act as a “spot check” to identify potentially overlooked up-sell or cross-sell opportunities as well as support mitigation of E&O. Historically, the quality of the portfolio coverage and subsequent submission would be at the sheer discretion of the producer and account team handling the account. With GenAI, years of knowledge and experience in the right questions to ask can be at a broker and/or agent’s fingertips, acting as a QA and cross-sell and up-sell tool.

Intelligent placements: The risk placement decisions for each client are largely driven by account managers and producers based on level of relationship with a carrier / underwriter and known or perceived carrier appetite for the given risk portfolio of a client. While the wealth of knowledge gained over years of experience in placement is notable, the changing risk appetites of carriers due to near constant changes in the risk profiles of clients makes finding the optimal placement for agencies and brokers challenging. With the support of GenAI, agencies and brokers can compare a carrier’s stated appetite, the client’s risks and policy recommendations, and the financial contractual details for the agency or broker to generate a submission summary. This provides the account team with placement recommendations that are in the best interest of the client and the agency or broker while reducing the time spent on marketing, both in terms of finding optimal markets and avoiding markets where a risk would not be accepted.

Revenue loss avoidance: As clients opt for advisory fees over commission, the fees that are not retainer-specific, but attributed to specific risk management actions to be provided by the agency or the broker often go “under” billed. GenAI as a capability could in theory ingest client contracts, evaluate the fee- based services agreements within, and establish a summary that can then be served up on an internal knowledge exchange-like tool for employees servicing the account. This knowledge management solution could serve specific guidance to the employee, at the time of need, on what fees should be billed based on the contractual obligations, providing a revenue growth opportunity for agencies and brokers that have unknown, uncollected receivables.

Client-specific marketing materials at speed: Historically, if an agent or broker wanted to expand a non-core capability (e.g., digital marketing) they would either hire or rent the capability to get the right expertise and the right return on effort. While this worked, it resulted in an expansion of SG&A that could not be tied tightly to growth. GenAI type solutions offer a solve for this in that they allow an agent or broker scalable access to non-core capabilities (such as digital marketing) for a fraction of the investment and cost and a potentially better outcome. As an example, GenAI outputs can be customized at a rapid pace to enable agencies and brokers to generate industry-specific material for middle market clients (e.g., we cover X% of the market and Z number of your peers) without the timely effort of creating one-and-done sales collateral.

While the use cases we’ve drawn out are in the prototyping phase, they do paint what the near-future could look like as human and machine meet for the benefit of revenue-generating activities. There are three key actions we encourage all of our broker/ agent clients to do next as they evaluate the use of this technology in their own workflows:

Focus on a subset of the data: Leveraging GenAI requires some of the data to be highly reliable in order to generate usable insights. A common misconception is that it must be all of an agent or broker’s data in order to take advantage of GenAI, but the reality is start small, execute, then expand. Identify the data elements most critical for the insight you want and establish data governance and clean-up strategies to improve that dataset before expanding. Doing so will give the private computing models a dataset to work with, providing value for the enterprise, before expanding the data hygiene efforts.

Prioritize use cases for pilot: Like many emerging technologies, the value delivered through executing use cases is being tested. Brokers and agents should evaluate what the potential high value use cases are and then create pilots to test the value in those areas with a feedback loop between the development team and the revenue- generating teams for necessary tweaks and changes.

Evaluate how to govern and adopt: As we discussed, insurance as an industry has been slower to adopt new technology and, as such, brokers and agents should be prepared to invest in the change management and adoption strategies necessary to show how this technology may very well be the first of its kind to materially impact revenue and organic growth in a positive fashion for revenue generating teams.

While this blog post is meant to be a non-exhaustive view into how GenAI could impact distribution, we have many more thoughts and ideas on the matter, including impacts in underwriting & claims for both carriers & MGAs. Please reach out to Heather Sullivan or Bob Besio if you’d like to discuss further.

Get the latest insurance industry insights, news, and research delivered straight to your inbox.

Disclaimer: This content is provided for general information purposes and is not intended to be used in place of consultation with our professional advisors.

Disclaimer: This document refers to marks owned by third parties. All such third-party marks are the property of their respective owners. No sponsorship, endorsement or approval of this content by the owners of such marks is intended, expressed or implied.

Improved loss ratios, strong premium growth, and lower retention rates characterized the U.S. auto insurance industry in 2024, according to LexisNexis® Risk Solutions’ 2025 U.S Auto Insurance Trends Report.

The report shows that, “while a number of insurers returned to profitability as the market softened,” the market was characterized by “record levels of policy shopping and switching, attorney representation, claims severity, and rising driving violations.”

Rate increases over the past two years helped U.S. insurers address profitability issues, the report said. Premium rate increases are beginning to ease, rising 10 percent in 2024, compared with a 15 percent hike in 2023, as market conditions soften. Insurer profitability is improving, with direct written premiums growing 13.6 percent, to $359 billion, and incurred loss ratios stabilizing, enabling some carriers to pursue growth strategies and file for rate decreases.

LexisNexis Risk Solutions also notes that tariffs may factor into how insurers consider rate in 2025. While the market wouldn’t expect the magnitude of activity seen between 2022 through 2024, tariffs, if they stick, could set off a ripple effect of moderate rate increases with implications across the industry.

Other trends identified in the report include:

Bodily injury claims severity jumped 9.2 percent, and property damage severity climbed 2.5 percent, year over year. In contrast, collision severity fell 2.5 percent for the same period.

All driving violations increased 17percent and driving violation rates across the United States surpassed 2019 levels.

Policy shopping reached an all-time high, with more than 45 percent of policies in force shopped at least once by year-end.

The report also noted that electric vehicle (EV) transitions are introducing new risks, as drivers moving from internal combustion engine vehicles to EVs experienced a 14 percet rise in claim frequency.

“Auto insurers continue to navigate a dynamic market,” said Jeff Batiste, senior vice president and general manager, U.S. auto and home insurance, LexisNexis Risk Solutions. “The combination of the market softening and a return to profitability presents a potential new chapter for the industry as insurers encounter a consumer base that is more willing than ever to shop for deals.”

Record levels of auto policy switching translated to 2024’s new policy growth rate of 17.7 percent year over year. It also added momentum to the ongoing customer retention decline across the industry.

Since 2021, retention has decreased five percentage points, to 78 percent, resulting in a 22 percent increase in policy churn, the report says.

“Historically, dropping even one percentage point is significant,” it says. “However, against a backdrop of heightened levels of shopping and switching activity, insurers may want to focus on their retention strategies, especially when long-tenured customers are hitting the market.”