Shark Tank is a reality TV show built around entrepreneurs seeking investments in their companies. Some of these companies go on to achieve success. The worst Shark Tank products went absolutely nowhere and produced nothing but losses for their investors.

Let’s take a look at some of the lemons that Shark Tank has produced: the worst Shark Tank products.

Shark Tank: How It Works

Shark Tank is based on a simple premise. Entrepreneurs bring their business ideas into the Shark Tank and ask for money in return for part ownership of their companies. A panel of investors – the “sharks” – listens to the pitches, analyzes their potential, and decides whether to invest.

Like all TV shows, Shark Tank was primarily developed for entertainment: viewers get a vicarious thrill out of watching entrepreneurs lay their ideas on the line and seeing some shot down and others walking away with hundreds of thousands in new capital.

While Shark Tank is all about entertainment, it has been a way for some entrepreneurs to gain both money and publicity, launching their companies to success. It has also launched some spectacular flops. We’ll look at some of the worst Shark Tank products here.

🦈 Learn more: Explore our roundup of the best Shark Tank products that made it big, from innovative gadgets to groundbreaking services.

The 12 Worst Shark Tank Products

Becoming an entrepreneur isn’t as easy as it might first appear. It’s not enough to have a cool idea and bring it straight to market. You need to fully develop your business plan, research the market, identify your target audience, assess the competition, develop an expansion strategy, test the viability of your product, and more.

These entrepreneurs have failed on at least one of these accounts.

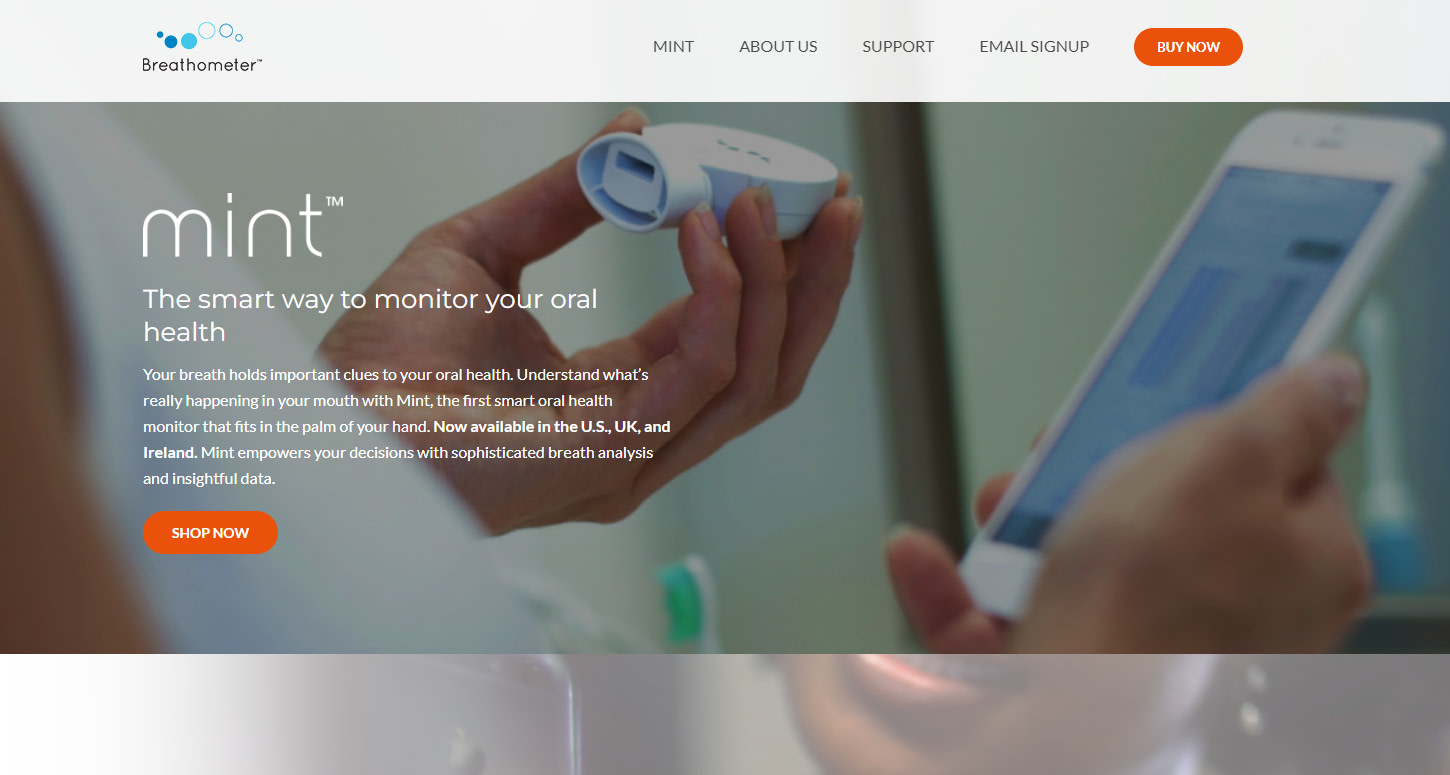

1. The Breathometer (2013)

At first glance, the Breathometer, developed by Charles Michael Yim, seemed like an ingenious idea. Presented in season 5 of the show (2013), the portable breathalyzer could pair up with a smartphone to read the user’s blood alcohol levels.

All five of the sharks decided to invest in it, with Mark Cuban, Lori Greiner, Robert Herjavec, Kevin O’Leary, and Daymond John raising 1 million in exchange for just 30% of the business’s equity.

Problems arose after the investment, though. The business couldn’t meet the heightened demand for the product. The product also failed to meet user expectations, delivering inaccurate results and causing the Federal Trade Commission (FDC) to step in.

It wasn’t long before the Breathometer had to be taken off the market. The idea went down the drain, along with the money invested by the sharks.

💵 Learn more: Explore 5 effective ways to get money to start a business, helping you turn your entrepreneurial dreams into reality

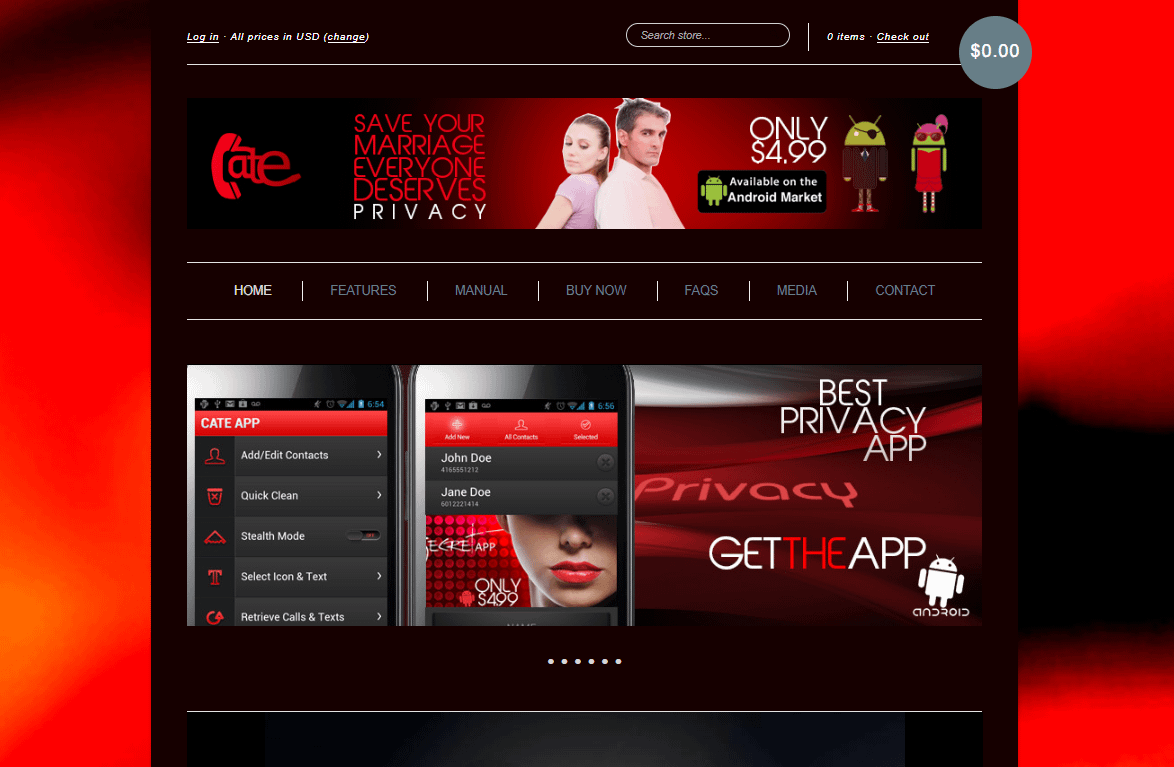

2. CATEapp (2012)

In season 4 of the show (2012), the Shark Tank investors heard a presentation from Neal Desai, inventor of CATEapp. Known as the “cheater’s app”, CATEapp offered the ability to hide messages from select contacts, enabling them to only be seen by the phone’s primary user.

Two of the sharks, Kevin O’Leary and Daymond John, were intrigued enough to raise $70,000 in exchange for 35% equity.

The app got thousands of downloads after its Shark Tank appearance, but it quickly became clear that the app was laden with bugs and leaked sensitive information. Its features could also be circumvented rather easily. Moreover, it couldn’t compete with similar, more reliable apps that came to market.

CATEapp is no longer available for downloads, and the money invested in it is gone, making it one of the worst Shark Tank products.

📱 Learn more: Discover how to make money with your phone using our practical tips and ideas that turn your device into a revenue source.

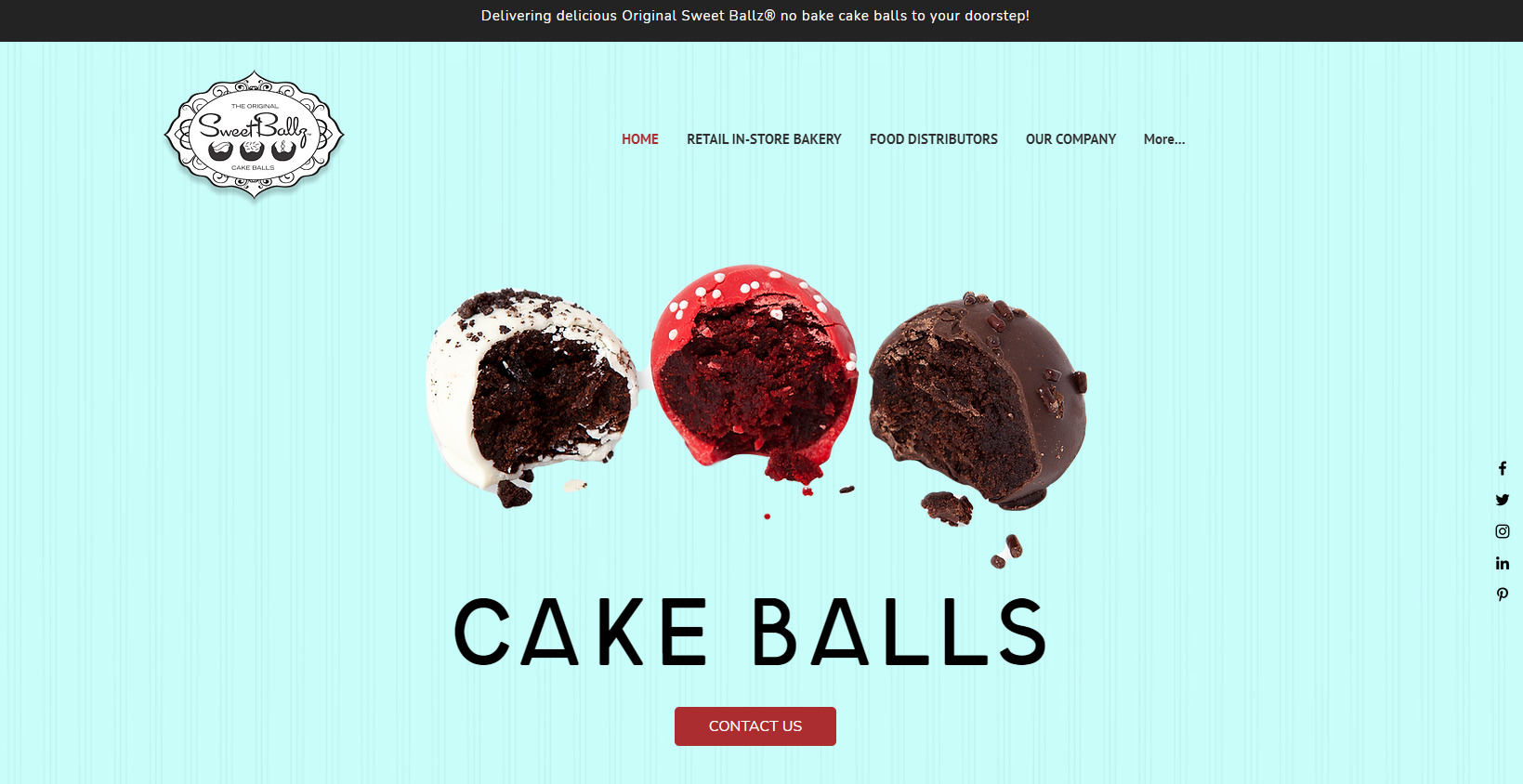

3. Sweet Ballz (2013)

Although the investors in Shark Tank have, on multiple occasions, highlighted how risky investing in food businesses can be, Mark Cuban and Barbara Corcoran jumped at the opportunity to invest in Sweet Ballz.

In season 5 James McDonald and Cole Egger presented their idea: selling delicious little cake balls. The founders received $250,000 in exchange for 25% of their equity, and all was good for a while.

Unfortunately, though, James and Cole had a falling out and even filed for restraining orders against one another.

Sweet Ballz, now run by James, is still in business today, though it’s not nearly as successful as it could’ve been had he and his business partner stayed on the same page. Sweet Ballz may not have been one of the worst Shark Tank products, but it was certainly one of the worst partnerships!

📈 Learn more: Explore the top picks for the best food stocks & ETFs of 2025 to spice up your investment portfolio.

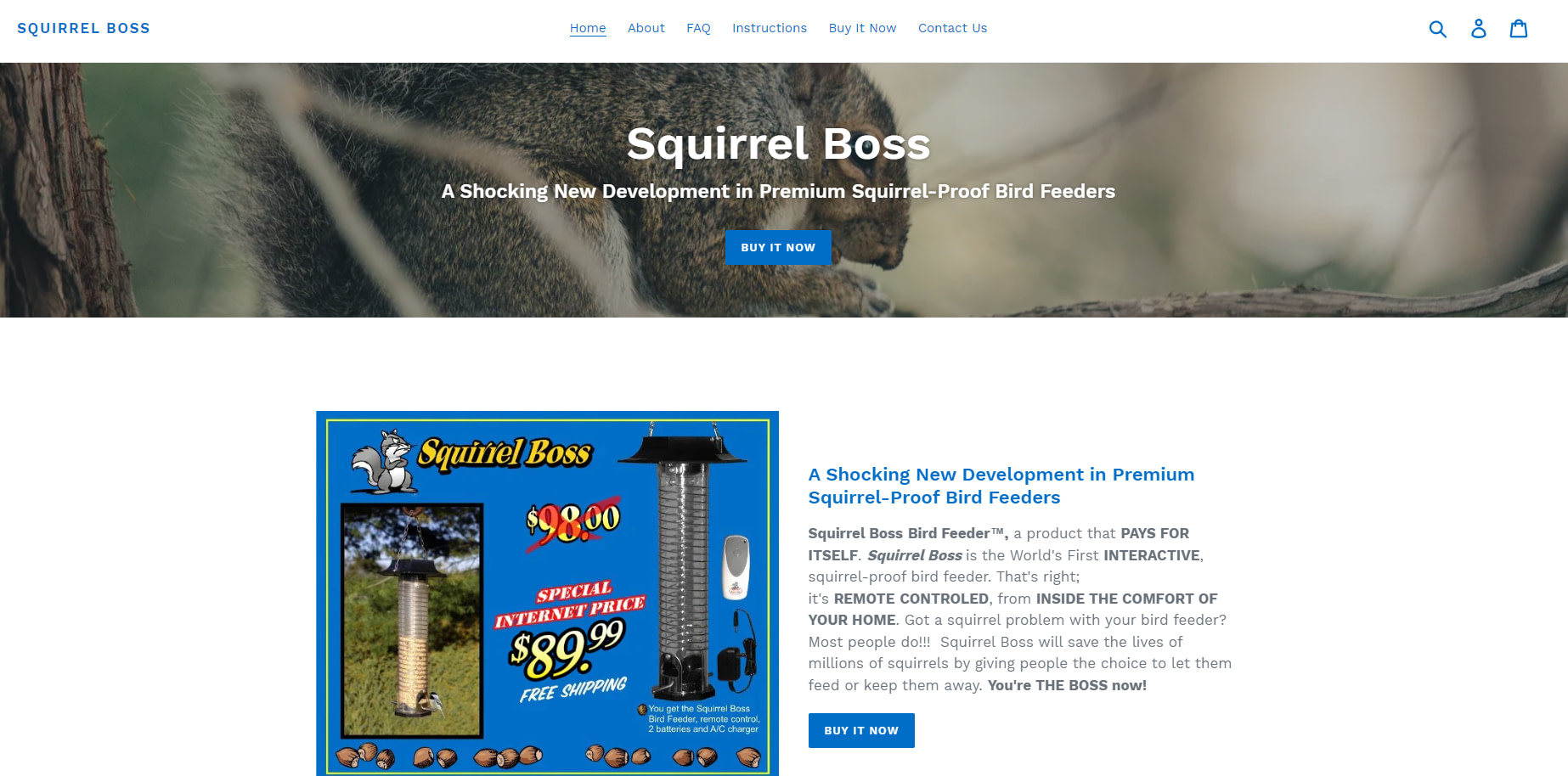

4. Squirrel Boss (2013)

Michael Desanti presented Squirrel Boss in season 4 (2013) of Shark Tank. At its core, it was a simple bird feeder, but it had a feature that would send an electric shock to pests like squirrels to deter them from stealing the bird food. Supposedly, the shock wouldn’t harm the squirrels.

The main problem was that the product couldn’t differentiate between pests and birds and would shock any animal that came into contact with it, a significant design flaw that could hardly be overlooked.

Squirrel Boss was also expensive and unpatented, so none of the sharks were willing to invest in it.

While it was available on Amazon for a while, Squirrel Boss never took off due to its major design flaws and hefty price.

5. Original Man Candle (2011)

The Original Man Candle was the brainchild of Johnson Bailey, who believed that traditional scented candles were too feminine.

Presenting his idea in season 2 of the show, Johnson tried to differentiate his product by introducing more “masculine” scents that would supposedly appeal to the male target audience.

Unsurprisingly, none of the “sharks” were interested in investing in the Original Man Candle. That may have been due to the selection of scents offered, which included “popcorn,” “golf course,” and “flatulence,” or due to the lack of a comprehensive business plan.

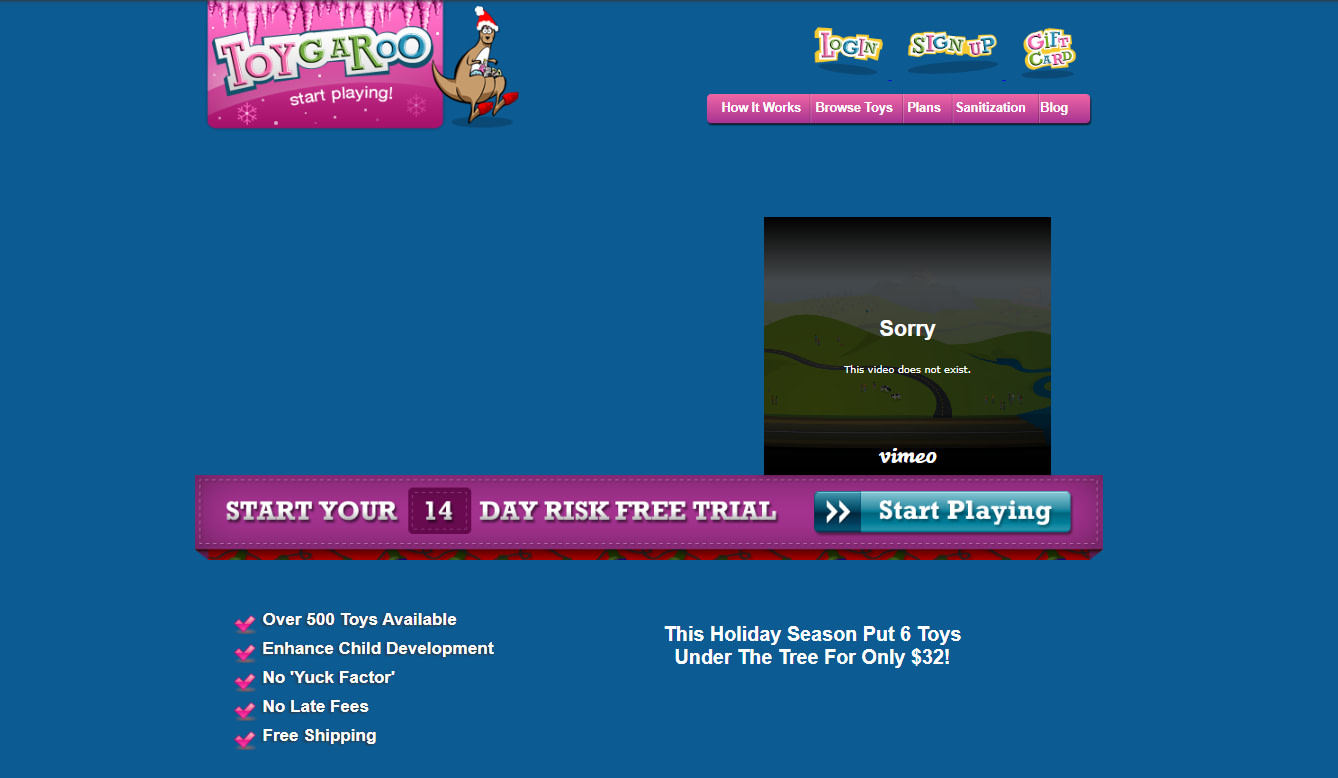

6. ToyGaroo (2011)

ToyGaroo is one of the better-known failures from Shark Tank. Originally presented in season 2 (2011), ToyGaroo was founded by Nikki Pope, Young Chu, Hutch Postik, Phil Smy, and Rony Mirzaians.

The premise behind it was simple. ToyGaroo rented out children’s toys in a subscription-based service. Parents could sign up for the service, rent high-quality toys for a month, return them, and get a new batch, avoiding the problem of spending on toys only to have the kids lose interest.

Mark Cuban and Kevin O’Leary saw the appeal, committing $250,000 to the venture.

However, ToyGaroo wasn’t ready for the heightened demand following the episode’s airing. Sourcing high-quality toys and shipping them proved to be more expensive than anticipated, leading the business to go bankrupt in months.

👉 Learn more: Learn exactly what is bankruptcy and the steps involved in declaring it, in our latest post designed for clarity and insight.

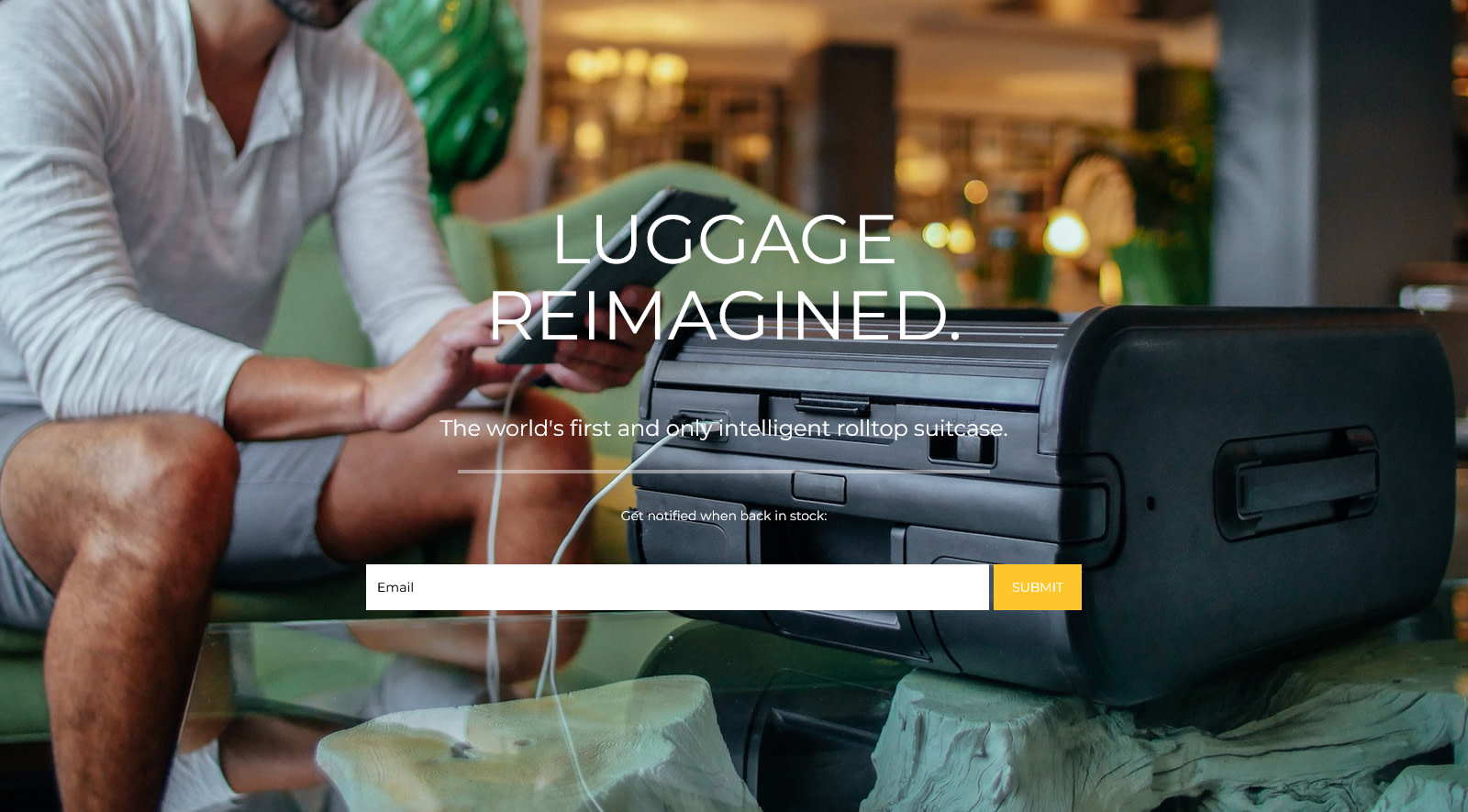

7. Trunkster (2015)

Trunkster was a promising new company that was supposed to disrupt the travel industry. Founded by Gaston Blanchet and Jesse Potash, it brought a new level of technology to a very old product: luggage. The product was a smart suitcase with useful features like a GPS tracking system, USB ports, a digital scale in the handle, and more.

Presented on Shark Tank in season 7, Trunkster caught the attention of Mark Cuban and Lori Greiner, who invested $1.4 million in exchange for 15% of the company.

The deal, however, fell through. Trunkster’s apparent $28 million valuation only came from presales on Kickstarter and Indiegogo and aggressive revenue projections. Most of the customers who signed up for preorders never received their high-tech luggage and those who did received poor-quality products that didn’t meet the expectations set up by Trunkster’s marketing campaign.

💳 Learn more: Explore our top picks for the best no-fee travel credit card options in 2025, perfect for savvy travelers looking to save.

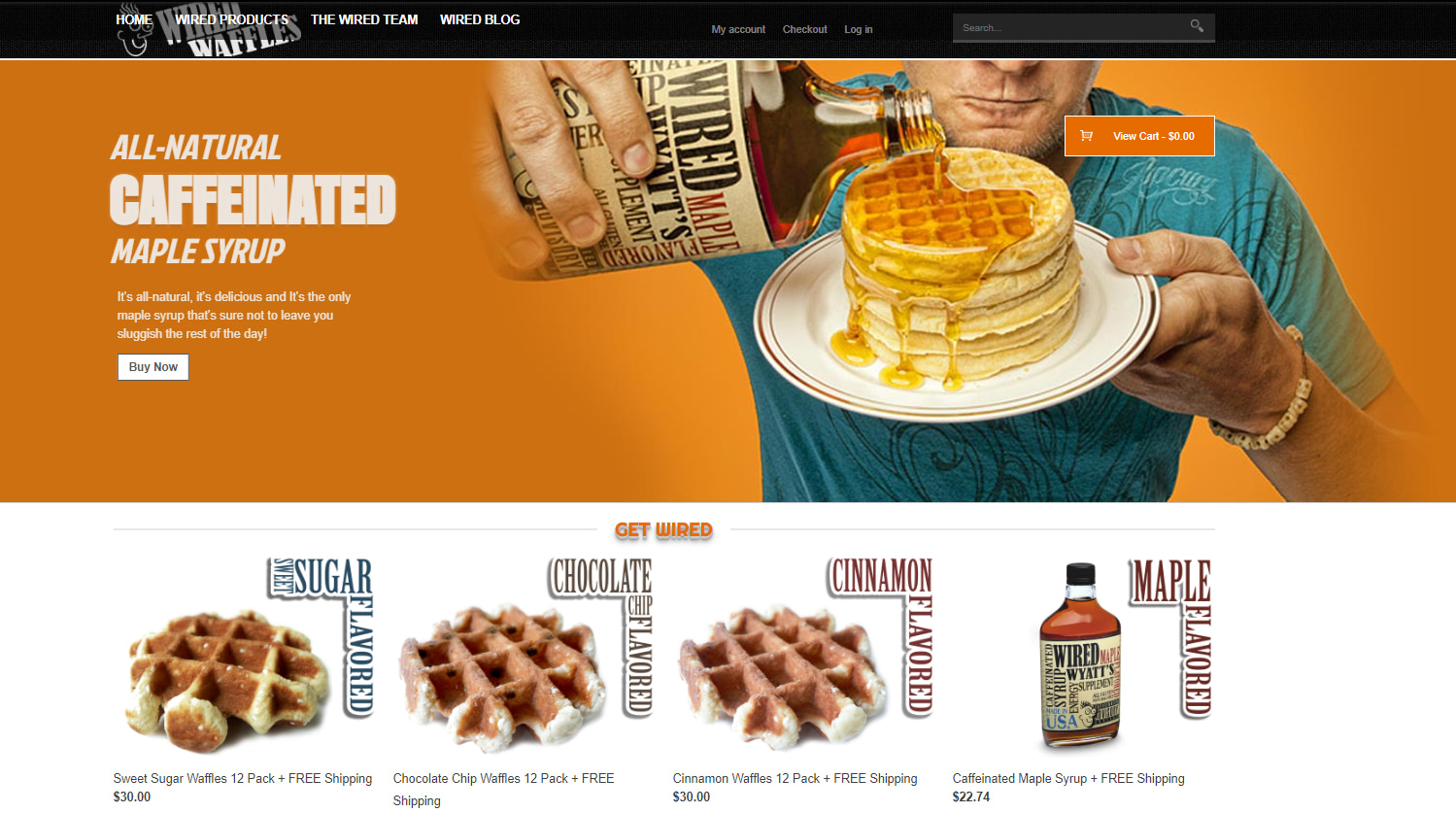

8. Wired Waffles (2012)

Wired Waffles was a flop from the get-go. First presented in season 4 of Shark Tank, the business was founded by Roger Sullivan.

Wired Waffles are caffeine-infused waffles that would supposedly help busy people save time in the morning since they wouldn’t have to make both coffee and breakfast.

None of the sharks were interested in investing in this. After all, caffeine as a simple ingredient couldn’t be patented. The product didn’t have a pleasant taste, and worst of all, it could be ingested by children by accident.

Wired Waffles is a perfect example of what happens when entrepreneurs don’t think their ideas through, fail to test the viability of their products and don’t conduct proper market research.

9. Vestpakz (2014)

Vestpakz seemed like a promising product when it was presented during season 6 of the show (2014). Michael Woolley and Arthur Grayer created it as an innovative new children’s backpack that would reduce the wearer’s back and shoulder pain.

Shaped to look like a vest and boasting plenty of storage space, it seemed like the perfect product. Unfortunately, though, no shark wanted to invest in it.

Despite Vestpakz being available in Walmart stores, the sales were abysmal. The ratio between its manufacturing costs and selling price was too low, and there was minimal consumer demand. Ultimately, Vestpakz went out of business.

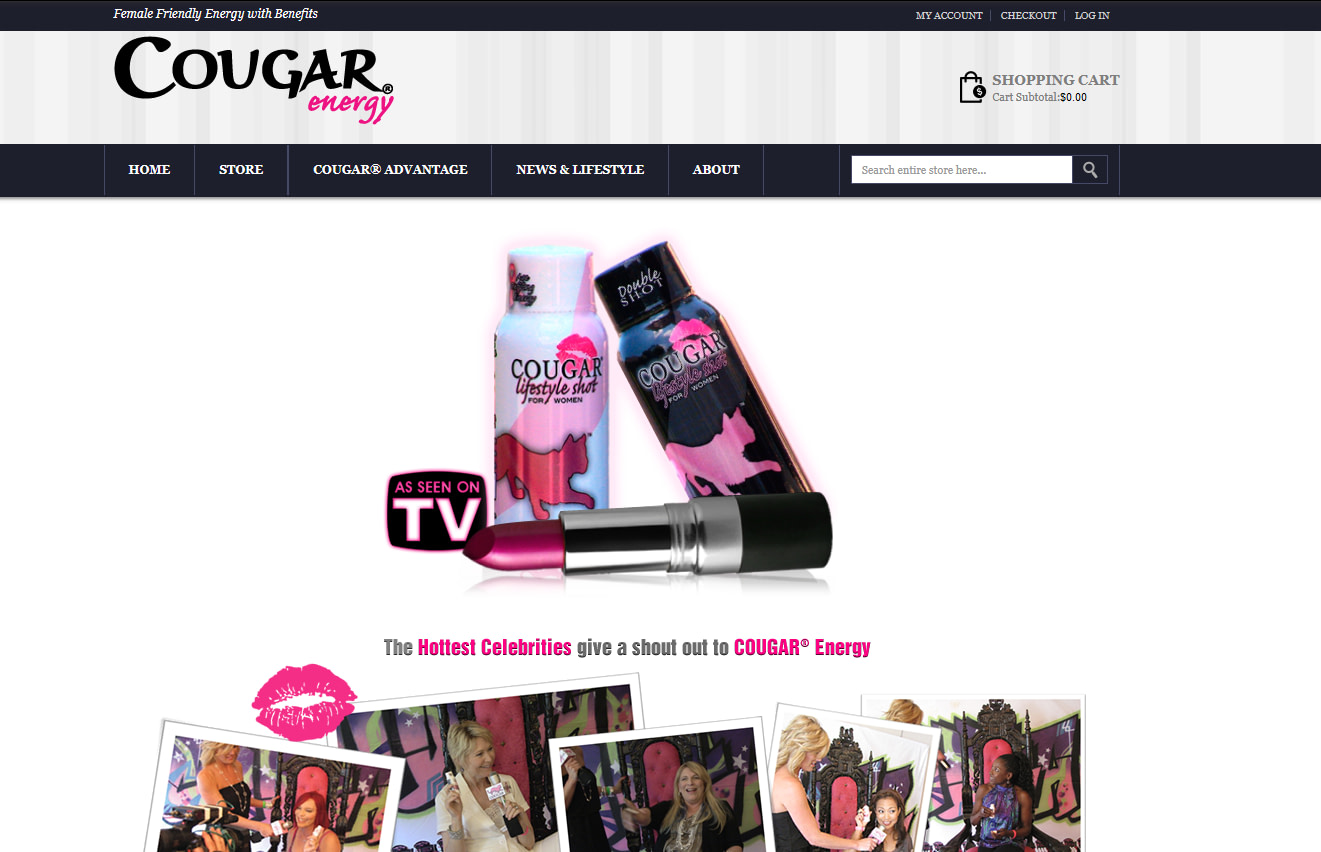

10. Cougar Energy (2012)

Cougar Energy was a product developed by Ryan Custar and presented to Shark Tank investors during season 3 (2012). As its name suggests, it was an energy drink designed for “cougars”, aka middle-aged single women.

Supposedly, the drink wouldn’t only bring the consumer’s energy levels up, but it would also positively affect the hair and nails. Moreover, it boasted “anti-aging” ingredients, though none of these claims were scientifically supportable.

Cougar Energy received no investments in Shark Tank. None of the investors believed there was a market for such a product, nor did they believe it would stand up to competitors. With low sales and plenty of negative comments on Amazon and social media, it was apparent that the investors were right.

11. Wake N Bacon (2011)

Wake N Bacon was first presented by Matty Sallin in season 2 of Shark Tank. It was an alarm clock/oven that would start cooking bacon 10 minutes before wake-up time, thus waking the user up to the sweet smell of bacon.

The concept gained popularity online before Matty came on the show, with plenty of people asking to buy it.

However, the sharks saw it as a gag gift that would have few legitimate users. Moreover, it quickly became apparent that Matty hadn’t thought the whole concept through. There were no safety guards that would minimize fire risks, for instance.

Matty hadn’t come up with a selling price. He hadn’t developed a plan that would help him sell more units after creating a prototype and had no sales projections.

All he had was an idea for a product and no plans to help him market and sell it. Despite many online consumers expressing a desire for Wake N Bacon, the business fell through because there really wasn’t a business there in the first place, just an idea.

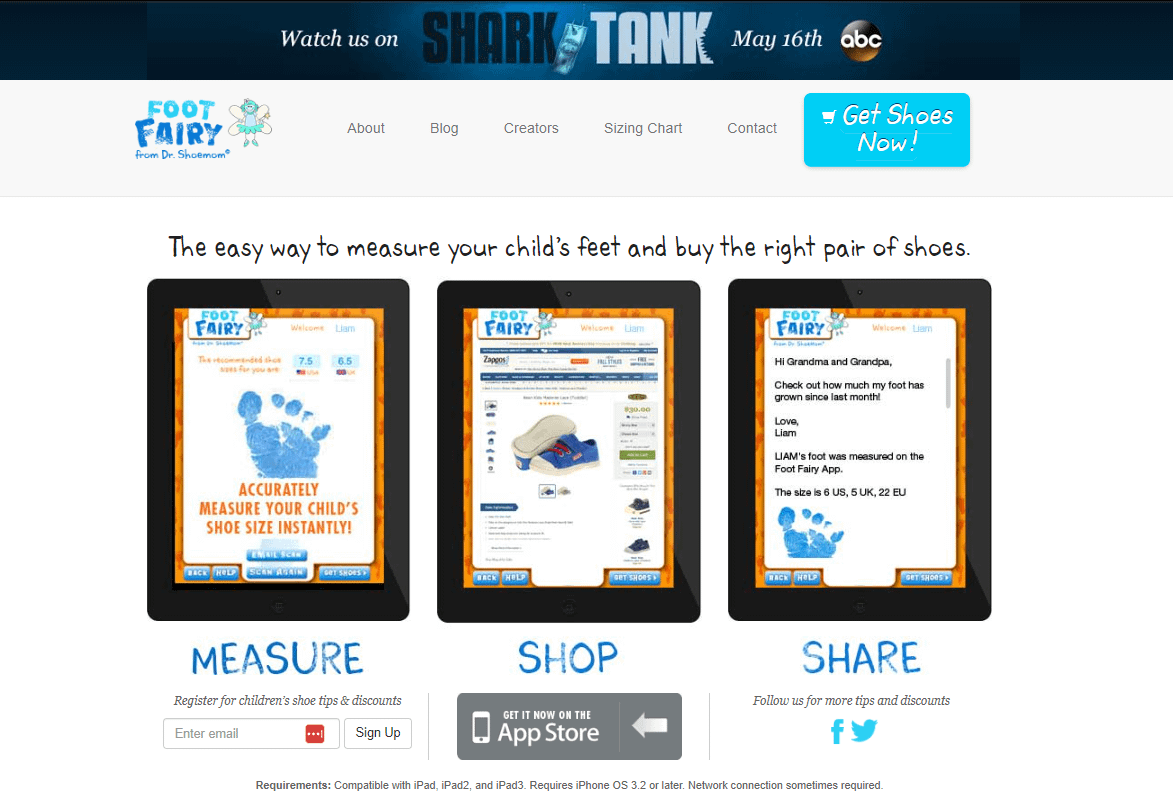

12. Foot Fairy (2013)

Foot Fairy was presented during season 5 of Shark Tank. Inventors Sylvie Shapiro and Nicole Brooks developed an app to help parents measure their children’s feet and buy suitably sized shoes for them, thus minimizing the risks of common foot issues.

Foot Fairy would be free to use, and the company would earn commissions from popular stores like Zappos.

However, despite the app having thousands of downloads prior to Sylvie and Nicole’s appearance on Shark Tank, the two had earned no commissions.

While the concept, at its core, seemed interesting enough, there were a couple of issues that deterred the sharks from investing in it. The app was easy enough to copy, which would deter any major retailers from offering commissions for it. Moreover, it would have been a much more viable business plan for Sylvie and Nicole to develop their own brand of footwear and use Foot Fairy to increase their sales.

Although one of the sharks did offer a deal, it never came to fruition, and Foot Fairy is no longer available.

Conclusion

While there are a couple of outrageous Shark Tank pitches on this list, some would likely have proven to be lucrative had the entrepreneurs developed their ideas better. After all, having a great product idea is never enough to ensure the success of a business. Entrepreneurs always have to conduct thorough market, competitor, and audience research. They need to test their products’ viability, develop expansion strategies, and develop comprehensive business plans if they hope to attract customers and investors.

")

")