Understand what No Claim Bonus in Health Insurance really means, its risks, and why you shouldn’t rely on it as permanent coverage. Simple guide with examples.

When we talk about health insurance, most of us focus on things like premium, network hospitals, or claim settlement ratio. But one term that often excites policyholders is No Claim Bonus (NCB). Many people see NCB as a “reward” for staying healthy and not using their policy in a year.

But there’s a common misunderstanding here – many assume that this bonus becomes a permanent part of their coverage, and that can lead to serious issues later. In this post, let’s dive deep into what NCB really means, why it should not be treated as guaranteed coverage, and how to plan your health insurance accordingly.

No Claim Bonus in Health Insurance: Don’t Rely on It!

What is No Claim Bonus (NCB) in Health Insurance?

No Claim Bonus is a benefit given by insurance companies if you don’t make a claim in a policy year. Instead of giving you cashback or discounts, insurers usually reward you by increasing your sum insured without increasing your premium.

Two common types of NCB:

Cumulative Bonus

Your base sum insured increases by a fixed percentage (like 10% or 20%) every claim-free year.

Usually capped (e.g., up to 50% or 100% of base sum insured).

Discount on Renewal Premium

Instead of increasing the coverage, some policies reduce your premium for the next year.

In India, cumulative bonus is more commonly used in retail health insurance. For instance:

If you have a Rs.5 lakh health cover and get a 20% NCB every year, after 3 claim-free years, your total coverage becomes Rs.8 lakhs (Rs.5 lakhs base + Rs.3 lakhs NCB).

The Common Misconception: Treating NCB as Guaranteed Coverage

Many policyholders think the NCB addition is just like the base sum insured — fixed and permanent. But that’s not true.

NCB is conditional. It stays only as long as you don’t make a claim.

Once you file a claim, the NCB reduces or vanishes depending on the policy terms.

Example:

Let’s say:

Base Sum Insured: Rs.5 Lakhs

NCB Accrued over 2 years: Rs.2 Lakhs

Total Cover: Rs.7 Lakhs

Now, if you claim Rs.1 lakh in the current year, your NCB may reduce or reset. So, next year your cover may drop to just Rs.5 or Rs.6 lakhs — not the Rs.7 lakhs you thought you had.

This is where the real problem begins — people assume they’ll always have Rs.7 lakhs and don’t upgrade their base cover. When a big medical emergency strikes, they face underinsurance.

No Claim Bonus is a floating benefit. It is not guaranteed. If you rely on the NCB to plan your medical expenses or choose a smaller base sum insured thinking NCB will cover you, you’re exposing yourself to unnecessary financial risk.

Even the Insurance Regulatory and Development Authority of India (IRDAI) clearly mentions in its consumer education materials that:

“Cumulative Bonus is a reward and may reduce in case of claim.”

Why You Shouldn’t Depend on NCB for Long-Term Health Planning

Let’s understand this with a simple real-life situation:

Case Study:

Mr. Rajesh, 40 years old, took a health insurance plan with Rs.5 lakh sum insured and a 20% NCB clause. After 3 claim-free years, his coverage reached Rs.8 lakhs. He felt confident that Rs.8 lakhs was good enough.

In the 4th year, he was hospitalized for an emergency surgery costing Rs.6.5 lakhs. The insurer paid the entire claim from his policy (base + NCB).

But next year, his bonus reset. His policy cover dropped to Rs.5 lakhs again.

Now imagine if he needed a second surgery or a follow-up procedure in the same year or next year? He’d be short of funds.

He now had to either pay from his pocket or rush to buy a top-up cover (which could be costlier due to age and claim history).

Problems That Arise When You Rely Too Much on NCB

1. False Sense of Security

You may feel your policy is sufficient when NCB is at its peak. But NCB is not a guaranteed benefit. One claim can pull it back to zero.

2. Delayed Upgrade Decisions

People avoid increasing their base sum insured because NCB makes it look like their cover is growing. But this is temporary. It delays your decision to buy top-ups or add-on covers, which can prove costly later.

3. Reduced Coverage When You Need It Most

Medical conditions often strike in patterns — first a major event, then follow-ups, complications, rehab, etc. If your NCB gets consumed in the first round, you may not have enough for the next.

4. Avoiding Claims Just to Retain NCB

Some people hesitate to file even small claims, fearing NCB loss. But insurance is meant to reduce your out-of-pocket burden. Delaying treatment or paying unnecessarily just to retain bonus is a poor strategy.

What Should You Do Instead?

Here’s a more balanced approach:

1. Base Your Planning on Base Sum Insured

Always evaluate your health insurance adequacy based on the base sum insured, not with NCB additions. If your base sum insured is ?5 lakhs, plan as if that’s your actual protection — NCB is a bonus, not a shield.

2. Consider Super Top-Up Plans

Buy a super top-up health policy with a high deductible (say Rs.5 lakhs) and an additional cover of Rs.10–25 lakhs. These are affordable and offer better protection than relying on unpredictable NCB.

3. Use Riders Like NCB Protection (If Needed)

Some insurers offer riders that protect your NCB even if you make a claim (up to a limit). Evaluate them carefully — they come at a cost but can help if you want to maintain your coverage buffer.

4. Don’t Hesitate to Use Your Insurance

If there’s a legitimate need to claim, go ahead. NCB is just an add-on — your health and finances are more important than preserving a bonus.

Final Thoughts: NCB is a Reward, Not a Guarantee

No Claim Bonus is an attractive feature, but it should not distort your understanding of your actual insurance coverage. It is temporary, conditional, and revocable.

Make sure you buy health insurance with a sufficient base sum insured, and use NCB only as a bonus. Never build your healthcare plan around a benefit that disappears the moment you actually need your insurance.

Remember, health insurance is not just about saving money when you’re healthy — it’s about protecting your wealth when you’re not.

For Unbiased Advice Subscribe To Our Fixed Fee Only Financial Planning Service

This Fundrise review will examine how the platform works and review its pros and cons.

Fundrise allows non-accredited investors to invest in private real estate funds with initial investments as low as $10. The company has recently expanded to include private equity and private credit investments.

Pros

No accredited investor requirement.

Minimum investments as low as $10.

Multiple fund types are available.

Cons

Investments require careful assessment

How It Works

Fundrise made its reputation by offering real estate funds to smaller investors who aren’t eligible for funds restricted to accredited investors.

The company has introduced new offerings and now offers funds in four strategy categories.

Real estate funds offer multiple packages combining a range of real estate asset classes, serving several investment strategies.

Private credit is an investment strategy pooling funds to lend to companies, capitalizing on the high interest rate environment to deliver strong fixed-income returns.

Venture capital is a new investment strategy for Fundrise, offering investors exposure to a range of pre-IPO companies without the restrictions that often apply to private investors.

Retirement accounts include both conventional and Roth IRAs.

Fundrise is building from its base in real estate to develop a fully integrated platform for investing in alternative assets. The company currently manages over 20 different funds, and investors can choose among them.

Funds are accessible to private investors who previously had little access to these asset classes, with minimum investments as low as $10.

Fundrise currently has over 393,000 active investors. The total portfolio holdings are over $7 billion, and Fundrise has paid out over $344 million in dividends to investors.

Investor communication is a priority, and investors can expect real time performance reporting, frequent analyses of economic trends affecting Fundrise portfolios, updates on portfolio changes, and other materials designed to enhance transparency.

Fundrise offers several investment tiers with different minimum investments and different features.

Plan

Minimum Investment

Features

Starter

$10

Minimal customization, uses fixed portfolios

Basic

$1000

Allows investment via IRAs

Core

$5000

Complete customization and access to a dedicated investor relations team. Accredited investors only.

Advanced

$10,000

Access to customized strategies

Premium

$100,000

Minimal customization uses fixed portfolios

Each of these contains one or more of the Fundrise fund offerings. The difference is in the minimum investment and in the investor’s ability to tailor the portfolio to meet personal preferences and requirements.

Fundrise offers an extremely simple investment process. You open an account, fund it, and select your investment strategy, investment goal, and tier.

From there, Fundrise will manage your portfolio for you, offering suggestions and updates, or you will design your own portfolio if you have selected one of the more customizable tiers.

The Fundrise site gets generally high marks for being informative and easy to navigate.

Let’s take a closer look at what Fundrise offers in its various asset classes.

Real Estate

Fundrise offers several real estate investment plans, differentiated by the mix of income-focused and growth-focused assets in each fund.

Supplemental income funds are designed to produce consistent dividends over the life of the fund but may have lower long-term appreciation.

Balanced investing funds are highly diversified and place an equal weight on income and growth.

Long-term growth funds will generate dividends but place a higher priority on growth-focused assets.

Fundrise calls their real estate funds eReits, and they are structured as Real Estate Investment Trusts (REITs). The main difference between Fundrise eREITS and public REITs is that public REITs are liquid: they trade on public exchanges and can be sold at any time.

The funds managed by Fundrise do not trade on an exchange and are considered illiquid. You can’t just sell any time you want to. There may be a waiting period for redemption – redemptions typically occur at the end of each quarter – and some funds may have early withdrawal penalties.

Fundrise advises that its real estate funds should be considered long-term investments. Investors should not commit funds that they are not willing to tie up for five years or more.

Fundrise offers an exceptional range of real estate assets, including the following:

8,962 multifamily apartments in 10 US markets.

2,310,800 square feet of leased industrial space.

3,471 single-family apartments in 30 US markets.

Fundrise also has 296 active real estate projects and 147 completed projects. These projects are divided into four categories with increasing risk levels.

Fixed income investments generate immediate cash flow with an expected 6% to 8% annual return.

Core Plus investments take 6-12 months to deliver yield, but expect to deliver 8% to 10% annualized yield, with a slightly higher risk profile.

Value Add is a strategy of acquiring undervalued assets and investing additional capital to increase their value. Time to cash flow is 12-18 months, and projected returns are 10% to 12%.

Opportunistic investments carry the highest risk. They may take 2-3 years to first cash flow but are expected to generate 12% to 15% returns on an annualized basis.

All figures for expected return are projections, not commitments.

A Fundrise portfolio can contain a mix of these assets tailored to fit the user’s risk tolerance and investment strategy.

The number of different strategies and asset types can be confusing, but that variety also offers a very high level of diversification for the size of the investments involved and offers the ability to construct many different portfolio types.

🏢 Learn more: Explore the top-performing market opportunities with our guide to the best real estate stocks & ETFs available today.

Private Credit

Fundrise has introduced a private credit fund, which the company describes as “an opportunistic strategy for income-focused investors. The strategy is based on the fact that short term loans currently carry higher interest rates than long-term loans.

The fund is designed to capitalize on the current high interest rate environment by pooling investor funds and lending them to companies. Fundrise is leveraging its real estate experience by lending specifically for real estate projects.

The fund currently has $516 million in capital deployed in 90 debt deals covering real estate projects with 20,194 units at an average interest rate of 10.8%. It delivered a 13% annualized return in its first quarter[1].

This strategy is designed to be temporary and will only be viable while interest rates remain high. Fundrise does not expect this situation to last beyond 2024.

Venture Capital

Investment in privately held technology companies has traditionally been restricted to venture capital firms and well-heeled angel investors. Fundrise aims to upset that status quo with a venture capital fund that is accessible to any investor.

Called the innovation fund, this investment vehicle focuses on high-growth private companies, primarily in the tech sector. The fund primarily invests in four categories.

Modern data infrastructure

Artificial intelligence and machine learning

Development operations

Financial technology

The fund currently has over 35,000 investors, with over $100 million invested in 19 private companies.

As with any venture capital fund, profits are only gained when the companies held go public or are acquired. Investors should be prepared to hold the fund for a medium-term to long-term time frame.

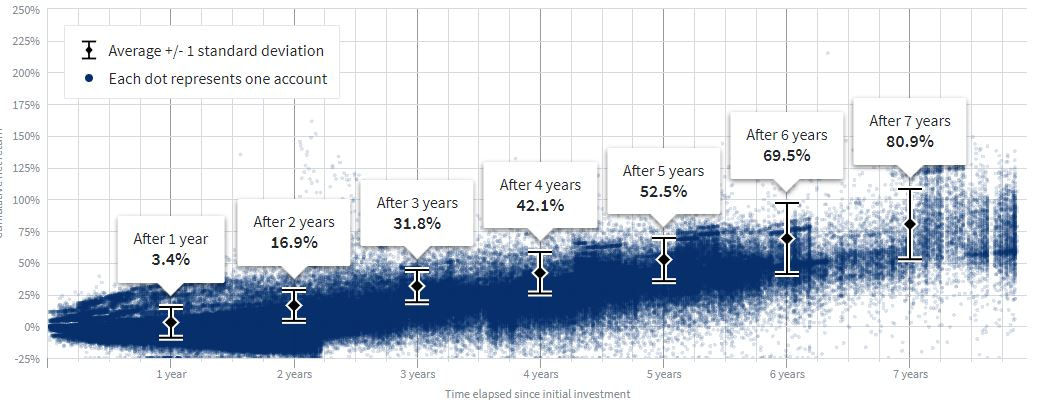

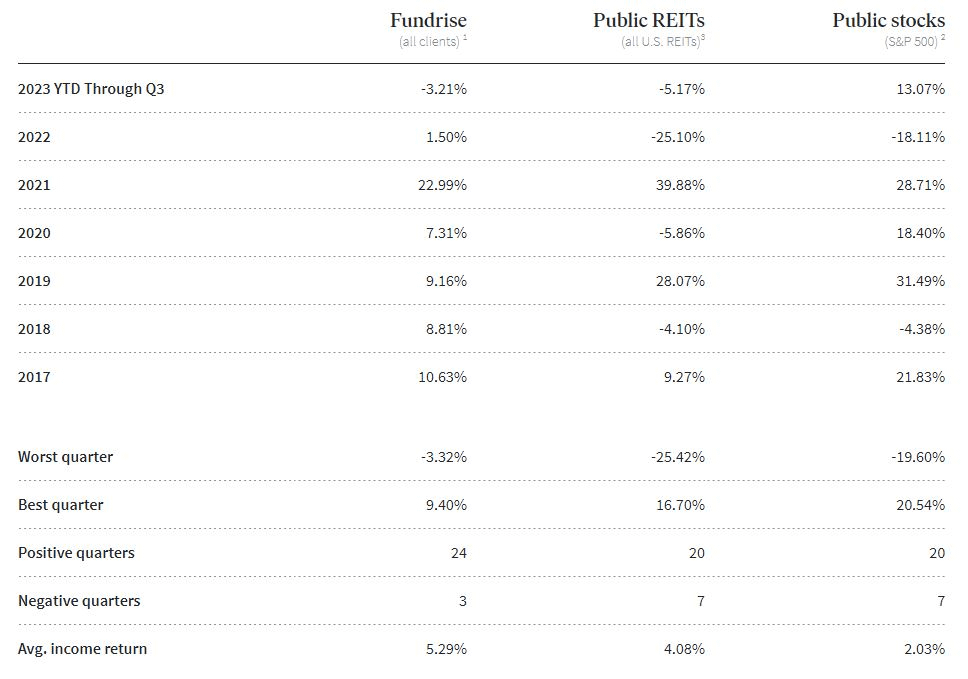

Past Performance

Fundrise provides detailed information on investor returns. As you can see, average returns are solid, but some accounts deliver returns well below the average.

Fundrise also provides data on returns vs public REIT and the S&P 500. Again, these are averages and not all portfolios will deliver the same performance.

It’s clear from these figures that Fundrise can deliver very competitive returns. It’s also clear that these returns are not guaranteed.

You will need to pay close attention to the composition of your Fundrise portfolio, especially if you are using one of the more customizable plans. Evaluating these portfolios will require significant research and expertise.

Costs

Fundrise offers a generally low-cost investing model. There is an annual advisory fee of 0.15% or $1.50 for every $1000 you have invested. This fee does not cover actual fund management expenses.

There is also a management fee of 0.85%, which replaces the per-fund management fees charged by many fund managers.

This amounts to a total of 1%/year in management costs.

You may be required to pay a 1% early redemption fee if you choose to redeem your fund shares after a holding period of less than five years.

The Flagship Fund and the Income Fund do not charge any penalty for quarterly redemptions, but Fundrise can freeze redemptions during periods of economic stress.

There may be additional fees associated with specific projects. These will only be stated in the offering documents for the project, so you’ll need to read these carefully.

Risks

Any investment involves risks, and Fundrise is no exception. Be sure to consider these factors.

Low liquidity. Fundrise offers private funds designed to be held for a minimum of five years. Redemptions are available quarterly, but you may pay a fee if you redeem before five years have passed.

Possible redemption freeze. Fundrise reserves the right to suspend redemptions during periods of economic stress. You may not be able to withdraw your money.

Complex investment vehicles. Fundrise offers a huge range of options, particularly in their higher tiers. Accurately assessing these options may require time and expertise that many investors don’t have.

Fees may be higher than expected. The basic fee structure is reasonable and accessible, but individual projects may carry fees and restrictions of their own, which may not be as easy to find.

No assurance of performance. As with all investments, there is no assurance that a Fundrise portfolio will deliver the expected returns. While average returns are competitive, past results do not assure future performance, and some accounts have delivered below-average returns.

Tax issues. Income from your Fundrise portfolio will be taxed as regular income, not as capital gains or dividend income. You should remember this when comparing potential returns to those of other investments.

Unlike some competing platforms, Fundrise has not invested in projects in which the property developer failed to deliver the expected property and the money effectively disappeared. That doesn’t mean that it can’t happen in the future, but based on its track record to date, Fundrise has generally done a good job vetting and managing its projects.

User Reviews

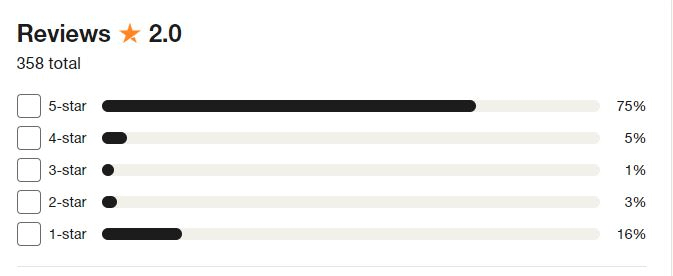

Fundrise has an A+ rating from the Better Business Bureau (BBB), indicating a high degree of responsiveness to complaints. The site has only 8 reviews and 30 complaints, all resolved over the last three years. It’s not possible to draw a relevant conclusion from such a small sample.

Fundrise has 358 reviews on Trustpilot. The average is 2 of 5 stars, which is poor. At the same time, Trustpilot reports that 75% of reviews are five-star and 16% one-star, with the rest scattered between.

Reading the reviews, there’s a clear division between those who were happy with their returns and those who were not. This may stem in part from a failure to fully understand the nature of the investment from the start.

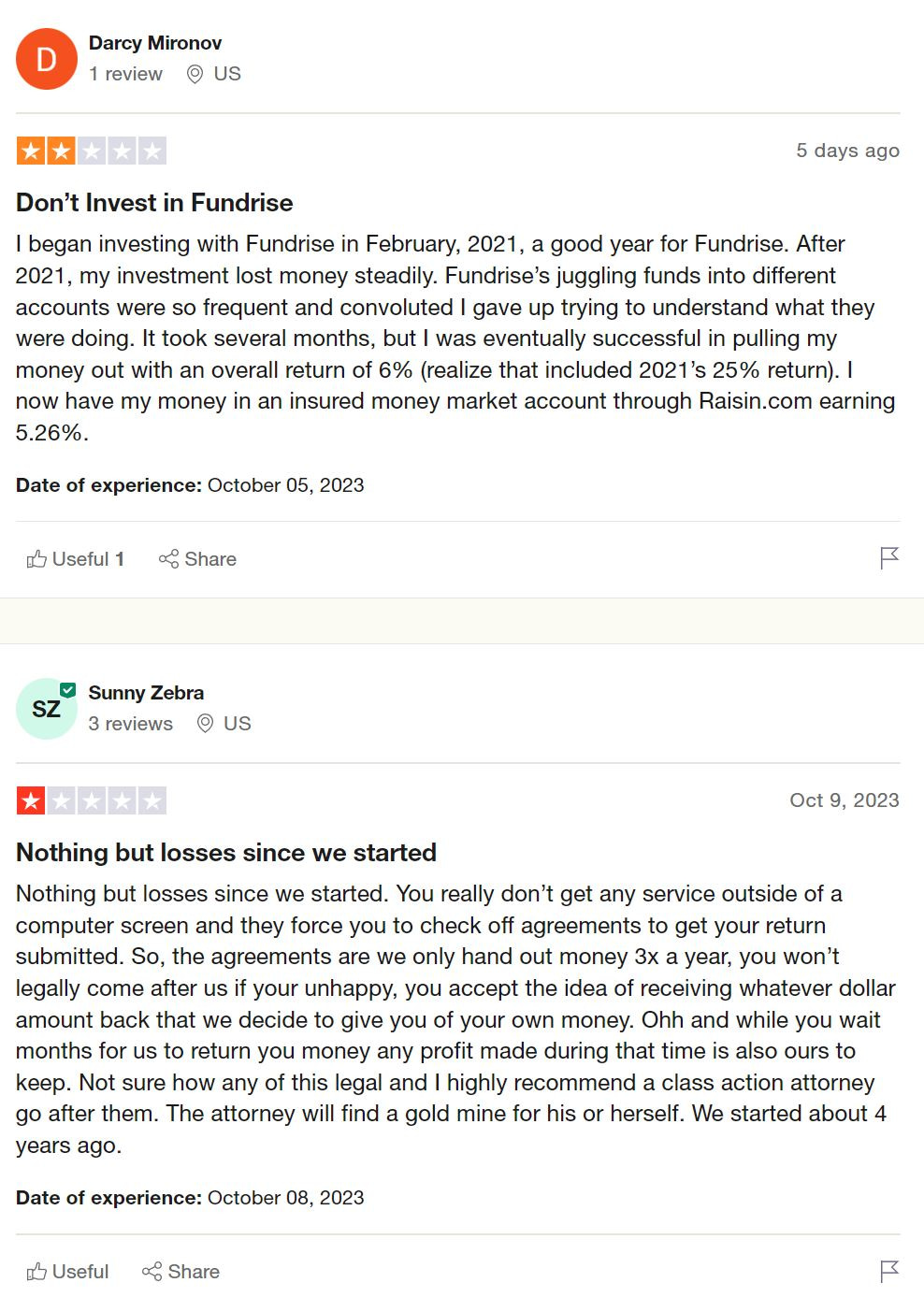

Some investors were clearly unhappy.

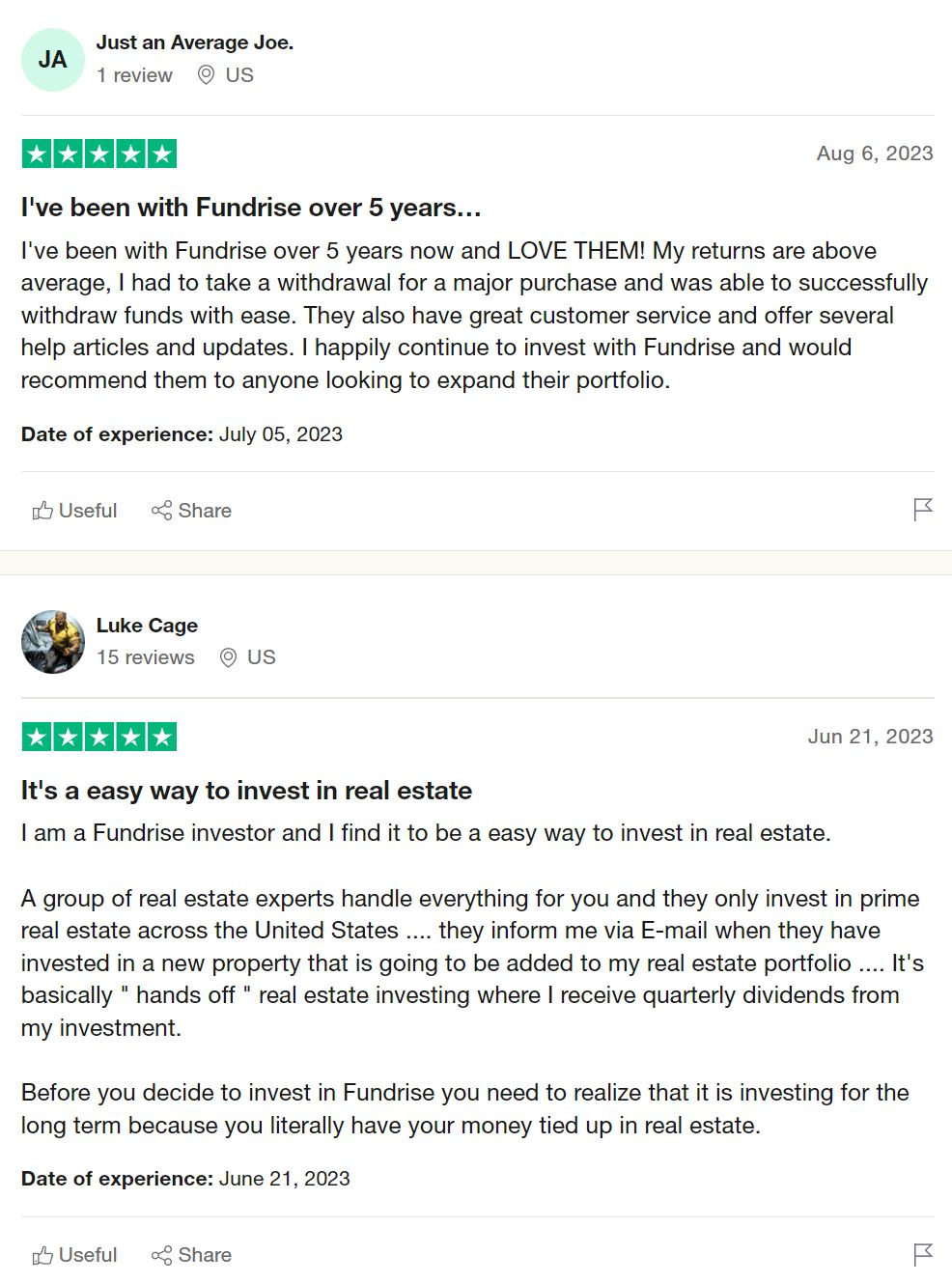

Others had more favorable experiences.

If you do choose to invest in Fundrise, it’s important to recognize that these funds are complex and they are actively managed: fund composition may change rapidly. There is no assurance that a given level of return – or any return – will be achieved.

Is Fundrise Right For You?

Fundrise offers accessible exposure to alternative asset classes such as real estate, private credit, and private equity. You can diversify into these asset classes with investments as low as $10.

That is a substantial advantage over platforms that are only available to accredited investors.

Just because you can, of course, doesn’t mean that you should. A Fundrise investment will tie up your funds for a substantial amount of time, and you may pay a penalty if you need to withdraw early.

If you’re considering a Fundrise investment, be sure that you are assessing not only the potential returns you could get from Fundrise but also the possible returns you could get from other uses of the same funds.

Fundrise has achieved a solid record in its 13 years of operation. Not all portfolios have been profitable and not all years have been positive returns, but the company has avoided scandal and major issues and is a viable option if you want to diversify into alternative asset classes without a major commitment.

If you’re considering a new investment in any asset class, it’s always a good idea to consult a professional investment advisor.

January 29, 2023 Posted By: growth-rapidly Tag:

Personal Finance

Walmart Neighborhood Market is a smaller grocery store format owned by Walmart, offering fresh produce, meat and dairy, bakery, deli, and pharmacy services, among other items. Walmart launched its Neighborhood Market store format in 1998.

Walmart is a multinational retail corporation that operates a chain of discount department stores, grocery stores, and more. It was founded in 1962 and is headquartered in Bentonville, Arkansas, United States. Walmart is one of the largest retailers in the world and offers a wide range of products including groceries, clothing, electronics, home goods, and more at affordable prices.

As of 2023, Walmart has over 11,000 stores worldwide, with over 5,000 in the United States alone. And there are over 550 Walmart Neighborhood Market stores in the United States.

Walmart Neighborhood Market stores typically provide the following services:

Grocery items including fresh produce, meat, dairy, bakery, and deli products.

Pharmacy services with prescription filling and related health services.

Select household essentials such as health and beauty products, cleaning supplies, and pet supplies.

Financial services including money transfers, bill payments, and tax preparation services.

Online grocery delivery and pickup options.

Optical services such as eye exams and eyeglass fittings.

The difference between Walmart Neighborhood Market and Regular Walmart Stores

Walmart Neighborhood Market stores are smaller in size compared to regular Walmart stores and primarily focus on grocery items, pharmacy and select household essentials, while regular Walmart stores offer a wider range of products including electronics, clothing, and home goods in addition to groceries.

In conclusion, the purpose of Walmart Neighborhood Market stores is to provide a convenient, smaller-format grocery shopping option for customers in local neighborhoods. They offer a selection of grocery items, pharmacy services, and select household essentials, aimed at making it easier for customers to get what they need quickly and efficiently. The focus on grocery items and essentials is meant to meet the needs of customers who live in urban or densely populated areas where a full-size Walmart store may not be feasible.

Work With the Right Financial Advisor

You can talk to a financial advisor who can review your finances and help you reach your goals (whether it is making more money, paying off debt, investing, buying a house, planning for retirement, saving, etc). Find one who meets your needs with SmartAsset’s free financial advisor matching service. You answer a few questions and they match you with up to three financial advisors in your area. So, if you want help developing a plan to reach your financial goals, get started now.

Looking to make your money work harder? Explore the world of Certificates of Deposit (CDs), where you can secure solid returns while locking in your funds for a specific time. Discover the banks and credit unions offering the best CD rates, and find out how to maximize your savings with this low-risk investment option.

Certificates of Deposit (CDs) work similarly to online savings accounts or money market accounts in terms of offering great returns with zero risk. The difference is, CDs “lock your money up” for a specified period of time. To access your funds before the term ends, you’ll have to pay a penalty.

Although CDs offer less liquidity than a regular checking account or savings account, you might get a higher rate of return with this financial product. This is especially true if you open a CD account with a longer timeline; for example, a 60-month CD instead of a 12-month CD.

However, quite a few banks offer vastly superior CD rates to consumers who do their research. We compared dozens of banks and financial institutions to find the best CD rates today. If you’re on the hunt for a high-yield CD, start your search here.

Important Factors for Certificate of Deposit Accounts

CDs are for long-term savings. Since CDs lock your funds into the account for a specific term (usually 12 to 60 months), they aren’t ideal for money you might need to access in the short term.

CDs offer security for your funds. CD accounts are a secure place to stash your money and earn interest, thanks to FDIC insurance.

Check for CD fees. Most CDs charge fees if you need to access your money early. Make sure you understand these fees before opening this deposit account.

Online banks might offer better rates. Although brick-and-mortar banks offer their own CDs, you might find better rates through online banks. Compare legacy banks and online institutions to find the best CD rates.

If your goal is securing a superior short-term investment, the best CD rates are worth exploring. To help in your search, we compared many of the top financial institutions and online banks to find options with the most attractive rates and terms.

Find the Highest CD Rates from Banks and Credit Unions

Explore and contrast the top certificates of deposit (CDs) rates based on the highest Annual Percentage Yield (APY), spanning various terms including 3-month, 6-month, 1-year, 2-year, and 5-year options.

For The Current CD Rates…

Raisin (Save Better) partners with some of the top banks in the U.S. for the highest rates on CDs. Check below for the current rates.

Disclaimer: Interest rates are subject to daily fluctuations, and we strive to provide you with the most current information. Please verify the rates with your bank or credit union for accuracy!

The banks below made our ranking due to the interest rates they offer and other features.

PNC

CIT Bank

Discover®

Marcus by Goldman Sachs

Synchrony Bank

Best Certificate of Deposit Accounts – Reviews

There are a few factors to consider when choosing where to open a certificate of deposit. These include whether you want to open your CD in person or online, the rates and terms that apply, and the fees required to access your money early.

The following reviews explain the CD rates for each of the top banks we profile and other details you should know.

PNC Bank

PNC Bank offers a variety of popular banking products, including certificates of deposit. Its CDs don’t require any monthly maintenance fees, and you can monitor your account at any time online or with the BBVA mobile banking app.

CD terms range from 7 days to up to 10 years, and CDs with longer timelines pay higher CD rates. Note that penalties apply if you access your money early.

If you cash out your CD early, with a term of one year or less, you’ll pay $25 plus 1% of the amount withdrawn. If you cash out a CD with a longer-term early, you’ll pay $25 plus 3% of the amount you cash out.

CD Rates: Online CDs with terms from 11 months to 36 months currently pay up to 5.04% APY.

CIT Bank

CIT Bank is known for its popular high-yield savings account, known as Savings Builder, but it also offers an array of CDs with excellent terms. Its 11-month, no-penalty CD stands out since it offers an excellent return rate. There are also no penalties if you need to access your money early.

CIT Bank also offers term CDs with various other lengths, as well as jumbo CDs for deposits of $100,000 or more. None of its CDs come with account opening fees or account maintenance fees.

CD Rates: CIT Bank currently pays from 0.30% to 3.50% APY on their CDs, depending on the term you choose. Top rates are offered on their 18 month CDs, which pay out 3.00% APY, respectively. Additionally, they have an excellent 11-month No-Penalty CD at 3.50% APY as of the time of this writing (04/05/23.)

Discover

With Discover, you can open a CD that lasts anywhere from three months to 120 months. There are no fees to open a CD, including account opening fees or maintenance fees.

Discover also stands out due to the reasonable penalties it charges if you need to access your money early. CDs with a term of less than one year, incur a penalty at three months of simple interest. For a CD that lasts one to four years, the penalty for cashing out early is just six months of simple interest.

CD Rates: The 18-month CD is most rewarding, currently offering 4.00% APY. If you’re willing to part ways with your funds for just 24 months, you can earn a rate of 4.10% APY.

Marcus by Goldman Sachs

Marcus by Goldman Sachs is a popular online bank for personal loans and high-yield savings accounts, yet it also offers rewarding CDs. Terms for its CDs range from seven months to six years, with a minimum $500 deposit to get started.

Marcus by Goldman Sachs even offers a 10-day guarantee that says you can move your rate up if the advertised rates on the CD you purchased increase within 10 days.

CD Rates: Some of the best CD rates from Marcus by Goldman Sachs are for its 9-month CDs, which currently pay 4.30% APY. Marcus by Goldman Sachs also offers limited-time CD rate promotions, like 4.40% on an 18-month CD.

What Holds It Back: Marcus by Goldman Sachs is an online bank only, so you don’t have the option to open your CD in person.

Synchrony Bank

We chose Synchrony Bank for our ranking because it doesn’t impose a minimum balance requirement, yet has competitive CD rates. It offers a 15-day guarantee, which lets you raise your rate if the advertised rate increases within 15 days of your CD purchase.

Terms are available from three months to 60 months. Early withdrawal fees for their CDs are also reasonable. For example, early cash-outs on CDs with terms of 12 months or less charge 90 days of simple interest at the current rate.

CD Rates: Five-year (60-month) CDs currently pay 4.00% APY, and three-year (36-month) CDs pay 4.30% APY. They also have a 16 month paying 5.40%

What Holds It Back: Synchrony Bank CDs are meant to be opened and maintained online, so you consider a different bank if you’re hoping for a personalized experience or you prefer to bank in person.

How We Found the Best CD Rates

Finding the best CD rates is important if you want to maximize returns on your savings, yet there are other factors to consider before opening an account. We considered the following factors when compiling this list of banks with the best CD rates of 2025:

Rates and Terms

Although we gave preference to banks that apply the best rates to various CD terms, we focused on banks that offer at least one CD with an APY that is at least double the average CD rate nationwide.

BBVA didn’t score well in this category, yet we included them due to their lack of account fees and a strong reputation among major U.S. financial institutions.

Account Fees

We only considered banks that don’t charge fees to open a CD account. We also chose banks that don’t charge any monthly account maintenance fees.

Early Withdrawal Penalties

Most banks charge an early withdrawal fee if you cash out your CD early, so we looked for banks with reasonable penalties. We also gave preference to accounts or CD options that don’t charge any penalty for early withdrawals.

FDIC Insurance

Finally, we only included institutions in our ranking that offer FDIC insurance. This insurance secures up to $250,000 of CD funds per account holder.

What You Need to Know About Certificates of Deposit

If you have never opened a certificate of deposit before, you might wonder how they work and why people choose this option. Here are some important factors when considering a CD account.

CDs offer superior rates compared to other deposit products. According to recent figures from the FDIC, the average national CD rate for a 60-month term is about four times greater than the average national savings account rate.

Longer CDs offer better yields. Committing your money to a longer timeline can lead to considerably higher returns. FDIC data shows that the average APR for a one-month CD is only .02% — not much better than a basic savings account.

CD rates can go up or down over time. CD rates are determined based on the current interest rate environment, including benchmark interest rates. This means that you might get a better CD rate any time benchmark interest rates go up.

CD rates can be higher on larger amounts. If you have $100,000 or more to deposit, you might qualify for a “jumbo CD”. This type of CD requires a high minimum deposit, but banks are willing to pay higher APYs to lock in more funds.

Investing in a certificate of deposit (CD) is one of the safest ways to grow your money. CDs are low-risk investments with guaranteed returns, so they can be an excellent choice for those looking to diversify their portfolios and lock in higher interest rates.

When choosing a CD, it’s important to compare APYs (annual percentage yields) and terms between different banks and credit unions in order to get the best rate possible. Shop around for promotional offers or talk to financial advisors if you need help selecting the right CD for your needs.

With careful research and comparison, you’ll be able to find the CD that gives you the highest rate – and peace of mind – in the long run.

Some of the key factors you should consider when searching for the best CD rates include the length of the term, any penalties for early withdrawal, and minimum deposit requirements. You’ll also want to compare the annual percentage yields (APYs) of different products to ensure you’re getting a good return on your investment.

Certificate of deposit (CD) rates may fluctuate throughout the year as interest rates change. It’s important to keep an eye on current market conditions in order to maximize your earning potential by investing in CDs with higher rates.

Yes, it is possible to get a higher APY than what is advertised by banks and credit unions – especially if you are willing to negotiate or shop around at online banks that offer competitive CD rates. Additionally, certain banks may offer promotional offers or discounts that can result in even better returns on your investment.

When comparing CD rates, consider the length of the term, penalties for early withdrawal, minimum deposit requirements, and the annual percentage yield (APY). The APY reflects the effective interest rate, including compounding.

While advertised rates are set, some banks, especially online ones, may offer negotiation options or promotional offers. Shopping around and researching online banks could help you find institutions that offer competitive rates or special deals.

I haven’t paid an ATM fee in ages because I use an Ally Bank checking account. They will reimburse me $10 per statement cycle on fees charged by another bank when I use their ATM. They also have a partnership with Allpoint and MoneyPass so I can access my cash through those networks without paying a fee.

$10 isn’t a lot but I don’t need cash often so it’s actually a perk I rarely use.

If you’re paying ATM fees for using other banks, you should consider switching to a bank that will reimburse you for those fees. Sadly, many of the best online banks do not offer ATM reimbursement as a perk (I checked Sofi, Capital One, Discover, CIT Bank, and a few more).

Here are some major banks that offer this and their terms, listed in alphabetical order:

Alliant Credit Union is a nationwide credit union that has 80,000+ fee-free ATMs but they will reimburse you up to $20 in ATM fees per month. The rebates are deposited into your account at the end of the day they are charged, which is a nice touch.

Ally Bank partners with the Allpoint and Moneypass networks so you get access to thousands of fee free ATMs but they will reimburse you up to $10 each statement cycle for fees charged by other ATMs. Ally will not charge you an additional fee though.

The checking account interest rate is tiny, which is common, but their savings account currently yields 3.70% APY. It’s not the top rate possible but it’s competitive.

Axos Bank, through its various checking products, offers unlimited ATM fee reimbursements, which is quite rare. most banks offer limited reimbursement but Axos goes beyond that. For example, on their Essential Checking account, you get early direct deposit, no overdraft, NSF, or monthly maintenance fees on top of unlimited ATM fee reimbursements.

The savings account available through Axos currently yields 4.66% APY.

Betterment, best known as a roboadvisor, offers unlimited ATM fee reimbursement on their checking accounts and that reimbursement will come as a credit the following calendar day. This extends internationally too, they will reimburse any ATM worldwide and will also reimburse you the Visa 1% transaction fee on foreign transactions, purchases, and ATM transactions.

Charles Schwab Investor Checking is Charles Schwab’s checking account and it offers unlimited ATM fee rebates on their Schwab Bank Visa Platinum Debit Card. Again, unlimited ATM reimbursement is rare and this is appealing if you already have a Charles Schwab account. Reimbursement happens at the end of the month.

Consumers Credit Union

Consumers Credit Union is the second credit union that made this list and they offer unlimited reimbursement of any and all ATM fees on their Rewards Checking account. They also have partnerships that allow you to use 30,000 surcharge-free ATMs but they’ll reimburse you for any fees you do get charged if you can’t find one of those ATMs.

Fidelity Cash Management Account

Fidelity will reimburse all ATM fees when you use their card linked to a Fidelity Cash Management Account. If you have a card linked to a Fidelity Account® Premium, Active Trader VIP, Private Client Group, Wealth Management, current or former Youth accounts owners, all ATM fees are reimbursed as well.

TD Bank

TD Bank offers reimbursement on their checking accounts, such as the TD Beyond Checking account. With that account, you get non-TD Bank fees reimbursed at all ATMs when you have at least a $2,500 daily balance.

TIAA

TIAA will reimburse you up to $15 for ATM fees charged by other banks but if you have an average daily balance above $5,000, they will reimburse you an unlimited number of times and amount. You can read the terms here.

USAA

USAA has partnered with networks that get you 100,000+ ATMs with no fees but if you can’t find one, they will reimburse you up to $10 each monthly statement cycle in ATM fees.

Wells Fargo

Wells Fargo offers ATM fee reimbursement on their Premier Checking and Prime Checking accounts. With Premier Checking, they will reimburse all fees but that account requires you to have a $250,000 minimum balance each month to avoid the $35 a month fee! The Prime Checking account, which requires a $20,000 minimum balance to avoid a $25 monthly fee, will reimburse you the first U.S. and first international fee each period.

When you transfer investments in a brokerage account from one broker to another, it goes by a system called ACATS, which stands for Automated Customer Account Transfer Service. Some people call it ACAT. I’m going with the official name ACATS.

ACATS transfers keep the holdings intact and don’t trigger taxes. I used ACATS when I transferred a part of my account from Fidelity to US Bancorp Investments recently for the 4% rewards card.

With all the hacks and data leaks in recent years, fraudulent ACATS transfers have also become a problem. I read a report of this type of fraud from a poster ww340 on the Bogleheads forum.

I discovered that our taxable account at Vanguard had been slowly pilfered of approximately $100,000 in stocks transferred by ACATS to 2 different brokerage accounts that were not mine over a period of time.

These stock transfers were taken out of our account each time we received a dividend. … … Every few months 750 shares of that fund were transferred. Transfers were made 3 times before I realized it was happening.

We don’t want our investments stolen from us. How do we protect our accounts from ACATS fraud?

Fraudulent Account In Your Name

ACATS is a pull-only system. All transfer requests start at the receiving firm. A transfer requires a medallion signature guarantee if names don’t match between the receiving and the sending accounts. Therefore thieves usually start with creating a fraudulent account in your name at another broker. They don’t have to hack into your account when they could just pull from an account they control.

Opening a brokerage account doesn’t require a credit check. Freezing your credit doesn’t stop it. Freezing your ChexSystems report doesn’t stop it either because that’s only for banks and credit unions. If someone has your name, Social Security Number, address, and phone number, they have all the information to open a brokerage account in your name. All those pieces of information have been leaked in repeated hacks.

Because thieves can choose paperless delivery at many financial institutions, you may have no clue when a fraudulent account is opened in your name somewhere out there. Some brokers still send mail. You should be on alert if you receive mail from a financial institution you don’t use.

Account Number and Statement

An ACATS transfer request requires the account number of the source account. Some brokers ask for a recent account statement from the source account but it’s often optional. My recent transfer went through without a statement.

An ACATS transfer doesn’t require confirmation by the customer at the sending firm either. A transfer would go through if someone had your account number and the names matched on both accounts. Therefore you should safeguard your account number from falling into the wrong hands. That’s the critical piece of information for a successful ACATS transfer.

A partial transfer also requires knowing your holdings, which are listed in your online account or statements. Therefore you should protect your account statements.

Choose paperless statements and tax forms. They are more secure than hard copies sent by mail. Store those documents securely.

Your brokerage account should have the strongest 2-factor authentication. Don’t let thieves reset your password to get your account number or holdings. See Security Hardware for Vanguard, Fidelity, and Schwab Accounts. If you submit your statement to someone to qualify for a loan, black out the account number.

Your email should also have the strongest 2-factor authentication. Don’t let thieves find your account number or holdings in some emails. See Secure Your Email Account to Prevent Wire Fraud.

Enable Lockdown

Fidelity is the only broker I know that offers an optional Money Transfer Lockdown feature. It doesn’t stop all the ways money can go out of an account but a partial lockdown is better than no lockdown. Fidelity will reject all ACATS transfers when you turn on this setting on an account.

Enabling the lockdown also stops some legit transfers you initiate. You’ll have to disable the lockdown, do your transfer, and re-enable the lockdown. It’s a tradeoff between convenience and protection.

Transfer Alerts

An ACATS transfer doesn’t require an approval from you before it goes through but it’s helpful if your broker at least sends you an alert when it receives a transfer request or immediately after it processes a transfer. Some brokers don’t do any of that.

Fidelity sent me an alert when they received my legit transfer request through US Bancorp Investments. When I transferred from Vanguard last year, Vanguard didn’t send me anything either before or after they processed the transfer. A fraudulent transfer could’ve gone through without my knowledge. Vanguard only sent me a letter after a few weeks saying the account was closed. I would’ve received nothing if it had been a partial transfer and the account was still open, as was the fraudulent transfer against ww340.

If your broker notifies you by mail, it’s helpful if you open it. The poster ww340 said,

I had everything online and usually only get proxy votes or fund information sheets, so I do not always open Vanguard mail.

That was a mistake. Use a broker that sends you alerts about these transfers either before or after the transfer is processed. The sooner you know, the better chances you have to stop the transfer or reverse it. Make a habit of reading everything that comes from your broker.

A Flood of Spam

Beware when you receive a sudden flood of spam emails and texts. It’s a telltale sign you’re under attack somewhere. Thieves flood you with spam to bury the notification emails and texts from your financial institution. This happened to ww340:

My email got hundreds or thousands of spam emails every time a fraudelent order was placed. My email had 73,000 emails with 99% of those were spam and spam subscriptions. So that hid the fraud when the notices were hidden among the spam.

Call your banks and brokers immediately and tell them to stop all transactions if you see a surge of spam emails or texts.

Check Your Accounts

Some people suggest not checking your investment accounts often. This helps you avoid trading on fear or greed. That’s good if your broker will notify you of outgoing activities and you’re on top of the notifications. Otherwise your account or shares could be long gone before you notice.

Brokers send you account statements monthly or quarterly for a reason. You don’t need to check your accounts daily. I suggest checking monthly for unusual activities.

Keep Independent Records

An ACATS transfer can be a full transfer of the entire account or a partial transfer of select holdings. A full account transfer is easier to detect when you see your entire account is gone. A partial transfer such as leeching 750 shares at a time is more difficult to see.

Portfolio values fluctuate with the market prices but you should match the number of shares in your account with your independent records. Don’t just look at the total value of your account. Look at the number of shares in each holding. Thieves that stole from ww340 tried to hide their theft by transferring out shares shortly after a dividend was paid. You may not detect it easily if you only look at the total value.

Many old-timers use Quicken to track their accounts. I use Microsoft Money, which was discontinued 10+ years ago but you can still find the last free release on archive.org. It still works on Windows 11. What system you use doesn’t matter as long as it helps you track your shares independently. An online aggregator such as Empower or Fidelity’s Full View isn’t the best tool for this purpose because they don’t maintain an independent source of truth. An online aggregator only reports what’s currently in your accounts.

You should know how many shares you should have in each holding at any time. Compare them with how many shares you see in your account. You’ll know when you see a difference. Having fewer accounts, fewer holdings, and fewer transactions will make this task easier.

***

ACATS was designed before all the hacks and data leaks. Now the account number is the only secret that prevents a fraudulent transfer. We must do everything we can to protect this secret. It helps to turn on the lockdown setting if your broker offers it. It also helps to use a broker that notifies you of pending and completed transfers.

Fraudulent ACATS transfers can be reversed. We want to detect them sooner rather than later. Check your account activities monthly and keep independent records.

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

Picture a life without alarm clocks, office meetings, or weekday traffic — where you travel, pursue passions, or simply enjoy peace. That’s the dream early retirement planning aims to turn into reality.

More and more people in India are rethinking the traditional retirement age and exploring how to retire by 40 or 50. While it sounds ambitious, it’s possible with the right approach to retirement planning. It’s not just about saving aggressively — it’s about investing wisely, minimizing debt, and planning strategically for long-term financial freedom.

Successful early retirement planning requires discipline, clarity, and expert guidance. That’s where professional retirement planning services come in — helping you map a plan that aligns with your goals.

In this blog, we’ll explore how to retire early in India, key financial steps, and how expert advice can make it happen.

What Is Early Retirement Planning?

Early retirement planning is the process of preparing financially and mentally to retire before the conventional retirement age. This doesn’t just mean saving more — it means saving smarter, investing wisely, and making decisions that align with long-term goals.

Unlike traditional retirement planning, early retirement compresses the timeline, often requiring you to accumulate a corpus in 20-30 years rather than 40-45. It also requires that corpus to last longer, potentially 30-40 years or more.

Why Do People Choose Early Retirement?

People pursue early retirement for various reasons, such as:

Pursuing passions or hobbies that require time and energy

Escaping corporate burnout or a high-stress lifestyle

Spending more time with family

Starting a second career or a business venture

Improving quality of life while still in good health

Whatever the motivation, the path to early retirement starts with meticulous early retirement planning.

Step-by-Step Guide to Early Retirement Planning

1. Define Your Retirement Goals

The first step in early retirement planning is defining what retirement looks like for you. Consider:

At what age do you want to retire?

Where do you want to live post-retirement?

What kind of lifestyle do you want to maintain?

Do you plan to travel, start a business, or pursue a hobby?

Knowing these answers helps you estimate the cost of your dream retirement and set a realistic savings target.

2. Calculate Your Retirement Corpus

A general rule of thumb is that your retirement corpus should be 25-30 times your annual expenses. If you expect to spend ₹10 lakhs annually, you should aim for a corpus of ₹2.5–3 crores (or more considering inflation).

Use tools like a retirement planner or a retirement calculator to factor in:

Life expectancy

Inflation

Healthcare costs

Lifestyle expenses

Emergency fund

3. Start Saving Early and Aggressively

Create multiple savings goals such as:

The earlier you start saving, the more you benefit from compounding. For early retirement, aim to save 40% to 70% of your income, especially in your 20s and 30s. The FIRE (Financial Independence, Retire Early) movement recommends living frugally to save a larger portion of income.

Emergency fund (6–12 months of expenses)

Retirement fund

Health fund

Travel or leisure fund

Consistent, high-percentage saving is the foundation of effective early retirement planning.

4. Invest Smartly

Savings alone won’t take you far unless they’re invested wisely. Choose investments that offer long-term growth and align with your risk appetite.

Ideal Investment Options for Early Retirement:

Equity Mutual Funds: High returns over the long term

ULIPs: Insurance with investment benefits

Public Provident Fund (PPF): Safe and tax-saving

National Pension System (NPS): Long-term retirement savings with equity exposure

Stocks: For aggressive investors

REITs and rental income: Real estate income

Gold ETFs: As an inflation hedge

You need to choose and balance these instruments based on your retirement timeline.

5. Create Passive Income Streams

To retire early, it’s wise to create sources of passive income. These generate revenue even after you stop working full-time.

Some passive income ideas:

Rental income from property

Dividends from stocks

Royalties (books, music, etc.)

Income from side businesses

The goal is to have income that covers your essential expenses without dipping into your retirement corpus prematurely.

6. Plan for Healthcare Costs

Healthcare expenses can derail the best retirement plans. With aging comes a higher probability of lifestyle and chronic diseases. Once you retire, employer-sponsored health insurance typically ends.

To protect your finances:

Purchase a comprehensive health insurance plan

Invest in critical illness cover

Build a healthcare emergency fund

Fincart’s retirement plan services help integrate medical cost planning into your overall retirement strategy.

7. Be Debt-Free Before You Retire

Paying EMIs during retirement can drain your savings. Make it a goal to be debt-free before retiring.

Tips:

Avoid long-term loans after 40

Prioritize clearing home loans, credit card debts, and personal loans

Don’t co-sign loans that might risk your financial independence

A debt-free retirement ensures you enjoy peace of mind and financial freedom.

8. Monitor and Rebalance Your Portfolio

Early retirement planning doesn’t stop at investing — it continues with regular monitoring.

At least once a year:

Review your financial goals

Rebalance your portfolio

Adjust for inflation and market volatility

Assess if you’re on track for your target retirement age

A retirement planner can periodically evaluate your plan and suggest course corrections.

9. Practice Frugality

Retiring early means your savings have to last longer. Adopting a frugal lifestyle — without compromising on essential needs — is critical.

Differentiate between needs and wants

Reduce discretionary spending

Avoid lifestyle inflation

Focus on value-driven purchases

Living well below your means during your working years paves the way for financial freedom.

10. Use the 4% Withdrawal Rule

Once you retire, managing your corpus becomes crucial. The 4% rule suggests that you can withdraw 4% of your total corpus annually in the first year, adjusting for inflation every year after.

For example, if your retirement corpus is ₹3 crores, you can safely withdraw ₹12 lakhs in the first year.

Note: This rule is a general guideline and should be personalized with help from a retirement planner.

Advantages of Early Retirement

More Time for Hobbies and Travel: Enjoy activities while you are still young and energetic.

Reduced Stress: No work pressure or deadlines.

Opportunity to Start Something New: Launch a business, mentor others, or volunteer.

Improved Health: Less work stress can positively impact physical and mental health.

Challenges of Early Retirement

Savings Need to Last Longer: You might need 30–40 years of sustained income.

Healthcare Expenses: You bear the full cost without employer benefits.

Potential Boredom: Lack of purpose can affect mental health.

Social Isolation: Colleagues and peers may still be working.

These challenges can be addressed through thoughtful early retirement planning and lifestyle design.

Role of a Retirement Planner

A retirement planner plays a pivotal role in shaping your early retirement journey. At Fincart, our planners offer:

Personalized financial assessments

Investment strategies tailored to your goals

Risk profiling and asset allocation

Tax-efficient planning

Periodic reviews and rebalancing

Using Fincart’s retirement plan services, you can retire early with confidence and financial security.

Making Early Retirement a Reality: Key Takeaways and Action Plan

Early retirement may seem like a luxury, but with smart financial decisions and consistent planning, it can become an achievable goal. The secret lies not in how much you earn, but how wisely you save, invest, and plan. Here’s a consolidated view of what you need to focus on to make early retirement a reality — not just a dream.

1. Start Early, Stay Disciplined

The earlier you begin your early retirement planning, the more time your money has to grow. Even small monthly investments can compound into a significant corpus over time. Delaying just a few years can drastically impact your retirement corpus.

2. Key Elements of an Effective Early Retirement Plan:

Aggressive savings strategy: Aim to save at least 40–60% of your income if you’re targeting retirement before 50.

Health insurance coverage: Post-retirement medical costs can drain your savings. Invest in a comprehensive health plan early.

Debt-free living: Clear off major debts — home loans, personal loans, credit card balances — before retirement.

3. Build Multiple Income Streams

Relying solely on your retirement corpus can be risky. To ensure sustained cash flow, create parallel income sources such as:

Rental income

Dividend-paying stocks or mutual funds

Freelance consulting or part-time business ventures

4. Monitor, Review, and Adjust

Your retirement plan isn’t a one-time effort. Revisit it annually to:

Adjust your investment contributions

Rebalance asset allocations based on market trends

Recalculate expenses as per lifestyle or health needs

Keep pace with inflation and changing goals

5. Leverage Expert Retirement Planning Services

Planning for early retirement involves more than just saving money — you must also account for inflation, tax implications, insurance needs, and changing market conditions. This can get complex quickly. Working with a professional retirement planner gives you access to tailored strategies, informed decision-making, and regular plan reviews to ensure your goals stay within reach. Expert retirement planning services help you stay disciplined, optimize investments, and make smarter financial choices as your needs evolve.

Benefits of Expert Retirement Planning with Fincart:

Tailored retirement corpus calculation

Tax-efficient investment strategies

Periodic reviews and realignment

Health and life insurance advisory

Legacy and estate planning guidance

Final Thoughts

Early retirement planning is a commitment to securing your financial independence years before the conventional age. It demands clarity of purpose, aggressive savings, diversified investments, and consistent discipline. While the journey may seem tough, the rewards are life-changing.

Whether your dream is to travel the world, start a business, or just live peacefully, early retirement can offer that freedom — but only if backed by solid financial planning. Let Fincart be your partner in this journey. Our experienced retirement planners and holistic retirement plan services are designed to help you live your dream life — sooner than you thought possible.

Do term life insurance war exclusions cover civilian death? Find out the answer and how to protect yourself during such uncertain times.

When a country faces geopolitical tensions or an ongoing conflict, it’s natural for people to worry about the impact on their lives, including their financial security. For those with term life insurance, a common concern is whether a death due to war or war-like situations will be covered under their policy. This is particularly important for civilians, as they are often indirectly impacted by the chaos of war, even though they aren’t directly involved in military actions.

In this blog post, let us explore the key aspects of war exclusions in term life insurance policies and clarify whether civilian deaths due to war are covered. Let’s break down this complex topic by looking at common policy exclusions across Indian insurers and understanding the risks involved.

Are Term Life Insurance War Exclusions Valid for Civilian Death?

Term life insurance policies typically offer a straightforward benefit: in the event of the insured person’s death, the nominee will receive a sum assured. However, like most insurance contracts, term policies come with exclusions — situations in which the insurer will not pay out a claim.

One of the most common exclusions in life insurance policies is death due to war or war-like situations. But how do these exclusions work for civilians, and what exactly do insurance companies mean by “war” in these contexts?

Most life insurance policies, including those from well-known Indian insurers like LIC, HDFC Life, ICICI Prudential, SBI Life, and others, explicitly exclude death resulting from war or war-like situations.

As per the standard exclusion clause in LIC’s Tech Term policy document,

“The Corporation shall not be liable to pay any death claim if the death of the Life Assured is caused directly or indirectly by or resulting from war, invasion, act of foreign enemy, hostilities (whether war is declared or not), civil war, rebellion, revolution, insurrection, or military or usurped power.”

This exclusion can be interpreted to mean that any death caused by a situation involving armed conflict, war, terrorism, civil commotion, or similar circumstances will not be covered under the policy, whether the individual is a civilian or a member of the armed forces.

Please take note of these two important points here.

The term “war” usually refers to an organized conflict between states or parties, but the exclusion also includes civil war, terrorism, and rebellion.

The clause is broad and comprehensive, applying to both civilian deaths as well as those related to military operations.

Why Are War-Related Deaths Excluded from Term Insurance?

The reasoning behind this exclusion is primarily based on the risk factors associated with war or conflict situations. Insurance is typically designed to protect individuals from unpredictable but insurable risks. Events like war, terrorism, and civil strife are catastrophic, wide-ranging events that are often seen as uninsurable.

Here are a few reasons why insurers usually exclude war-related deaths:

High Risk of Mass Casualties: Wars and conflicts can cause widespread destruction, leading to significant casualties that insurance companies may find financially unsustainable to cover.

Unpredictability: The nature of war is often unpredictable, and its effects can extend beyond traditional accidents, including factors like national security, military actions, and civil unrest.

Excessive Losses: Insuring against war can expose insurers to enormous liabilities due to the large-scale death tolls and destruction.

Do War-Related Exclusions Apply to Civilians?

Yes, civilian deaths due to war are generally excluded under the terms of most Indian term life insurance policies. While the first part of the exclusion often focuses on military personnel (especially those directly engaged in military operations), the second part applies to all insured persons — including civilians.

Example of Common Exclusions for Civilians:

Death due to bombing, airstrikes, or missile attacks during a conflict.

Death caused by terrorist activities, which are often part of war-like scenarios.

Injury or death during civil unrest, rebellion, or revolution.

Even though civilians are not actively involved in combat, they can still be directly impacted by the consequences of war. Therefore, under most policies, these deaths are excluded from coverage.

Are There Any Exceptions to the War Exclusion?

In some special cases, insurers may make exceptions to the war exclusion, especially if the death is incidental to war rather than a direct result of it. For example:

If a civilian dies in a non-combat situation (such as a traffic accident caused by a bomb blast during a conflict), some insurers may consider paying the claim.

Accidental deaths resulting from war-like conditions might still be covered under accidental death benefit riders if the rider is separately purchased and doesn’t include exclusions for war.

However, these exceptions are rare, and the general rule remains that death due to war-related incidents is not covered.

Here’s a quick look at how some major Indian insurers treat war-related exclusions in their term life insurance policies:

Insurer

War Exclusion Clause

Death Due to War (Civilians)

LIC

War, invasion, terrorism, civil commotion, rebellion, etc.

Not covered

HDFC Life

War, terrorism, civil commotion, rebellion, military actions, etc.

Not covered

ICICI Prudential

War, civil commotion, terrorism, hostilities, military or usurped power

Not covered

SBI Life

War, rebellion, terrorism, civil war, hostilities

Not covered

Max Life Insurance

War, invasion, terrorism, hostilities

Not covered

As you can see, almost all major insurers have the same exclusion when it comes to death due to war.

Conclusion – To summarize, death due to war is generally excluded under term life insurance policies in India — even for civilians. While war may be an unpredictable and uncontrollable event, insurers typically deem it an uninsurable risk. Therefore, civilian deaths resulting from war, whether caused by airstrikes, bombings, or terrorist activities, are usually not covered.

If you are concerned about the risks associated with such events, it’s advisable to:

Review your policy exclusions carefully.

Consider additional coverage like accidental death benefit riders, which might offer some level of protection in cases of terrorism or accidents during conflict situations.

Disclaimer: The above article is based on the general information available in policy documents of various insurers. However, in a real-life situation such as war, the government may intervene and direct insurers to honor claims, or insurance companies might choose to settle them on humanitarian grounds. Still, I strongly recommend reviewing your individual policy document for specific exclusions and clarity.

For Unbiased Advice Subscribe To Our Fixed Fee Only Financial Planning Service

Every parent wants to see their kids succeed in life, and for many, that means offering financial support along the way. From college tuition to wedding expenses to helping with a down payment on a first home, it’s easy to open your wallet in the name of love. But while generosity is a beautiful quality, it can also come with a hidden cost: your own financial security.

Many retirees find themselves struggling to make ends meet because they gave too much to their children during their working years. Here are seven shocking ways helping your kids can leave you broke in retirement — and how to avoid falling into the same trap.

1. Paying for College Without a Plan

Covering college tuition and expenses is one of the biggest ways parents support their kids, but it’s also one of the easiest ways to derail retirement savings. With the cost of higher education soaring, parents often find themselves dipping into 401(k)s, IRAs, or even home equity to pay for tuition. Unfortunately, these withdrawals can create significant tax burdens, penalty fees, and a loss of future growth on investments meant to support your retirement.

Worse still, once that money is gone, it’s gone, unlike student loans that can be refinanced or deferred. Helping your child is admirable, but doing so without a clear plan can jeopardize your own financial well-being.

2. Co-Signing Loans That Come Back to Haunt You

Co-signing a student loan, car loan, or mortgage for your child might seem like a quick way to help them build credit or afford that first home. But if your child struggles to make payments, the responsibility falls squarely on you. Missed payments can tank your credit score and leave you on the hook for the entire debt, often at the worst possible time…like right before retirement.

Some parents end up paying off loans they never expected to cover, draining savings they’d counted on to support their golden years. Think twice before putting your name on the dotted line. It might come back to haunt you.

3. Funding Lavish Weddings or Dream Homes

It’s natural to want to help your children celebrate milestones like weddings or buying their first house. However, lavish spending on these occasions can quickly eat away at your retirement savings. Parents sometimes take out personal loans or raid their retirement accounts to fund big weddings or generous down payments, believing they’ll “catch up later.”

The reality? Most don’t. Once those funds are spent, they can’t be replaced, and the financial hit can be devastating. It’s okay to contribute to life’s big moments, but setting a clear budget that doesn’t compromise your own future is crucial.

4. Providing Ongoing Financial Support

Sometimes, adult children rely on their parents for ongoing help with rent, car payments, groceries, or other everyday expenses. While it might seem like a small monthly contribution, these payments can quietly drain your retirement funds over time. What starts as a temporary bridge during tough times can turn into a long-term financial lifeline that parents can’t easily turn off.

Many retirees are shocked to find themselves supporting their kids well into their own 60s or 70s, long after they planned to enjoy financial freedom. Before offering continuous help, consider whether it’s enabling dependence or hindering your own ability to retire comfortably.

Image source: Pexels

5. Sacrificing Your Own Emergency Fund

Parents often feel compelled to help their children during financial crises, even if it means sacrificing their own emergency savings. Whether it’s covering a medical bill, car repair, or sudden job loss, raiding your nest egg might seem like the right thing to do. But once that cushion is gone, you’re left vulnerable to unexpected expenses in your own life, like health issues or home repairs.

Financial experts recommend prioritizing your own emergency fund before extending help to others. Otherwise, you could find yourself in a financial bind at a time when earning more income is no longer an option.

6. Moving in Together Without Boundaries

Inviting your adult child (and sometimes their family) to move in can sound like a win-win: they save on rent, and you enjoy the company. But without clear boundaries, shared living arrangements can drain your finances faster than you think. Utility bills, groceries, home maintenance, and even additional wear and tear on the house all add up, often without formal rent contributions or shared responsibilities.

Parents who foot the entire bill may find themselves spending hundreds or even thousands each month supporting adult children at home, all while their own retirement plans suffer. Establishing ground rules and financial expectations is key to making multi-generational living work.

7. Letting Guilt Guide Your Decisions

One of the most subtle yet powerful ways parents end up broke in retirement is by letting guilt guide their financial choices. It’s easy to feel obligated to help your kids succeed, especially if they’re struggling. But giving in to guilt often means ignoring your own needs, risking your security for the sake of keeping the peace.

The truth is that financial independence is just as important for parents as it is for kids. Learning to say “no” when necessary and focusing on long-term stability ensures you can continue to support your children emotionally without sacrificing your own well-being.

You Need to Set Boundaries

Supporting your children financially is a loving gesture, but it shouldn’t come at the cost of your own retirement security. By setting boundaries, making informed choices, and prioritizing your own needs, you can strike a balance between helping your kids and protecting your financial future.

Have you ever found yourself giving too much? Or perhaps you’ve learned a valuable lesson about saying no?

Riley is an Arizona native with over nine years of writing experience. From personal finance to travel to digital marketing to pop culture, she’s written about everything under the sun. When she’s not writing, she’s spending her time outside, reading, or cuddling with her two corgis.

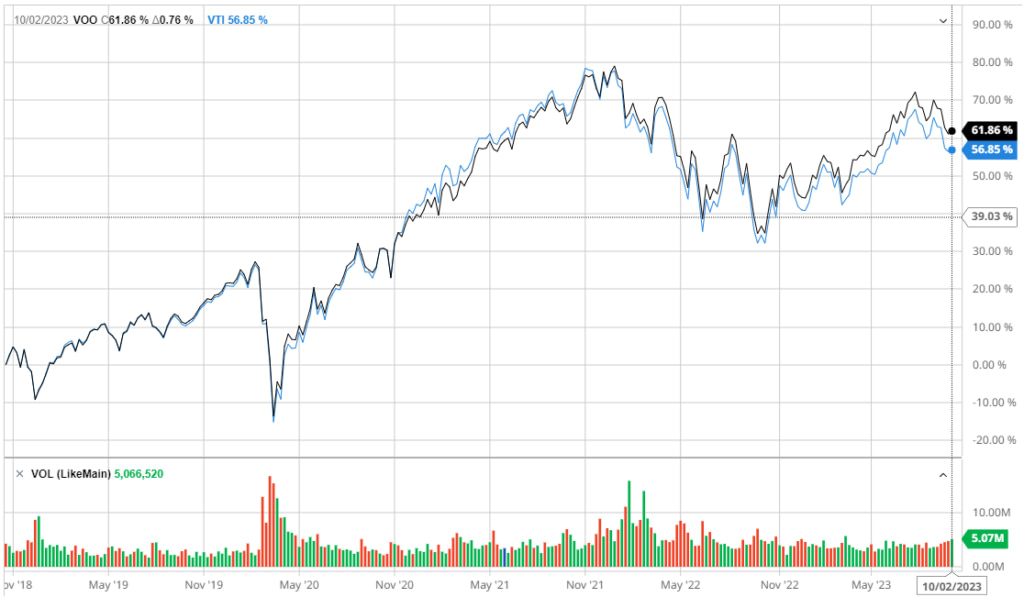

If you’re balancing VTI vs. VOO, you’re probably looking at putting money into an index fund. That’s generally going to be a good decision. Index funds allow you to diversify your portfolio even if you don’t have much to invest, and even investment professionals often fail to pick stocks that beat the index performance.

But which of these funds should you choose? Let’s start with the basics.

The most important difference between VTI and VOO is that each fund tracks a different index:

VTI tracks the CRSP U.S. Total Market index. The CRSP U.S. Total Market index is an index of almost 4000 companies headquartered in the US, from mega to micro capitalization. This makes the index a good representation of the entire US stock market, not just the largest companies.

VOO tracks the S&P 500. The S&P 500 is an index of the 500 top largest companies in the US.

These indices and the ETFs that track them are market cap weighted. That means that they give larger companies a heavier weight.

VTI and VOO use slightly different terms to break down their sector exposure.

VTI Sector Breakdown

Sector

Weight

Information Technology

30.20%

Consumer Discretionary

14.40%

Industrials

13.00%

Health Care

12.60%

Financials

10.30%

Consumer Staples

5.10%

Energy

4.60%

Real Estate

2.90%

Utilities

2.70%

Telecommunication

2.20%

Basic Materials

2.00%

VOO Sector Breakdown

Sector

Weight

Technology

28.20%

Health Care

13.20%

Financials

12.40%

Consumer Discretionary

10.60%

Communication Services

8.80%

Industrials

8.40%

Consumer Staples

6.60%

Energy

4.40%

Real Estate

2.50%

Basic Materials

2.50%

Utilities

2.40%

One thing that immediately stands out in these breakdowns is that both VTI and VOO are heavily weighted toward IT (tech & communication) especially VOO, reflecting the current large market capitalization of these sectors in the US stock market.

VTI tracks a larger number of companies from a wider range of corporate sizes. It is weighted more heavily toward the consumer and industrial sectors, which contain more medium and small-size companies. The larger number of holdings and higher variation in the companies’ profiles make it more diversified.

VOO tracks a smaller number of companies with a slightly greater concentration in tech. It gives a higher part to healthcare and financials, which tend to be dominated by large companies (sometimes referred to as Big Banks and Big Pharma).

Neither of these options is fundamentally better or worse. They provide exposure to slightly different sectors of the market, and that can lead to different performance characteristics.

VTI vs VOO: The Similarities

VTI and VOO have a lot in common. They are both extremely large ETFs. Both funds are managed by Vanguard, which has a reputation for providing low-cost funds.

If you’re looking for large, highly liquid funds with credible management, both of these ETFs will pass your screen.

There are also less obvious similarities, explaining the very similar performance charts stemming from three basic facts.

As market cap-weighted indexes, they both give a predominant space to mega-caps worth trillions of dollars, most of them tech companies.

A lot of the performance of the CRSP U.S. Total Market Index is driven by the top largest holdings, which are all part of the S&P 500.

The stock market value of mid and small-cap stocks tends to move in unison with larger-cap stocks.

What does that mean in practice? Let’s look at the ten largest holdings of VTI and VOO.

Top Holdings: VTI vs VOO

The top holdings of both indexes are identical for the first 9th largest holdings, only in a slightly different order. It includes:

Apple Inc.

Microsoft Corp.

Amazon.com Inc.

NVIDIA Corp.

Alphabet Inc. Class A

Alphabet Inc. Class C

Tesla

Facebook Inc. Class A

Berkshire Hathaway Inc. Class B

So the only difference among the top 10 holdings is that VTI contains insurance and healthcare stock UnitedHealth Group while VOO contains oil & gas Exxon Mobil Corp.

The same can be true even if looking at the next 10 holdings for each fund. The list is identical for 9th of them, with a very similar order:

Exxon Mobil Corp or UnitedHealth Group

Eli Lilly & Co.

JPMorgan Chase & Co.

Visa Inc. Class A

Johnson & Johnson

Broadcom Inc.

Procter & Gamble Co.

MasterCard Inc Class A

Home Depot

The difference is in the 20th largest holdings: pharmaceutical company Merck & Co Inc. for VTI and energy company Chevron Corp. for VOO.

The only real difference is for the top holdings of VTI to be slightly less of the whole ETF, making space for the smaller holdings of smaller companies.

Which Is Best for You?

Both VTI and VOO are good choices for an investor who is looking for a quality diversified index fund. Both are among the largest and most prominent ETFs in the country, both are highly liquid, and they have very similar track records. They also have the same low fee of 0.03%.

Your choice will be based on what you are looking for in an investment.

VTI is giving some exposure to companies with a smaller market capitalization. This gives a slightly different profile when looking at the sector basis, giving more importance to the industrial and consumer sectors.

VOO is a more aggressive, less diversified fund focused on major tech companies. This gives it greater potential for gains in bull market periods but also opens up the possibility of significant losses in a bear market.