St. Benilde Lady Blazers’ Mycah Go during the PVL Rookie Draft Combine. –PVL PHOTO

MANILA, Philippines — Former NCAA MVP Mycah Go is juggling College of Saint Benilde’s four-peat bid in the ongoing Season 100 and her dream to enter the PVL—officially, this time.

Go was signed by Farm Fresh when it joined the league two years ago but never suited up due to an ACL injury. That’s why she has to go through the 2025 PVL Rookie Draft on June 8 at Novotel.

“I’m definitely excited. I’ve been wanting to go pro for a long time, and now that it’s finally happening, it feels great,” Go told reporters in Filipino. “Just like everyone else, I’m really excited to take the next step into the pro league.”

The Lady Blazer is eager to prove herself again to earn a spot, even while still competing in the NCAA.

Mycah Go (in white) says losses taught them lessons. —CONTRIBUTED PHOTO

On Friday, Go dropped by the Draft Combine at Paco Arena before heading to FilOil EcoOil Centre, where she helped St. Benilde complete a second-round sweep with a 25-20, 25-18, 25-12 win over Lyceum to enter the Final Four with a 16-2 record.

Article continues after this advertisement

“That’s how it is. Once the NCAA ends, this is the next step. So I really have to be prepared,” Go said.

Her CSB teammates Clo Mondoñedo, Mich Gamit, and Gayle Pascual made their PVL playoff debuts with ZUS Coffee during its breakout 2024–25 All-Filipino campaign.

Go is not rushing her way to catch up to the pro achievements of her fellow Lady Blazers Al she wants is to help the team that will trust her in the draft.

“I’m very open and willing to learn whatever a team needs from me. I really want to contribute in any way I can,” she said. “I feel very ready. But since I’m coming from an injury, I just want to keep improving consistently.”

Your subscription could not be saved. Please try again.

Your subscription has been successful.

Go is determined to apply all her learnings from CSB and ZUS coach Jerry Yee, who accompanied her on Day 1 of the combine.

“I’ve learned a lot from Coach Jerry. He really helped me grow. So whoever picks me in the pros, I feel like I’ll be bringing everything I learned from him to the team,” she said.

The stark reality for legal practices today is this: The sensitive client information you handle makes you a prime target for a law firm data breach. Yet, despite the increasing cyber threat to lawyers, many still rely on insufficient insurance policies that leave them exposed to data breaches when it matters most. In fact, more than half of all firms have inadequate coverage.

When it comes to cybersecurity, the gap between awareness and action is growing, and the consequences can be extremely costly. In this article, we’ll break down the unique ways law firms are vulnerable to data breaches and where standard insurance policies fall short. Plus, we’ll cover the steps you can take to assess and improve your coverage before a breach hits.

The disconnect between awareness and action in legal cybersecurity

It’s not that law firms don’t understand the risks. In fact, cybersecurity routinely ranks as a top concern for managing partners and compliance teams. But despite this growing awareness, recent data shows that 52% of law firms believe their current insurance policies would only partially cover their firm in the event of a data breach, if at all. Even more surprising is that only 14% said they planned to expand their coverage in the near future.

So, what’s causing this hesitation? For many firms, it’s a mix of practical constraints and misplaced confidence.

For many lawyers, it’s tempting to assume that a general liability policy or a basic cyber endorsement is “good enough.” But the fact of the matter is that general liability and malpractice policies do not cover security incidents or data breaches.

Insurance policies can be time-consuming and confusing to read, so in some cases, firms may not fully understand the scope of their coverage. Attorneys may mistakenly think they’re already fully covered until a breach occurs and the fine print tells a different story.

The result is a dangerous gap between perceived protection and actual risk exposure. This gap can lead to serious financial, reputational, or regulatory fallout for lawyers.

Why are law firms prime targets for data breaches?

Law firms are typically holding onto a goldmine of sensitive data about their clients. It makes them incredibly attractive to cybercriminals.

It’s a problem highlighted by the increase in attacks the legal industry has been experiencing. Law360 Pulse reported in 2023 that breaches for law firms had doubled from the year before, while another report found a 68% increase in that period, with 636 weekly attacks.

Here’s a breakdown on why law firms are increasingly in the crosshairs for potential breaches.

Handling extremely sensitive client data

Clients trust their law firms with some of the most confidential information they have. This may include financial records, intellectual property, M&A strategy, litigation documents, and personal identifiers. This data is highly valuable to cybercriminals, as it can contain information that they can weaponize against both firms and clients.

For retail or healthcare companies, data breaches might result in quick sales on the dark web. But the data held by law firms is much easier to use for targeted extortion and insider trading. It can also lead to long-game phishing attacks.

With the stakes this high and clients increasingly aware of it, more and more clients are building cybersecurity standards into non-negotiable parts of engagement. Firms that can’t prove strong data protection may lose out on business.

Subject to ethical and confidentiality obligations

Confidentiality is a cornerstone of any legal practice, so law firms are ethically and professionally obliged to protect client data. Any breach has the potential to jeopardize attorney-client privilege, and this can violate bar regulations and trigger disciplinary action.

The challenge for firms is that ethical duties don’t pause for technical limitations. If a breach occurs because your systems are outdated, or you have unclear protocols or weak insurance coverage, it doesn’t lessen the consequences.

Courts and regulatory bodies expect firms to take reasonable steps to safeguard client information before, during, and after a cyber event.

Reliance on legacy systems and inconsistent IT practices

Many law firms still operate on outdated software, older infrastructure, or IT setups that haven’t kept pace with evolving cyber threats. Midsize and boutique firms are particularly prone to these issues.

Other factors like bring-your-own-device (BYOD) policies, remote work habits, and different tech capabilities across offices lead to fragmented environments that are more difficult to keep secure.

Even firms with internal IT teams in place can lack dedicated cybersecurity expertise. This can leave blind spots, especially in areas like endpoint security and threat detection. Hackers are incredibly savvy and are aware of this. They specifically look for easy entry points in firms with weak controls or inconsistent IT systems.

Working with high-profile and high-net-worth clients

Working with corporate executives, celebrities, political figures, or well-known brands can put a target on your firm’s back. These high-value targets may attract cyber criminals who are after sensitive information — especially if they can use it for extortion purposes.

Attackers are also motivated by how connected you might be to other, higher-priority systems. For example, if you work with a Fortune 500 client and your systems are easier to breach than theirs, you’re the more efficient target.

Leveraging complex vendor and third-party relationships

Like any company today, your law firm likely relies on a wide range of third-party vendors when it comes to tech. This can be anything from cloud storage to e-discovery tools or even how you manage payroll. Every single touchpoint in your technology stack represents a new layer of exposure. In fact, 61% of respondents to a survey said they experienced a third-party data breach or other security incident in the last 12 months.

You might have your internal systems locked down, but a breach through a vendor can still compromise your firm’s (and your client’s) data. And under many regulations, this means you’re still on the hook for the breach. That’s why proper vendor vetting and contractual protections are crucial. Otherwise, these relationships can quietly become one of your firm’s biggest cyber risks.

Not adequately investing in cybersecurity infrastructure

Talent and billable hours are traditionally the biggest expenses for law firms. However, this generally means that other operational areas, such as cybersecurity, can be underfunded or placed lower on the priority list.

But this short-term cost-saving approach can backfire since the average cost of a data breach in 2024 was $4.88 million.

From firewalls to email filtering and staff training, every layer of defense against cyberattacks matters. Threats to law firms are getting more and more sophisticated, and so are the tools and technology your firm needs to use to stop them. Without consistent monitoring and investment in people and systems to prevent data breaches, even the most well-intentioned firms can find themselves vulnerable.

Evolving regulatory and compliance pressures

The regulatory framework around law firm cybersecurity is only getting more complex. American Bar Association (ABA) guidance, data breach regulations, and regional privacy laws are constantly evolving, making it challenging to stay current.

If you’ve got what passed for “secure enough” even five years ago, it likely no longer meets today’s expectations.

Many firms find themselves scrambling to interpret or comply with new requirements, particularly when it comes to matters such as breach notification timelines or industry-specific obligations. Falling short risks financial penalties and can damage client trust and open the door to litigation.

What standard law firm insurance policies miss

Many firms still assume their general liability or professional liability policies will protect them in the event of a cyberattack. But according to recent data, only 40% of law firms have cyber liability insurance, which is actually down from 46% the previous year.

This is because, at first glance, your policy may appear to cover cyberattacks. But standard policies often exclude critical cyber-related losses like ransomware payments, regulatory fines, or data restoration.

Even those with so-called “cyber endorsements” (an addition to your existing policy) often find they only cover a small portion of costs, like breach notification or credit monitoring. It can leave massive gaps in areas that matter most to law firms.

And when an incident does occur, providers will often provide specialized legal, IT, or PR experts to help you manage the crisis. It’s an extremely helpful aspect of these policies that ensures you’re not left scrambling.

Self-assessment: Does your firm have gaps in its current insurance coverage?

It’s important not to let cyber insurance be a guessing game. But, like with lots of insurance policies, many law firms only really dig into theirs after a breach — and by then, it’s too late. A proactive review helps to uncover important blind spots and align your coverage with real-world risks.

Here’s a step-by-step guide to help your firm evaluate your current cyber insurance and take proactive measures to identify where gaps may exist.

1. Review your existing policies

Start with what you have and examine your policies across general liability, professional liability, and any cyber endorsements you have. Identify:

What’s covered

What’s excluded

Whether you have a standalone cyber policy

When your policy was last reviewed

2. Identify your firm’s unique risks

No two firms are the same in terms of the clients they serve, the areas of law they operate in, and how their existing IT set-up looks.

Know the exact conditions required for your policy to respond. Some policies won’t activate without a formal breach declaration or regulatory involvement. This can delay your response and increase financial and reputational risks.

4. Review policy exclusions and sub-limits

Even if a policy looks strong at first glance, it can have significant gaps buried in the fine print. Look out for exclusions in your cyber coverage as well as carve-outs that relate to social engineering, employee error, vendor failure, or caps on ransomware payments.

5. Assess business interruption and downtime scenarios

Malware attacks, for example, cause significant business disruption, which can be the costliest part of a breach. Check your policy thoroughly or, if you don’t have a cyber-specific policy yet, identify the types of outages and delayed work you would need compensation for during an attack. Closing these gaps helps mitigate significant revenue losses from business disruption.

6. Compare your coverage against industry benchmarks

What are similar-sized firms in your space insuring against? Brokers and legal industry reports can help you see how your policy measures up against peer standards and industry best practices.

7. Consult an insurance broker who specializes in legal risks

Generalist brokers may not be fully aware of law firm-specific exposures. Work with someone who understands attorney-client privilege, confidentiality obligations, and the unique structure of legal operations to make sure you close as many gaps as possible in your policy. At Embroker, we create insurance policy packages with law firms in mind.

8. Use risk modeling tools and outside audits

Cyber risk isn’t a one-size-fits-all approach, so consider consulting a broker or IT provider to explore modeling tools that quantify your exposure. External audits can also help validate your policy against your real-world risk.

9. Review vendor and third-party risk exposure

We’ve discussed the type of risk you’re exposed to from third-party technology and vendors in the event that they themselves experience a breach. Make sure your policy accounts for vendor breaches and includes clear coverage for third-party liability.

10. Evaluate client contract requirements

Some clients require proof of cyber insurance (or even specific limits) as a condition of doing business. Failing to meet these expectations can cost you work or create liability conflicts.

11. Check for coverage of reputational harm and PR support

Rebuilding client trust after a data breach is hard work, so look for policies that include PR and crisis communications support. This helps you to manage the fallout from a breach effectively and protect long-term relationships.

12. Incorporate your insurance into your incident response plan

Your cyber policy and your breach response plan should be in sync. Review both your cyber policy and incident response plan to make sure your firm is sufficiently covered. Ask yourself:

Who’s responsible for what issues

How do you contact your insurer in a crisis

What resources will be provided

This is a good opportunity to evaluate your incident response plan, since only 26% of law firms believe their firm is “very prepared” to respond to cyber incidents.

13. Test and update your coverage annually

Cyber risks evolve constantly, and they’re increasing in volume and complexity. Set a schedule to revisit your coverage every year, especially if you’re adding new technology or taking on bigger clients. Even small updates to your operational processes can produce new risks, and an annual review helps you to stay on top of them.

Best practices for managing cyber risk and coverage

Insurance is just one piece of the puzzle. Here are a few essential best practices you can implement to strengthen your risk posture and complement your insurance coverage:

Prioritize cyber hygiene with strong passwords, multifactor authentication, and keeping software and systems up-to-date.

Train your team regularly to avoid breaches that start with human error. Invest in ongoing training to help staff spot phishing attempts and follow security protocols.

Develop a clear incident response plan so you know exactly what steps to take if a breach occurs, and align your cyber policy with this plan.

Audit vendors and third parties with the same scrutiny as you do to your own systems because their security gaps can quickly become yours.

Document everything from IT policies to employee training logs, as this is typically required for insurance claims and compliance audits.

Strong cyber coverage is essential, but you can make it even more effective by integrating it as a core component of your overall risk management strategy.

Close your coverage gaps before they cost you

Cyber threats against law firms aren’t slowing down. Take the time to audit your current coverage and assess your firm’s risks by diving into our 2024 Legal Risk Index Report to stay ahead of emerging risks. At Embroker, we work closely with law firms to craft insurance packages that close coverage gaps and protect you and your clients. Get a quote today!

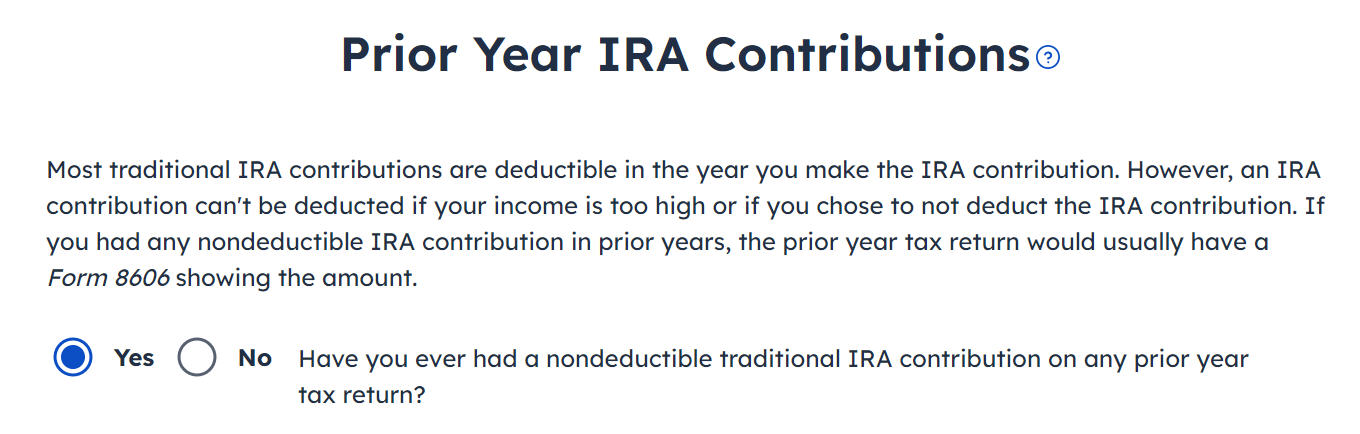

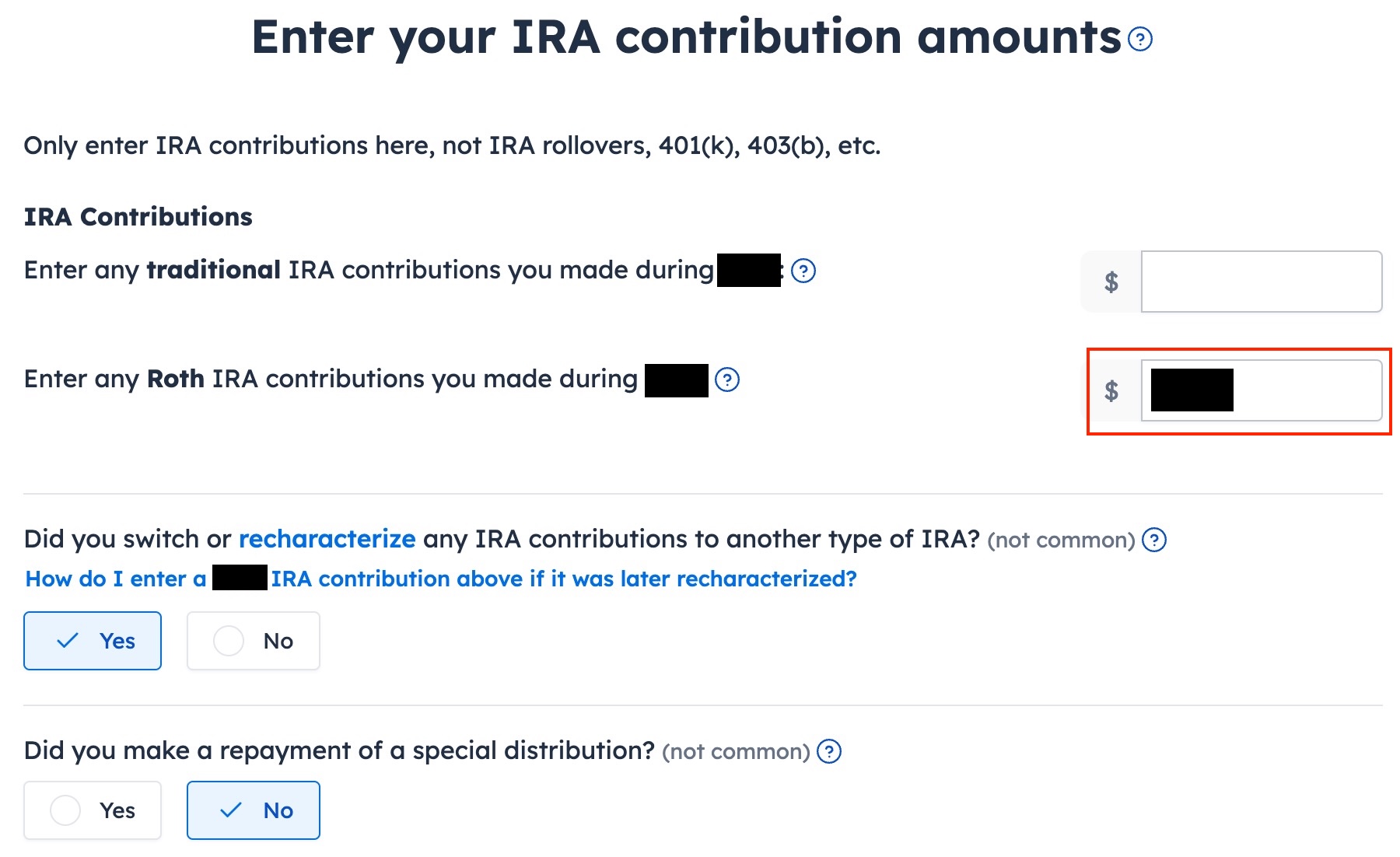

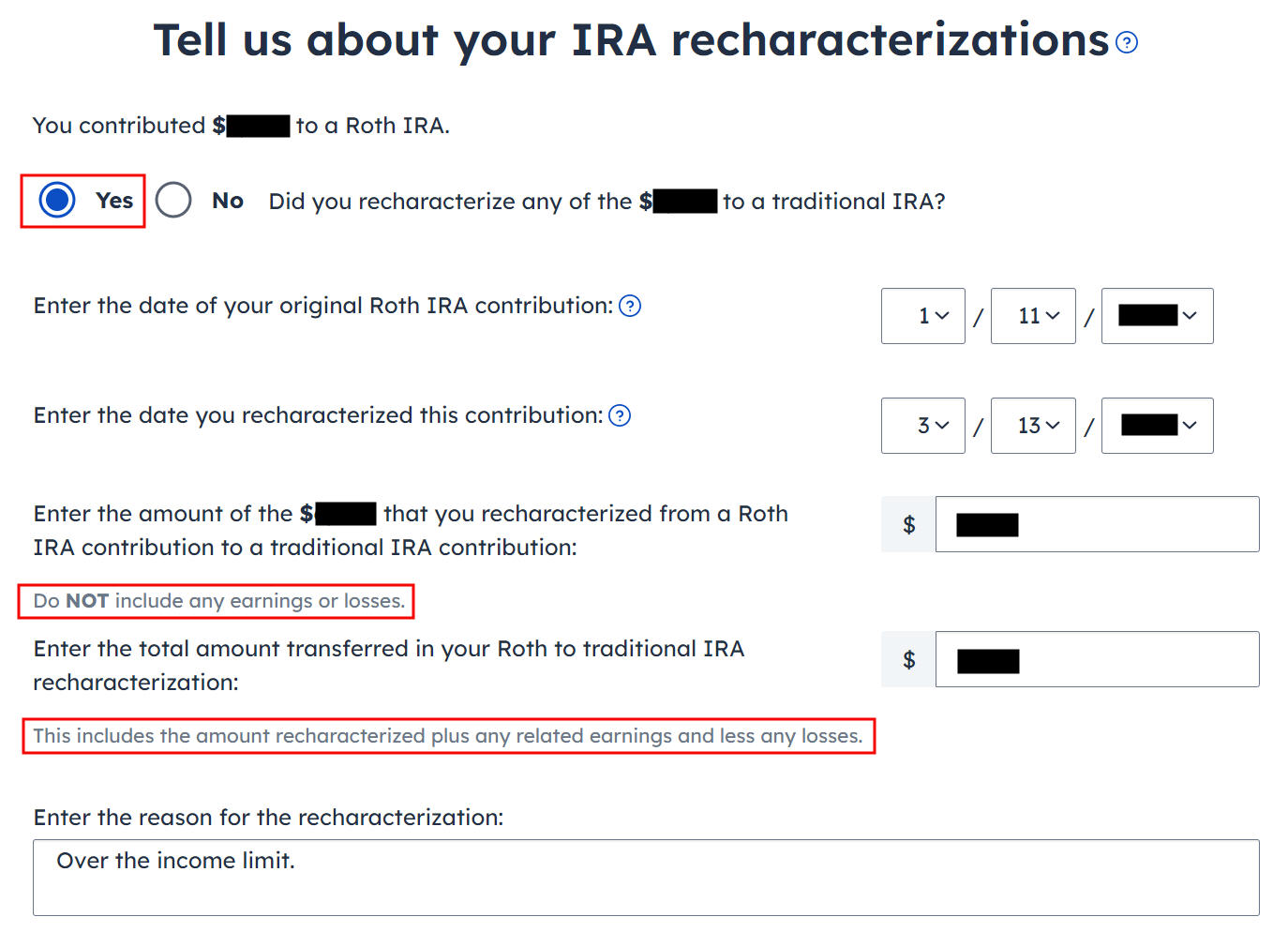

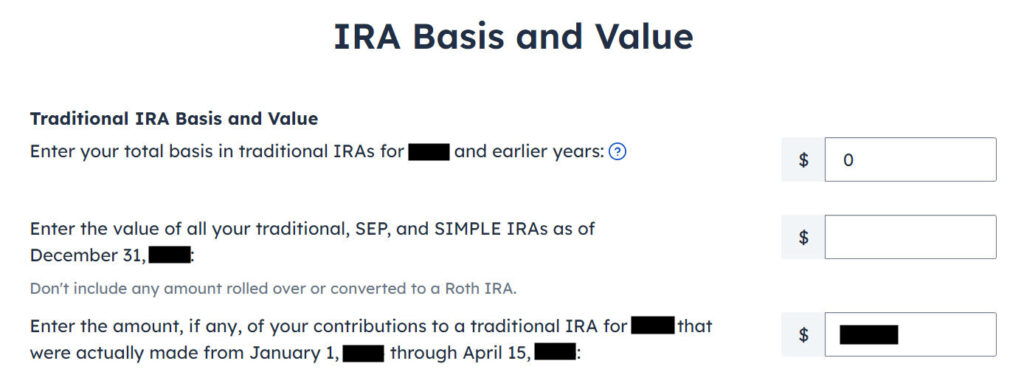

You may have contributed to a Roth IRA and then realized later in the same year that you would exceed the income limit. You recharacterized the Roth IRA contribution as a Traditional IRA contribution and converted it to Roth again before the end of the year. Your IRA custodian sent you two 1099-R forms, one for the recharacterization and one for the conversion. This post shows you how to put them into FreeTaxUSA.

Here’s the example scenario we’ll use in this guide:

You contributed $7,000 to a Roth IRA for 2024 in 2024. You realized that your income would be too high later in 2024. You recharacterized the Roth contribution for 2024 as a Traditional contribution. The IRA custodian moved $7,100 from your Roth IRA to your Traditional IRA because your original $7,000 contribution had some earnings. The value increased again to $7,200 when you converted it to Roth before December 31, 2024. You received two 1099-R forms, one for $7,100 and another for $7,200.

If you’re married and both you and your spouse did the same thing, you should follow the steps below once for yourself and again for your spouse.

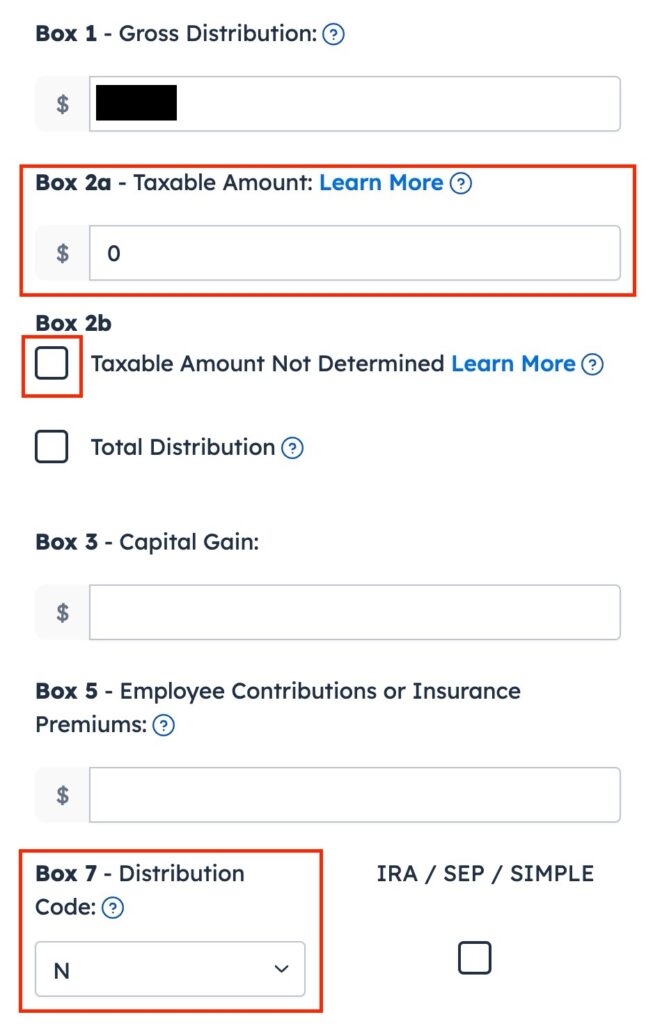

1099-R for Recharacterization

We handle the 1099-R form for the recharacterization first. This 1099-R form has a code “N” in Box 7.

Find “Retirement Income (1099-R)” under the Income menu.

Click on the “Add a 1099-R” button.

It’s just a regular 1099-R.

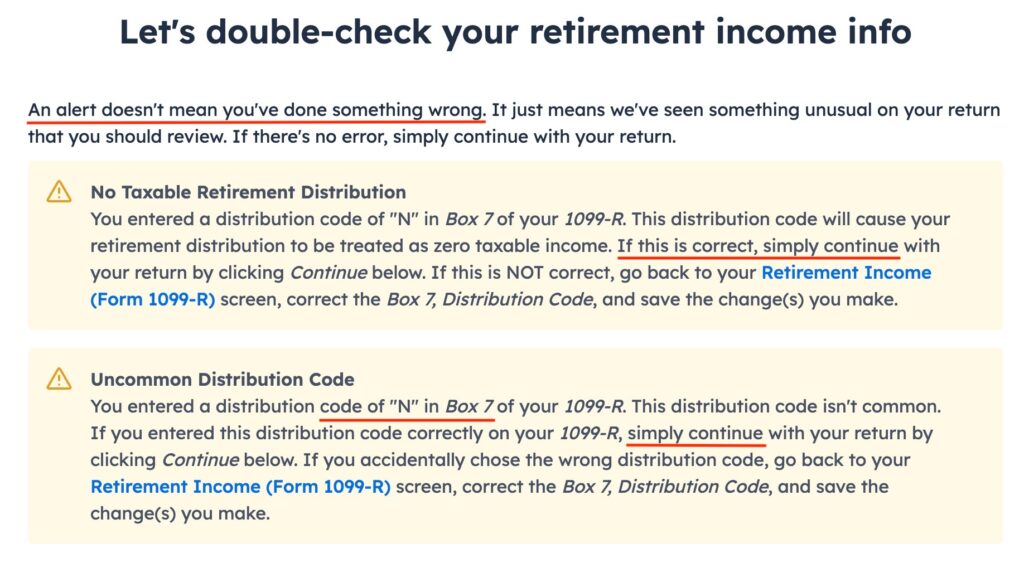

The 1099-R form for the recharacterization shows the amount moved from the Roth IRA to the Traditional IRA in Box 1. It’s $7,100 in our example. The taxable amount is 0 in Box 2a and the “Taxable amount not determined” box isn’t checked. The code in Box 7 is “N” and the “IRA/SEP/SIMPLE” box may or may not be checked. It isn’t checked in our sample form.

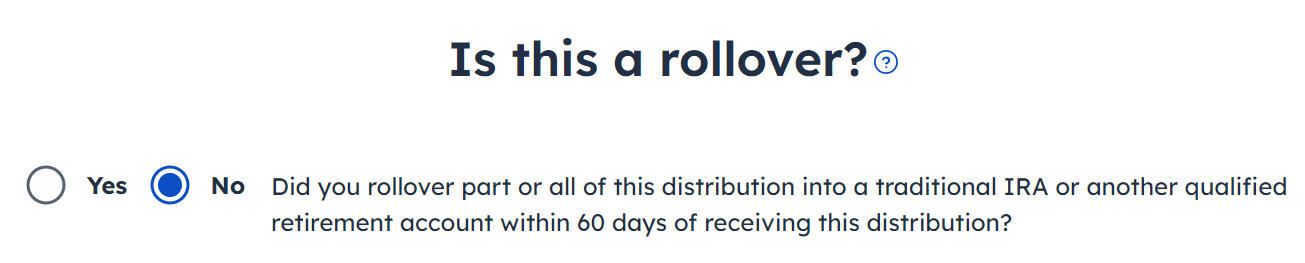

The recharacterization wasn’t a rollover.

FreeTaxUSA shows some alerts just to double-check. The zero taxable income on the 1099-R is correct. Code “N” in Box 7 is also correct.

You’re done with the 1099-R form for the recharacterization. Click on the “Add a 1099-R” button to add the other 1099-R for the conversion.

1099-R for Conversion

The 1099-R for the conversion has a code “2” in Box 7 if you’re under age 59-1/2 or a code “7” if you’re 59-1/2 or older.

It’s also a regular 1099-R.

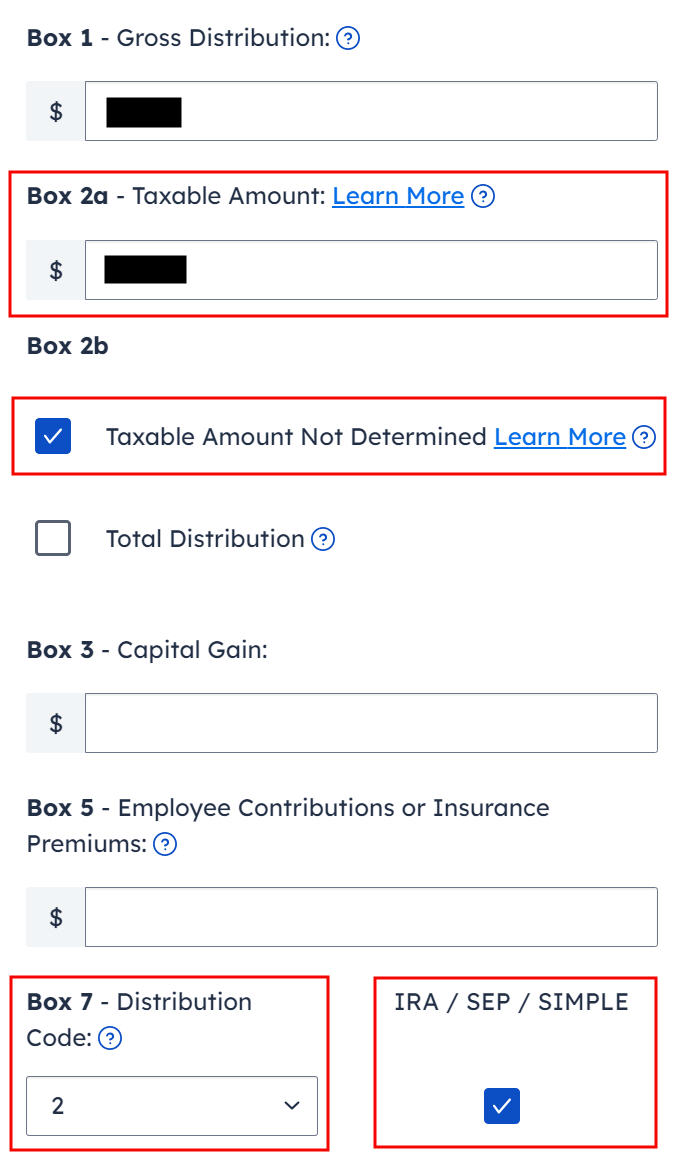

Box 1 shows the amount converted to Roth. It’s $7,200 in our example. It’s normal to have the same amount as the taxable amount in Box 2a when Box 2b is checked saying “taxable amount not determined.” Make sure to choose the correct code in Box 7 to match your 1099-R. The “IRA / SEP / SIMPLE” box is checked.

Your refund number drops after you enter this 1099-R. Don’t panic. It’s normal and temporary. The refund number will come up when we finish everything.

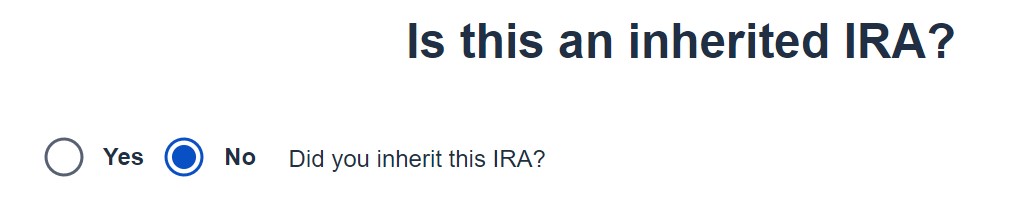

It’s not an inherited IRA.

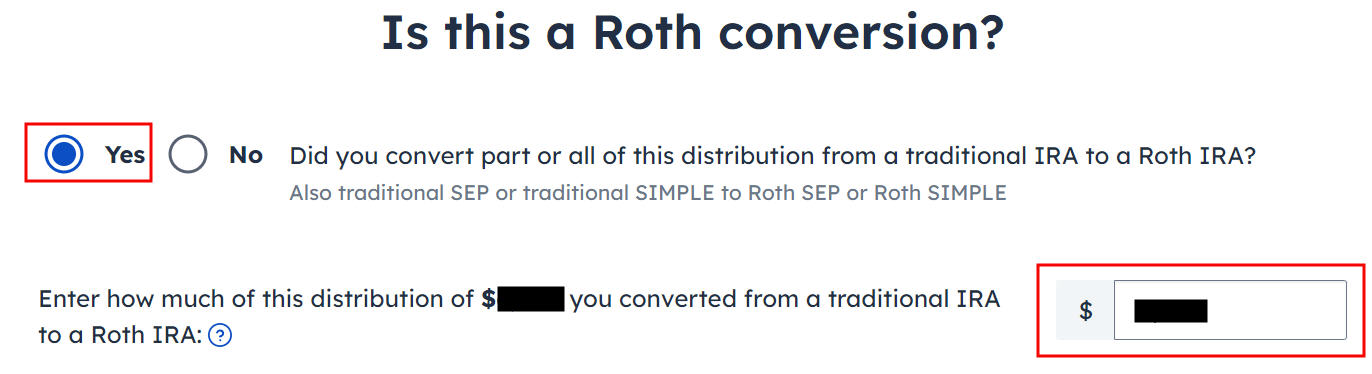

It’s a Roth conversion. 100% of the amount on the 1099-R was converted from a Traditional IRA to a Roth IRA.

You are done with this 1099-R for the conversion. Repeat if you have another 1099-R. If you’re married and both of you converted to Roth, pay attention to whose 1099-R it is when you enter the second one. You’ll have problems if you assign both 1099-R forms to the same person when they belong to each spouse. Click on “Continue” when you have entered all the 1099-R forms.

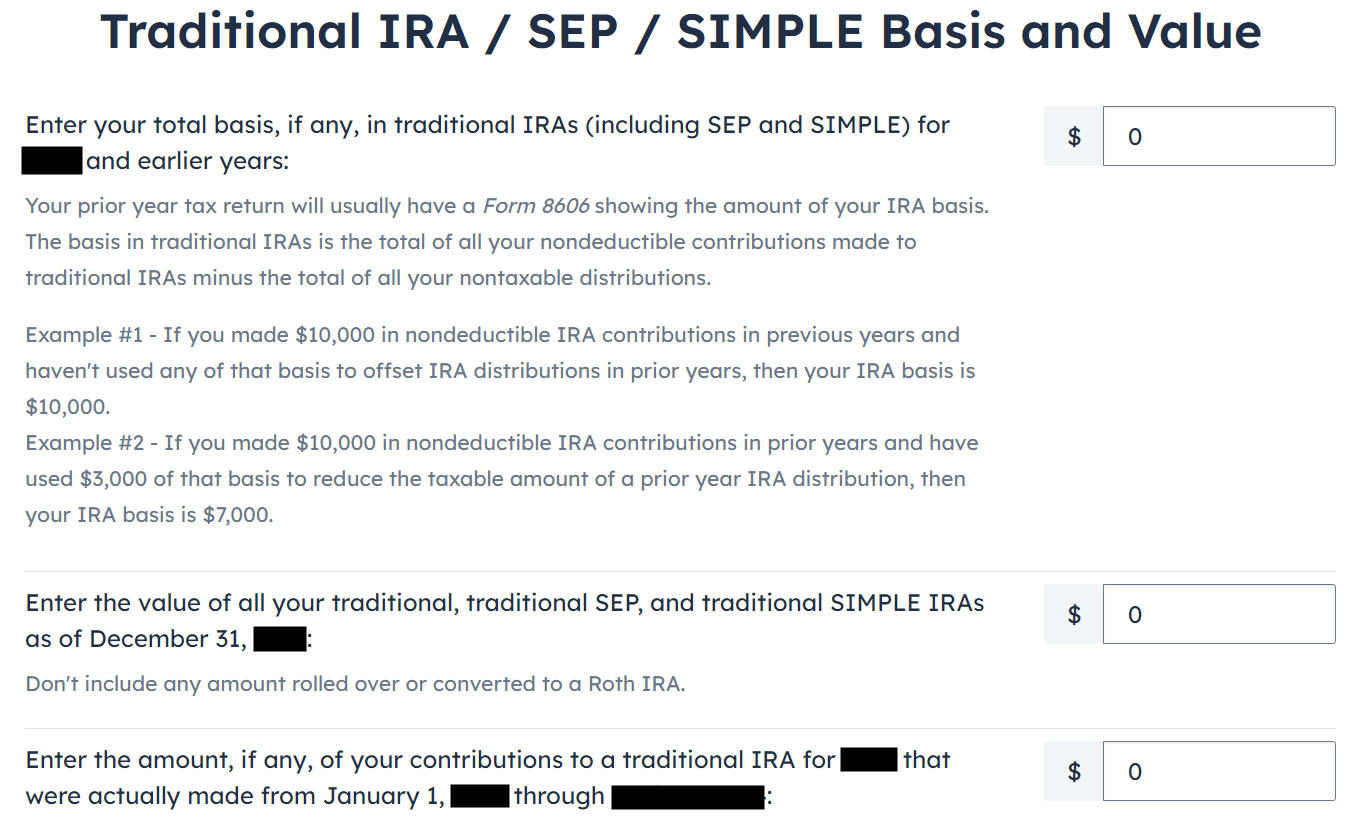

It asks you about the basis carried over from previous years. If you never contributed to a Traditional IRA in previous years, you can answer “No.” Answering “Yes” and entering a zero on the next page has the same effect as answering “No.” If you have gone back and forth before you found this guide, some of your previous answers may be stuck. Answering “Yes” here will give you a chance to review and correct them. If you have a basis carryover on line 14 of Form 8606 from your previous year’s tax return, answer Yes here and enter it on the next page.

The value in the first box should be zero if you never contributed to a Traditional IRA in previous years. If you had a small amount of earnings posted to your Traditional IRA after the conversion and you didn’t convert the earnings, enter the account’s value from your year-end statement in the second box. The third box should be zero because you recharacterized before the end of the year.

We didn’t take any disaster distribution.

Now continue with all other income items until you are done with income. Your refund meter is still lower than it should be but it will change soon.

Recharacterized Contribution

Now we tell FreeTaxUSA that we contributed to a Roth IRA before we recharacterized the contribution to a Traditional IRA.

Contributed to Roth IRA

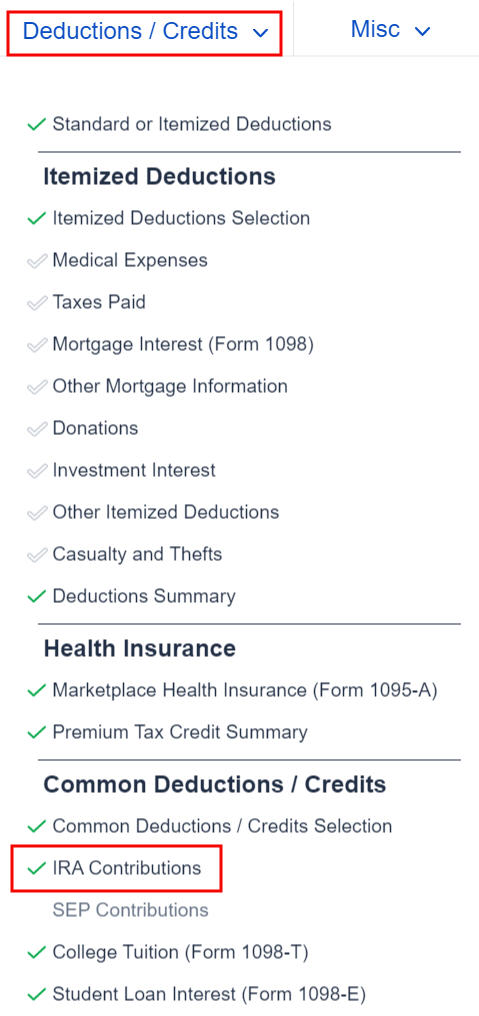

Find the IRA Contributions section under the “Deductions / Credits” menu.

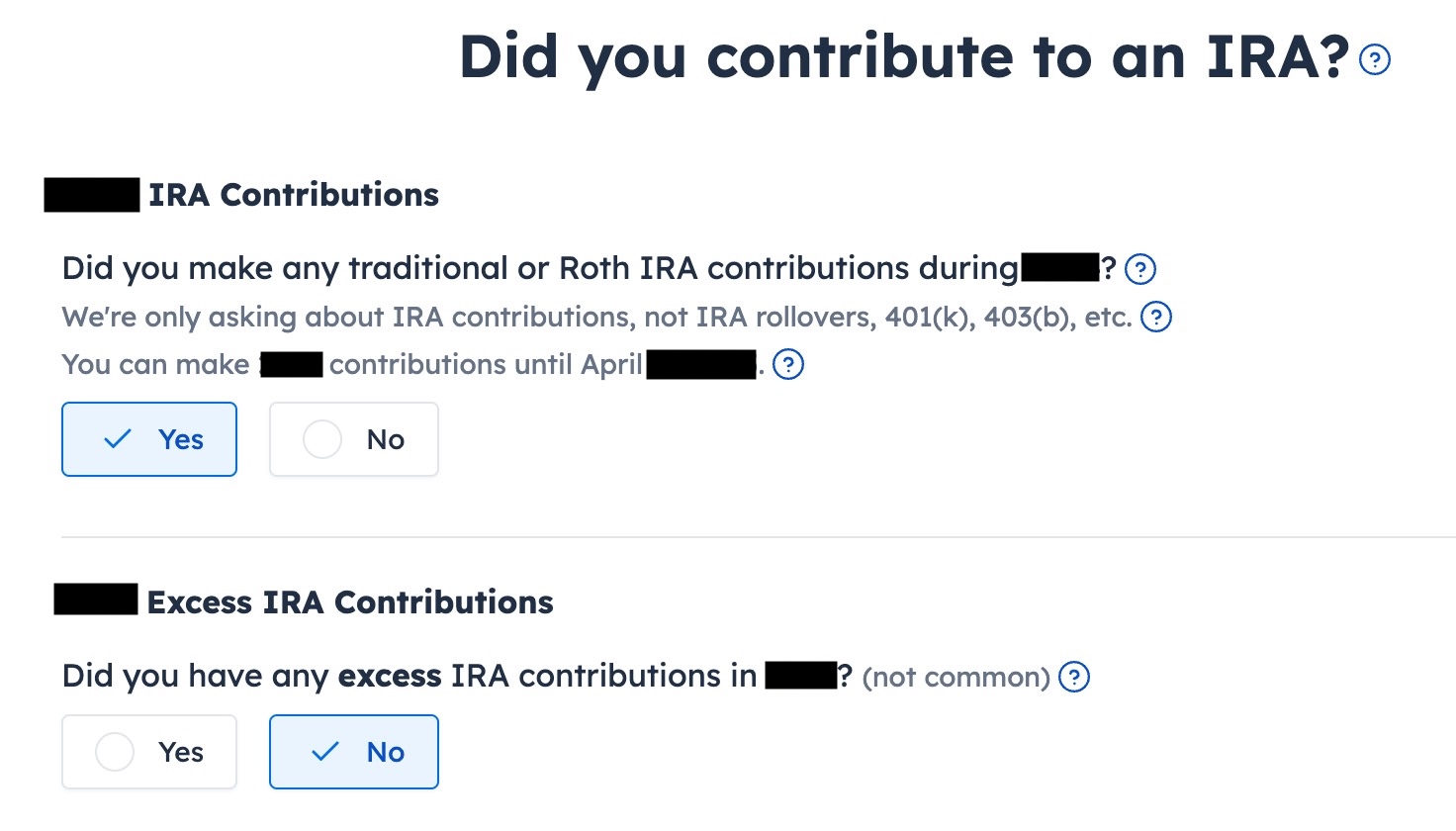

Answer “Yes” to the first question. An excess contribution means contributing more than you’re allowed to contribute. We didn’t have that.

Enter your contribution in the second box because you originally contributed to a Roth IRA. Answer “Yes” to “Did you switch or recharacterize.” We didn’t repay any special distribution.

Recharacterized to Traditional

Select “Yes” to confirm you recharacterized a contribution. It opens up additional inputs for an explanation. If you recharacterized 100% of your original contribution, enter it in the first box. It’s $7,000 in our example. We enter $7,100 from our example in the second box, which is the amount that the IRA custodian moved from the Roth IRA to the Traditional IRA when we recharacterized.

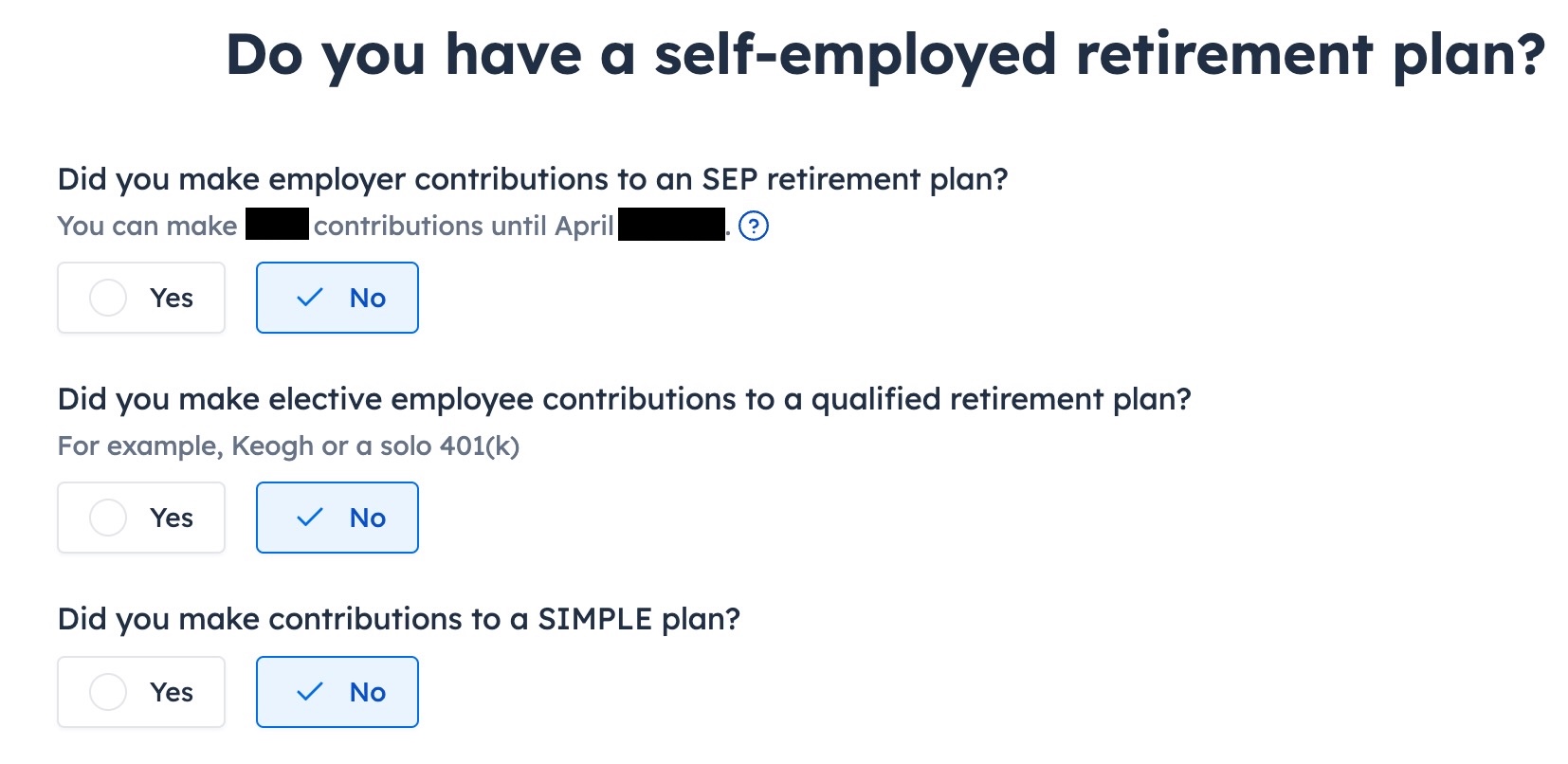

We didn’t contribute to a SEP, solo 401k, or SIMPLE plan. Answer “Yes” if you did.

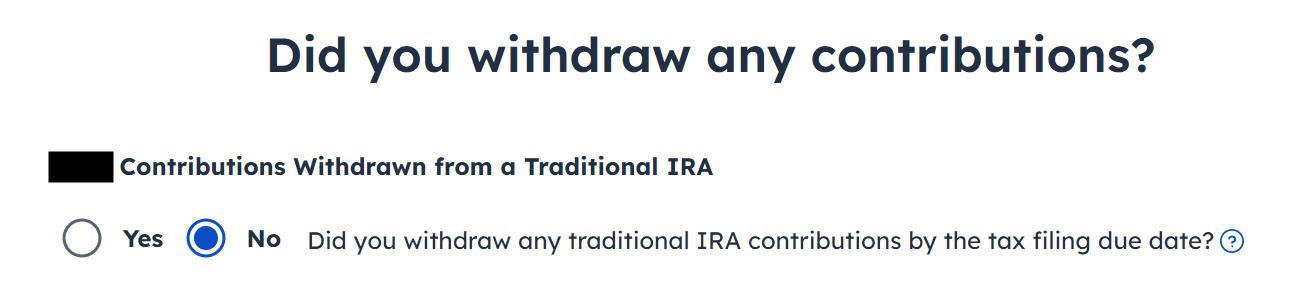

Withdraw means pulling money out of a Traditional IRA back to your checking account. Converting to Roth is not a withdrawal. Answer “No” here.

The value in the first box should be zero if you never contributed to a Traditional IRA in previous years. The value in the second box should also be zero if you converted everything. If you had a small amount of earnings posted to your Traditional IRA after the conversion and you didn’t convert the earnings, enter the account’s value from your year-end statement in the second box. The third box should be zero because you recharacterized before the end of the year.

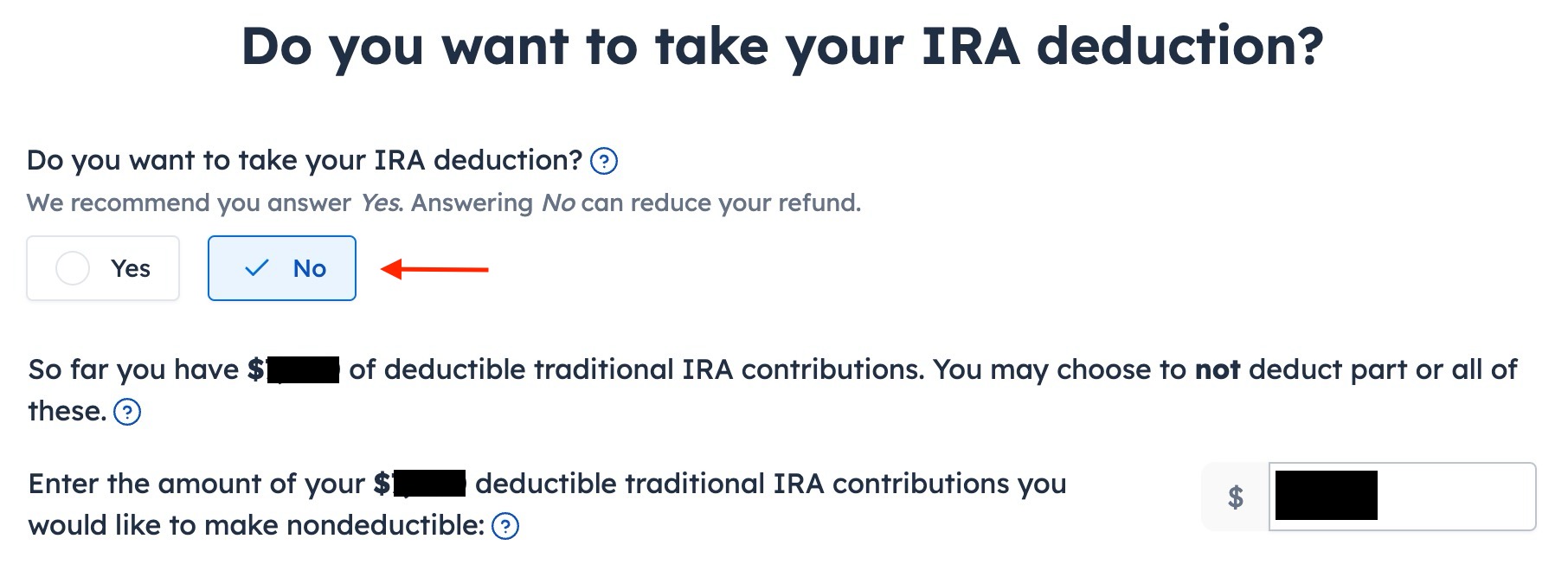

You see this screen only if your income falls below the income limit that allows a deduction for a Traditional IRA contribution. You don’t see this if your income is above the income limit. Answering Yes will make your contribution deductible but it will also make your Roth conversion taxable, which comes to a wash. It’s less confusing if you answer “No” here and make the entire amount that could be deducted nondeductible.

It tells us we don’t get a deduction because our income was too high or because we chose to make our contribution nondeductible. We know. That’s why we did the Backdoor Roth.

The refund meter should go back up now.

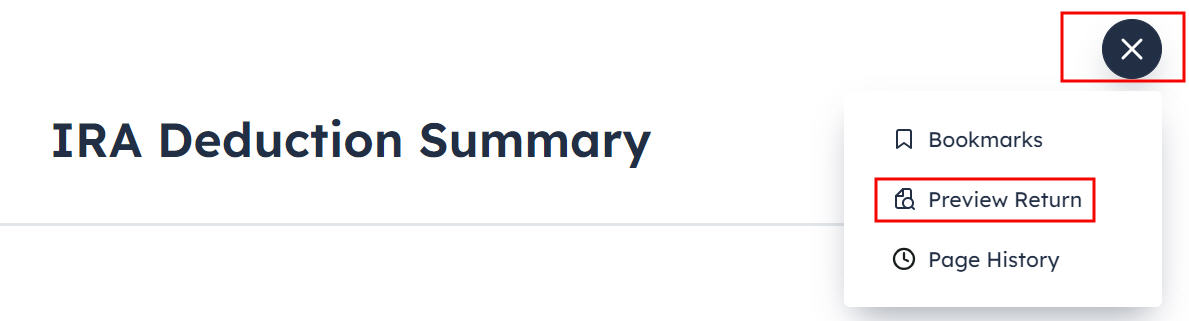

Taxable Income

Let’s look at how these entries show up on our tax return. Click on the three dots on the top right above the IRA Deduction Summary and then click on “Preview Return.”

Look for Lines 4a and 4b in your Form 1040.

It shows the sum of your two 1099-R forms on line 4a and only $200 is taxable on line 4b. The taxable amount is the difference between the amount you converted to Roth and your original contribution.

Form 8606

Go toward the end of the pop-up to find Form 8606. It shows these for our example:

Line #

Amount

1

7,000

3

7,000

5

7,000

13

7,000 *

16

7,200

17

7,000

18

200 *

footnote

* From Worksheet-1-1 in Publication 590 B

Form 8606

There’s also a statement to describe your recharacterization at the end.

Troubleshooting

If you followed the steps in this guide and you are not getting the expected results, here are a few things to check.

The Entire Conversion Is Taxed

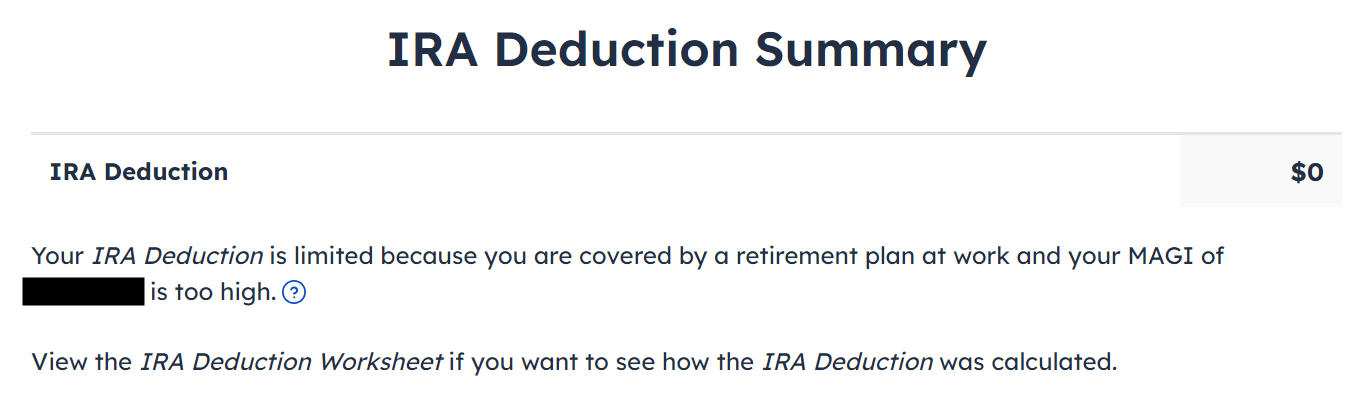

If you don’t have a retirement plan at work, you have a higher income limit to take a deduction on your IRA contribution. If you have a retirement plan at work but your income is low enough, you are also eligible for a deduction on your IRA contribution. FreeTaxUSA gives you the option to take a deduction if it sees that your income qualifies.

Taking the deduction makes a corresponding amount of the Roth conversion taxable. Answering “No” in the “Do you want to take your IRA deduction?” page will have you taxed only on the earnings in your Roth conversion.

Self vs Spouse

If you are married, make sure you don’t have the 1099-R and the IRA contribution mixed up between yourself and your spouse. If you inadvertently assigned two 1099-Rs to one person instead of one for you and one for your spouse, the second 1099-R will not match up with an IRA contribution made by a spouse. If you entered a 1099-R for both yourself and your spouse but you only entered one IRA contribution, you will be taxed on one 1099-R.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

I just read an excellent book The Beck Diet Solution by Dr. Judith Beck. I was looking for a book applying cognitive behavioral therapy to weight loss, and came up with this one in a search on Amazon. CBT is excellent for improving negative thought patterns that affect our behavior. I personally notice negative thoughts leading to bad eating habits especially snacking (like when the little voice of temptation whispers “what could it hurt just this once?”) and I figured others might also, and CBT might help with this. It turns out Dr Beck’s father was a CBT pioneer and she is well versed in this, and excellently qualified to write this book.

I have gone several weeks avoiding snacking between meals and unplanned eating at mealtimes, my two downfalls. The first couple of weeks I had to gut it out, but afterwards it has gotten easier due to applying techniques from this book. For clarification, Dr. Beck means “diet” in the sense of a healthy way of eating, not some fad diet. Each chapter of the book has a section “what are you thinking”, about what Dr. Beck calls “sabotaging thoughts”, and how to respond to them. Very helpful.

The most inspirational part of the book was when she described having to put her young son on the ketogenic diet as treatment for epilepsy. Keto has good success for that purpose, but this is an extreme diet to have to put a young kid on. Fortunately it worked for the epilepsy, but he had to endure it for six years! Imagine the discipline required, no treats, no in between meal snacks, and a strict diet at mealtime, and going to school and watching your friends indulge in the things you can’t have. He learned to just say “Oh well” to temptation, and move on. If a child can show such awesome willpower, I guess I can say “Oh Well” and say no to snacks.

Share this:

Related

Published by BionicOldGuy

I am a Mechanical Engineer born in 1953, Ph. D, Stanford, 1980. I have been active in the mechanical CAE field for decades. I also have a lifelong interest in outdoor activities and fitness. I have had both hips replaced and a heart valve replacement due to a genetic condition. This blog chronicles my adventures in staying active despite these bumps in the road.

View all posts by BionicOldGuy

Throughout history, insurers have been pivotal in driving social change, enabling human progress, innovation, and prosperity. From seatbelts to vaccines and fire-retardant materials, insurers have fostered numerous innovations. Nowadays, they face a new monumental challenge: climate change. 2024 has been another record loss year for insurers driven by natural catastrophes linked to climate change. Insurers are hence seeking greener pastures. If done right, aiding businesses in their transformation to reduce greenhouse gas emissions becomes a positive for insurers. They can be facilitators of the transition to a carbon-neutral future by exerting influence across the wide variety of industries they finance.

There is an opportunity for insurers to safeguard their top-line and bottom-line while supporting customers on their net zero journeys. In Underwriting, that minimizes risk exposure and scope for regulatory fines by proactively responding to changes, and clients who effectively embark on the green transition are expected to bring higher sales in the mid to long term. In Investments, the case is even better understood: 93% of investors say that climate issues are most likely to affect the performance of investments over the next two to five years.Non-transitioning companies or those who start transitioning too late are in danger of losing an investment grade credit rating, while the outperformers – what we call ‘green stars’ are expected to benefit from green technologies shift in a Paris-agreement-aligned world scenario.

A new tool for profitable portfolio decarbonization

Insurers need to be able to translate their investee and clients’ emission reduction measures into financial implications for appropriate risk calculations, to decarbonize profitably on their own end.

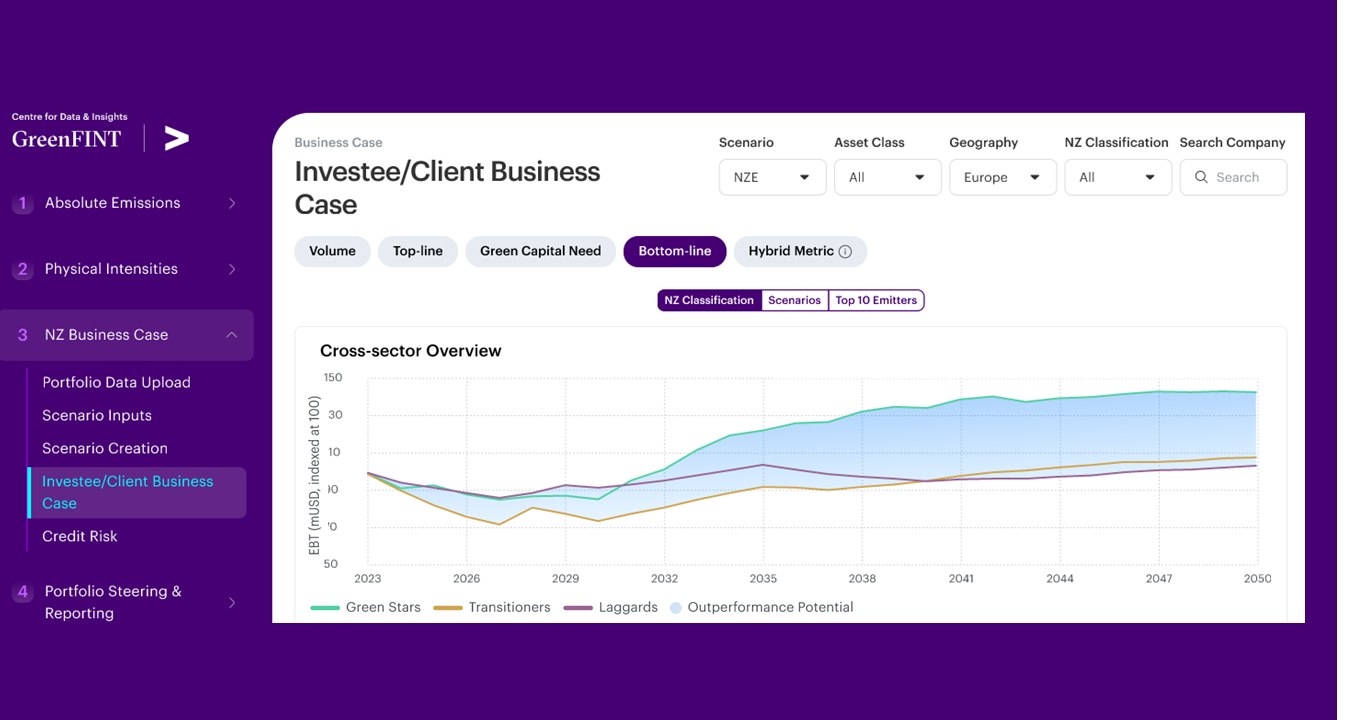

As we at Accenture are committed to fostering net zero business practices we have introduced the GreenFInT (Green Financial Institution Tool ), also known as the Profitable Portfolio Decarbonization Tool. Comparing sample client portfolio dynamics up until 2050 for high carbon intensive sectors, it shows ‘green stars’ might outperform ‘climate laggards’ by 30-40 percentage points. The true value of the tool lies in familiarizing insurance managers across investment, risk and pricing with setting assumptions for different world views, from a ‘hot world’ scenario to reaching the Paris alignment.

Allow me to delve into the tool in greater detail. The GreenFInT tool caters to both the emissions measurement and reporting use cases (e.g., ESRS E1 quantitative KPIs for CSRD) as well as to business value cases with regards to decarbonization. The tool applies climate scenarios (e.g., 1.5°C, 2.4°C) to portfolio companies’ technology mix, depending on their Net Zero pledges and transition plans. Differences in technology mix, pledges, and plans translate into divergent profitability curves via required capital investments and differences in operational costs.

‘Green stars’ win out in the long term

For illustration, an insurer’s ‘green star’ client from the power generation sector with a SBTi verified Net Zero target by 2040 has and will have a larger share in renewables than a client classified as ‘laggard’. With its proactive transition towards net zero, the ‘green star’ client has initial high capital costs to finance the build out of installed capacities from renewable energy sources to meet its milestones while electricity prices are relatively high – outlining a business opportunity for insurers as the client is in need of financing and insuring of the renewables built out. In comparison, a ‘laggard’ company had no and will not have capital investments beyond usual replacement and maintenance costs of its power plants. On the other hand, renewables have much lower operational cost compared to power generated from nuclear energy and natural gas. Thus, the ‘green star’ that has invested in renewables in a timely fashion will benefit from lower operational costs while the ‘laggard’ will have higher operational costs from traditional energy sources.

Let’s take an exemplary insurance portfolio with 40 large company clients from four high-intensity sectors, namely power generation, steel, real estate, and automotive, focused within Europe. In a 1.5°C scenario, the capital need for the net zero transition of these companies amounts to approximately 650bn USD 2023-2050 – according to the GreenFInT modelling. While in the mid-term up until 2030, the EBT margin of ‘laggards’ outperform ‘green stars’ by approximately 6 percentage points, in the long-term, 2023-2050, ‘green stars’ outperform ‘laggards’ by 30-40 percentage points (see graph below).

This forward-looking approach – leveraging scientific sector carbon budgets vs. traditional forecasts based on historical values – enables insurers to integrate long-term scenarios (up to 2050) into their current considerations. This is a most important step towards breaking the ‘tragedy of the horizon’. GreenFInT makes it possible to identify insurers’ investees and clients with trustworthy net zero commitments as the business case assessment can reveal who may not be able to afford their net zero commitments. Building a trusted relationship with these companies as insurer or investor today, is key for a profitable decarbonization. Insights gained through GreenFInT can be helpful to prioritize clients to engage with and a grounded conversation opener to better understand the clients’ transition plans.

Beyond a net zero business case analysis, GreenFInT also covers the accounting of Scope 3 Category 15 emissions in absolute terms and physical intensities as well as target setting and a ‘What-If’ capability, enabling insurers to simulate effects on their carbon footprint with adjustments to their portfolio.

The time to act is now

Insurance has consistently demonstrated resilience in the face of numerous challenges, and the current push towards decarbonization is no different. By embracing the transition to net zero, insurers can not only safeguard their profitability but also play a pivotal role in fostering a sustainable future. The integration of science-based sustainability targets into underwriting and investment practices will enable insurers to drive significant change across various industries. As regulatory pressures and public expectations continue to rise, insurers must act decisively to avoid the risks of inaction and greenwashing. The tools and strategies outlined provide a clear pathway for insurers to achieve profitable portfolio decarbonization, ensuring long-term growth and trust in a rapidly evolving landscape. The time to act is now, and the opportunities for those who lead the charge are immense. For further discussion on how to implement these strategies in your enterprise, please get in touch.

New Nomination Rules for Demat & Mutual Funds by SEBI allow up to 10 nominees from Sept 2025. Know key changes, forms, deadlines, and investor guidelines.

Investing is not just about growing wealth; it’s also about ensuring it passes smoothly to your loved ones after your lifetime. That’s where nomination comes in.

To simplify and safeguard the nomination process, SEBI has issued a new circular (dated February 16, 2025), with additional operational guidelines shared by KFintech. These new rules are crucial for all mutual fund and demat account holders, and certain changes will take effect from June 1, 2025, and September 1, 2025.

Let’s break this down in simple language with real-life examples.

SEBI’s New Nomination Rules for Demat & Mutual Funds 2025

What Is Nomination and Why Is It Important?

A nomination is a facility that allows you (the investor) to name someone who can claim your investments after your death. Without a nomination, your family may have to go through time-consuming legal procedures.

Example: Mr. Ramesh, a salaried professional, invested in mutual funds but didn’t nominate anyone. When he passed away unexpectedly, his wife struggled for months to get access to the funds. If Ramesh had nominated her, the process would’ve been much smoother.

What SEBI’s February 2025 Circular Says

No More Freeze for Not Nominating

Earlier, investors had a deadline to either nominate someone or opt-out, failing which their accounts could be frozen. That’s now gone. You can continue investing without fear of your account being frozen.

However, SEBI still advises you to nominate or explicitly opt out for your family’s protection.

What’s Changing from June 1 and September 1, 2025?

KFintech has issued key updates to the nomination process, especially for mutual fund folios. Here’s what’s new:

1. New Nomination Form Format – Effective June 1, 2025

Starting June 1, 2025, a new format of the nomination form must be used. If you’re submitting your nomination on or after June 1, make sure to use the updated form. The opt-out form remains the same. No changes there.

2. Number of Nominees You Can Add

Period

Max Nominees Allowed

Until August 31, 2025

Up to 3 nominees

From September 1, 2025

Up to 10 nominees

What this means: If you’ve been restricted to adding just 3 nominees, you’ll be happy to know that from September 1, you can nominate up to 10 individuals, giving you more flexibility to distribute your investments.

3. Mandatory Information for Each Nominee

To avoid processing delays or rejections (called NIGO – Not in Good Order), the following details are mandatory for each nominee:

Full Name

Relationship with the investor

Percentage of share

Address

Email ID

Mobile number

Any one of the following identity details:

PAN

Driving License Number

Last 4 digits of Aadhaar

Passport Number

If any of this is missing, your nomination will be rejected.

4. Date of Birth for Minor Nominees

If you’re nominating a minor, you must mention the Date of Birth (DOB) of the nominee. However, naming a guardian is optional, though it’s recommended for better clarity.

Example: Mrs. Seema nominates her 10-year-old son as one of the nominees. She must mention his date of birth, but she may choose whether or not to mention her brother as the guardian.

5. Witnesses for Thumb Impressions

If you sign the nomination form using a thumb impression (instead of a signature), you must include the:

Name, address, and signatures of two witnesses

This is done to ensure the legitimacy of the nomination.

6. Who Can Operate Your Account If You’re Incapacitated?

You can authorize any one of your registered nominees (except a minor) to operate your folio or demat account in case you become physically or mentally incapacitated.

You can give this mandate at any time, and it’s not restricted to just when you open your account.

This is a great new feature that helps in unfortunate medical conditions.

7. Mode of Signing the Nomination Form – Based on Holding Type

Mode of Holding

Who Can Sign the Form

Single / First Holder

Only first holder must sign

Joint Holding

All holders must sign

Either or Survivor / Anyone or Survivor

Any one holder can sign

Ensure your signature matches with your records, or else it may be rejected.

8. What Happens After the Investor’s Death?

If the investor passes away:

The nominees can either:

Continue as joint holders among themselves, OR

Open separate single folios/accounts in their own name.

If some nominees don’t claim their share, the unclaimed portion stays with:

AMC in case of mutual funds

Depository in case of demat accounts

9. No Limit on Nomination Updates

There’s no restriction on how many times you can add/change/remove nominees. You can update nominations as often as you want, and every time you do, the AMC or DP will give you an acknowledgment.

Real-Life Example to Understand Better

Case 1: Mr. Arvind holds a mutual fund folio in his name and wants to nominate his wife and two children equally. He submits the nomination in July 2025 using the new format, filling all mandatory details, including Aadhaar numbers.

Outcome: Nomination accepted and acknowledged. Upon his death, the fund house can quickly release the funds to the three nominees.

Case 2: Ms. Rekha submits a nomination form in September 2025 with 8 nominees, but misses entering the mobile number of two nominees.

Outcome: The nomination is marked as NIGO and rejected until full details are provided.

Why You Should Act Now

Avoid Legal Complications: Without nomination, your family may need to get legal heir certificates or go to court.

Peace of Mind: You know your investments are protected and will go to the right person.

Flexibility: You can nominate, update, or delete nominees anytime.

Summary Table

Feature

Details

New Nomination Format

From June 1, 2025

Max Nominees Allowed

3 (till Aug 31), 10 (from Sept 1)

Mandatory Nominee Info

Name, % share, contact, identity number

Minor Nominee

DOB mandatory, guardian optional

Incapacitation Mandate

Can authorize any major nominee

Signing Rules

Based on folio holding (Single, Joint, Either)

Witnesses

Needed for thumb impressions

Update Nomination

Unlimited times, with acknowledgment

For Unbiased Advice Subscribe To Our Fixed Fee Only Financial Planning Service

Happy Summer 2024 my friends! After blogging this many years, you all should know that summer is my favorite time of the year.

Things are busy as the studio which is so awesome, summer training is gearing up for my athletes, and Corey and I are doing our annual visit to our family in PA before it all gets busy.

With that being said, not only is summer time my favorite, but summer clothes are my favorite. When I can finally swap from leggings to shorts, it’s low-key life changing.

My friends at adidas make it very easy to keep up my *life-changing* apparel and I wanted to share those with you today!

Womens Sweatshirt Matching Set – I’ve been looking into a cute matching set for so long and these floral details on this Floral Graphic Sweatshirt sold me. How adorable is this set!? Comfy and cute. The shorts that match are also super comfy.

Essentials Rib Tank Top – I’ve been eyeing this one up for a while on the website and finally got one to try. The material is fitted yet super stretchy and would be cute for working out or to wear to dinner.

Running Waist Belt – I recently just ran a 5k with some of our members from the studio and I realized I had no way to hold my phone and listen to music. Safe to say, I was bummed! I’d like to get back into running and thought this belt looked perfect to hold my phone so I can jam out.

Women’s Shorts – ok ok let me tell you about these shorts. At first I wasn’t sure because they weren’t as “high waisted” as I normally go for BUT they have quickly become the shorts I’m grabbing for. They have built in shorts that don’t squeeze too much around the thighs and actually hit high on my hips for being 5’8!

Adilette Aqua Slides – you really can’t go wrong with a pair of slides in the summer. I’ve been a soccer player my whole life so having easy slip on sandals has always been my vibe. I also love a neutral moment so these cream colored ones are adorable.

Tech Bucket Hat – bringing it back to the 90’s baby! My friend had a bucket hat on the other day at the beach and I was like, that is genius actually. I’m usually in a hat but now I’m adding a bucket hat to the fam.

Womens Running Shoes – I fell in love with a pair of shoes last year and I was trying to find a pair that was similar and I will say these are pretty dang close! They are supportive but stylish and comfortable for me to wear while teaching classes all day.

If you try out any of these summer picks, let me know!

Nvidia Corp.NVDA unveiled its robotics strategy during its first-quarter 2025 earnings call on Wednesday, positioning the chipmaker for what executives called the emerging “era of robotics” as artificial intelligence expands beyond data centers into physical applications.

What Happened: “The era of robotics is here. Billions of robots, hundreds of millions of autonomous vehicles, and hundreds of thousands of robotic factories and warehouses will be developed,” Chief Financial Officer Colette Kress told analysts during the earnings call.

The Santa Clara-based company reported record first-quarter revenue of $44.1 billion, up 69% year-over-year, driven by continued demand for its AI chips. Data center revenue reached $39 billion, representing 73% annual growth as customers deployed NVIDIA’s Blackwell architecture for reasoning AI applications.

NVIDIA introduced Isaac Groot, described as “the world’s first open, fully customizable foundation model for humanoid robots, enabling generalized reasoning and skill development.” The platform aims to train robots using synthetic data generated through NVIDIA’s Omniverse simulation environment.

Why It Matters: Leading robotics companies, including Agility Robotics, Boston Dynamics, and Figure AI are already integrating NVIDIA’s technologies. GE HealthCare Technologies Inc.GEHC is using the new NVIDIA Isaac platform for robotic imaging and surgery systems development.

CEO Jensen Huang emphasized the strategic importance of robotics during the call, noting that future manufacturing plants will require “AI factories” to operate robotic systems.

Price Action: Nvidia Corp.’s stock closed at $134.81 on Wednesday, down 0.51% for the day. In after-hours trading, the stock rose sharply by 4.89% to $141.40. Year to date, Nvidia shares are down 2.53%.

NVDA stock enjoys strong momentum, growth, and quality, but performs poorly on valuation metrics, according to Benzinga Edge Stock Rankings. The stock shows a positive price trend across the short to long term. Here is the full stock breakdown.

Read Next:

Disclaimer: This content was partially produced with the help of AI tools and was reviewed and published by Benzinga editors.

May is National Foster Care Awareness Month — a time dedicated to recognizing the resilience of youth in foster care and the critical role we all play in supporting their journeys. For many of these young people, stepping onto a college campus is not just the start of a new chapter — it’s the start of a new life. That’s why Move-in Day Mafia exists: to ensure foster youth aren’t just seen during their college transition but truly supported.

New Rooms, New Beginnings

For many, college is a time of firsts — first taste of independence, first real shot at shaping a future, and first steps into a world of possibility. It’s a season of discovery, excitement, and the thrill of the unknown. For many first-generation college students, these emotions run even deeper. But for young people emerging from the foster care system, the experience is often marked by an entirely different reality: survival.

Imagine stepping onto a college campus carrying every belonging you own in a single backpack. No parents to help set up your dorm. No family to send you care packages. No blueprint for how to navigate this brand-new world. Just hope — and the sheer will to succeed against the odds.

“Only 3–4% of youth who age out of foster care ever earn a college degree — Move-in Day Mafia is determined to change that.”

The hurdles facing foster youth are staggering. According to The National Foster Youth Institute, only about 3–4% of youth who age out of foster care ever earn a college degree. Many never even get the chance to enroll. The reasons are as heartbreaking as they are complex: unstable housing, lack of financial resources, emotional trauma, and an absence of reliable adult support. Even after overcoming these obstacles to reach a university, many foster youth find themselves isolated, ill-prepared, and overwhelmed.

That’s where Move-in Day Mafia comes in.

Cisco employee, Jenina John-Guobadia with her husband and MIDM crew.

Move-in Day Mafia exists with a powerful, clear mission: to ensure that students from the foster care system are not forgotten as they step into college life. Their work begins with the basics — turning bare dorm rooms into safe, welcoming homes. A simple comfort like a real bed, a desk stocked with supplies, or a closet filled with essentials can mean the difference between feeling like an outsider and believing you belong.

For some of these students, a dorm room is the first stable place they’ve ever called their own. It’s their sanctuary, their launchpad, and their first real taste of what it means to dream without limits. And yet, without support, even something as basic as a furnished room can seem out of reach.

More than a Makeover

Through its involvement with Move-in Day Mafia, Cisco is helping bridge that gap. Beyond providing financial support, Cisco has mobilized its employees and resources to directly uplift these students — helping to furnish dorm rooms, supply technology needs, and ensure that no student walks into college empty-handed.

An inspiring example of this commitment is Cisco’s ongoing support for the “Adopt a Scholar” program. Through this initiative, Cisconians come together to purchase care package items for students preparing to begin their college journeys. These care packages are filled with essentials like bedding, toiletries, school supplies and even personal notes of encouragement. It’s a collective effort that brings the Cisco community together in support of new beginnings, sending a powerful message to each student: you are seen, you are valued, and you are supported.

Cisco Volunteers with Move-in Day Mafia Founder, TeeJ Mercer

Together, Move-in Day Mafia and Cisco are making sure that these young people — who have already faced more adversity than many do in a lifetime — have a foundation to build on. They’re sending a message that someone believes in their potential, that they are not alone, and that their dreams are valid.

For every pillow placed on a bed, every lamp set up on a desk, every laptop connected to Wi-Fi represents a new beginning. A fresh start. A way forward. Because every child deserves the chance to not just survive college — but to thrive.

, GE Aerospace (NYSE:GE)")