College students have a lot on their plate already, including the need to study to get good grades, participating in any number of on-campus activities and potentially working part-time to have some spending money.

That said, college students should also focus on their financial future, including steps they can take to build credit before they enter the workforce.

After all, having a credit history and a good credit score can mean being able to rent an apartment, finance a car or take out a loan, whereas having no credit at all can mean sitting on the sidelines until the situation changes.

Fortunately, there are all kinds of ways for young adults to build credit while they’re still in school. Some strategies require a little work on their part, but many are hands-off tasks that you only have to do once.

Teach Them Credit-Building Basics

Make sure your student knows the basic cornerstones of credit building, including the factors that are used to determine credit scores. While factors like new credit, length of credit history and credit mix will play a role in their credit later on, the two most important issues for credit newcomers to focus on include payment history and credit utilization.

Payment history makes up 35% of FICO scores and credit utilization ratio makes up 30% of scores.

Generally speaking, college students and everyone else can score well in these categories by making all bill payments on time and keeping debt levels low. How low?

Most experts recommend keeping credit utilization below 30% at a maximum and below 10% for the best possible results. This means trying to owe less than $300 for every $1,000 in available credit limits at a maximum, but preferably less than $100 for every $1,000 in credit limits.

Add Your Child as an Authorized User

One step you can personally take to help a child build credit is adding them to your credit card account as an authorized user. This means they will get a credit card in their name and access to your spending limit, but you are legally responsible for any charges they make. Obviously, this move works best when you have excellent credit and a strong history of on-time payments and you plan to continue using credit responsibly .

While this step can be risky if you’re worried your college student will use their card to overspend, you don’t actually have to give them their physical authorized user credit card.

In fact, they can get credit for your on-time payments whether they have access to a card or not. If you do decide to give them their credit card, you can do so with the agreement they can only use it for emergency expenses.

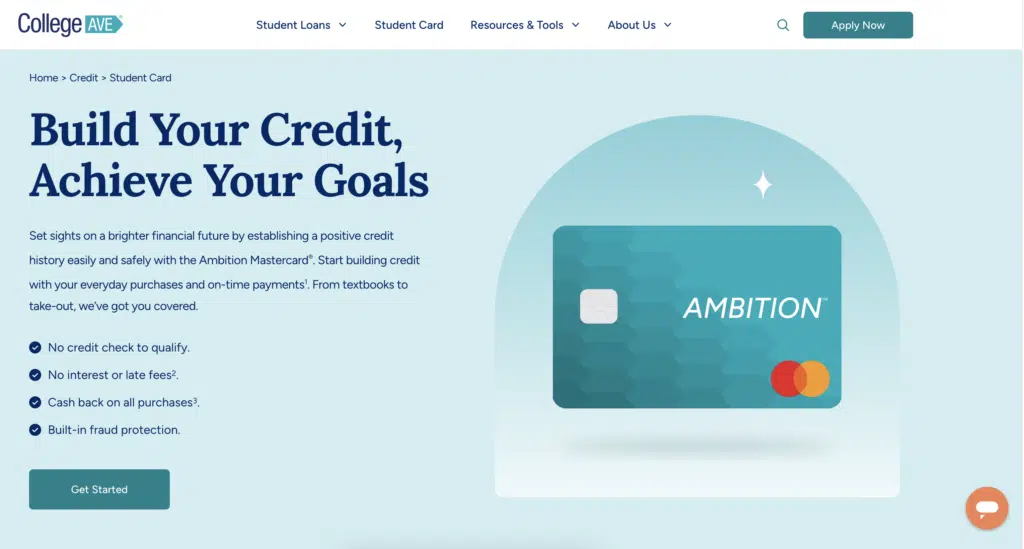

Encourage Them to Get a Secured Credit Card

Your child can build credit faster if they apply for a credit card and get approved for one on their own, yet this can be difficult for students who have no credit history. That said, secured credit cards require a refundable cash deposit as collateral are very easy to get approved for.

Some secured credit cards like the Ambition Card by College Ave even offer cash back1 on every purchase and don’t charge interest2. If your child opts to start building credit with a secured credit card, make sure they understand the best ways to build credit quickly — keeping credit utilization low and paying bills early or on time each month.

Opt for a Student Credit Card Instead

While secured credit cards are a good option for students with little to no credit get started on their journey to good credit, there are also credit cards specifically designed for college students. Student credit cards are unsecured cards, meaning they don’t require an upfront cash deposit as collateral, but charge interest on any purchases not paid in full each month.

Many student credit cards offer rewards for spending with no annual fee required as well, although these cards do tend to come with a high APR. The key to getting the most out of a student credit card is having your dependent use it only for purchases they can afford and paying off the balance in its entirety each billing cycle. After all, sky high interest rates don’t really matter when you never carry a balance from one month to the next.

Student Credit Cards…

“One of the safest ways for college student to build their credit by learning valuable money skills.”

Help Your Child Get Credit for Other Bill Payments

While secured cards and student credit cards help young adults build credit with each bill payment they make, other payments they’re making can also help.

In fact, using an app like Experian Boost can help them get credit for utility bills they’re paying, subscriptions they pay for and even rent payments they’re making. This app is also free to use, and you only have to set up most bill payments in the app once to have them reported to the credit bureaus.

There are also rent-specific apps and tools students can use to get credit for rent payments, although they come with fees. Examples include websites like Rental Kharma and RentReporters.

Make Interest-Only Payments On Student Loans

The Fair Isaac Corporation (FICO) also notes that students can start building credit with their student loans during school, even if they’re not officially required to make payments until six months after graduation with federal student loans.

Their advice is to make interest-only payments on federal student loans along with payments on any private student loans they have during college in order to start having those payments reported to the credit bureaus as soon as possible.

“Making interest-only payments as a student will not only positively affect your credit history but will also keep the interest from capitalizing and adding to your student loan balance,” the agency writes.

Of course, interest capitalization on loans would only be an issue with private student loans and Federal Direct Unsubsidized Loans since the U.S. Department of Education pays the interest on Direct Subsidized Loans while you’re in school at least half-time, for six months after you graduate and during periods of deferment.

The Bottom Line

College students don’t have to wait until they’re done with school to start building credit for the future, and it makes sense to start building positive credit habits early on regardless. Tools like a credit card can help students on their way, whether they opt for a secured credit card or a student card. Other steps like using credit-building apps can also help, and with little effort on the student’s part or on yours.

Either way, the best time to start building credit was a few years ago, and the second best time is now. You can give your student a leg up on the future by helping them build credit so it’s there when they need it.

20% APR. Account is subject to a monthly account fee of $2, account fee is waived for the initial six-monthly billing cycles.

College Ave is not a bank. Banking services provided by, and the College Ave Mastercard Charge Card is issued by Evolve Bank & Trust, Member FDIC pursuant to a license from Mastercard International Incorporated. Mastercard and the Mastercard Brand Mark are registered trademarks of Mastercard International Incorporated.

When I suggest adding impact training to the fitness routines of my over-50 clients, I often get wide eyes and raised eyebrows. They picture explosive box jumps or high-impact plyometrics — and understandably, that sounds intimidating, especially for someone who’s never tried it, hasn’t done it in decades, or is navigating osteoporosis or osteopenia.

But here’s the thing: impact training doesn’t have to mean leaping tall boxes in a single bound. In fact, it can be surprisingly simple — and a lot closer to the ground — yet still build stronger bones.

What Is Impact Training, Really?

Impact refers to any two forces meeting one another. In impact training, those two forces are your body and the ground.

We often think of bones like those lifeless plastic skeletons from anatomy class — static and inert. But bones are incredibly alive, richly supplied with blood vessels, and highly responsive to the stresses we place on them.

For your bones to pay attention, the impact needs to exceed what they experience during normal daily activity. Things like walking, stairs, yoga, and Pilates are “ho-hum” for your bones. Even running and jogging can be boring [yawn] if you do them regularly!

Impact training sends stronger signals that tell your bones to ramp up activity and lay down new bone cells. And new bone cells = stronger, denser bones.

How Impact Training Improves Bone Health

Throughout life, bones go through a regular remodeling process: old and damaged bone cells are broken down and replaced by new, healthy ones.

During youth, we build bone faster than we break it down — until we reach peak bone mass, which for most women occurs between ages 25–30.

But women can lose up to 20% of their bone mass during the menopause transition — usually from one year before their final period through five or six years after.

Osteoporosis Is a Childhood Disease?

Dr. Belinda Beck refers to osteoporosis as a “childhood disease.” Without enough bone-building physical activity as children and adolescents, we miss out on reaching our full bone mass potential. That leaves us more vulnerable to low bone density later in life.

SIDEBAR: Dr. Belinda Beck ran the landmark LIFTMOR trial, which found that high-intensity resistance and impact training significantly improved bone density in postmenopausal women — and it was safe, even for those with low or very low bone mass.

How to Start Impact Training Safely

When starting any new type of exercise, begin small. See how your body responds, and progress gradually.

Research shows that bones respond best to small doses of impact spread throughout the day.

Shoes or No Shoes?

I’m often asked whether to wear shoes for impact training. My answer? It depends.

If you’re used to walking around barefoot, you might feel fine starting without shoes.

If you always wear shoes, you’ll likely feel more supported wearing them.

The more intense the movement, the more helpful shoes become — especially for to cushion and protect your feet during training.

One note: very cushy sneakers can absorb (a.k.a. reduce) impact, which might help beginners ease into this kind of training more comfortably.

Beginner-Friendly Impact Moves (In Order of Difficulty)

Start with just a few reps, 2–3 times a day. Work up to 10 impacts per session, aiming for 50 total per day. You can sneak these in while your coffee brews or during commercial breaks! (Bonus points for multi-directional hops and jumps.)

Impact training isn’t just for elite athletes — it’s for anyone who wants to age with strength, confidence, and vitality.

Just a few hops or heel drops a day can help:

No need to jump into the deep end. Start small, stay consistent, and remember: every little impact counts.

Your bones — and your future self — will thank you.

If you need more information on navigating exercise for bone health, or have been diagnosed with osteoporosis or osteopenia, I’m here to help!—Karin

P.S. Got Young Ones in Your Life? Help them build their “bone bank” early. Encourage them to jump, skip, hop, climb — and better yet, move with them. Bone health is a lifelong investment, and it’s never too early (or too late) to start.

References:

The Role of High-intensity and High-impact Exercises in Improving Bone Health in Postmenopausal Women: A Systematic Review., Manaye S, et. al, 2023

Mechanobiology of Bone Tissue and Bone Cells, Astrid Liedert, et. al, 2005

Bone and the perimenopause, Lo JC, et. al, 2011

The BPAQ: A bone-specific physical activity assessment instrument, Weeks B., Beck, B., 2008

Skeletal site-specific effects of jump training on bone mineral density in adults: a systematic review and meta-analysis, Florence GE, et. al, 2023

The effect of exercise intensity on bone in postmenopausal women (part 2): A meta-analysis. Kistler-Fischbacher M, et. al, 2020

The Mechanosensory Role of Osteocytes and Implications for Bone Health and Disease States. Choi JUA, et. al, 2022

Efficiency of Jumping Exercise in Improving Bone Mineral Density Among Premenopausal Women: A Meta-Analysis, Zhao R., et. al, 2014

Opinions expressed by Entrepreneur contributors are their own.

In the early 1900s, as the automotive revolution reshaped industries, blacksmiths and carriage-makers struggled to adapt. More than a century later, we face a similar inflection point with AI. Just as horse-drawn carriages gave way to automobiles, entire industries are being redefined by algorithms today.

The question isn’t whether your company will adopt AI, but how. And the answer hinges on one critical factor: culture.

Building an AI-driven culture isn’t always about buying tools or hiring machine learning scientists. It’s about fostering a mindset where experimentation, learning and human-AI collaboration are core to your company’s DNA. Here’s how to start:

Model curiosity to dispel fear:

Leadership must champion AI, but grassroots innovation is what embeds it into real workflows. At CodeSignal, our engineering team doesn’t just use AI — they build with it. From leveraging GitHub Copilot for complex refactoring to fine-tuning custom LLM agents for internal tools, AI is part of their daily toolkit. And it’s not just engineering. Our marketers, for instance, prototype campaign ideas in Claude and validate messaging variations with Gemini.

The key? Leaders must model curiosity. Share your own AI experiments — and failures — with your team. CodeSignal has a Slack channel dedicated to experimentation with LLMs, where team members share how they’ve been using AI and what they’re learning (“productivity hacks” are a team favorite).

I have been studying AI technology and building AI-native products for over a decade, but this doesn’t stop me from continuing to learn. I regularly share my learnings, from using the latest LLM models for everything from code writing to email writing to image generation, and debate with my colleagues on how different models perform on complex math challenges.

The point of me doing this is to set the example that incorporating AI into your daily workflow doesn’t have to be intimidating, and in fact it can be quite enjoyable. It also reinforces that we’re all learning this new technology and figuring out how best to use it to do our work together.

Provide access to the right AI tools:

Today, tools like ChatGPT and Midjourney are free, yet many companies still gatekeep access. That’s a big mistake. We give every team member a ChatGPT Teams subscription, with the expectation that they’ll play around with it and even create their own GPTs to augment their workflow. In the past year, our employees have created over 50 custom GPTs that help them draft sales emails, gather market insights, extract data, answer HR questions and more.

Make AI literacy a core expectation — then build on it:

Giving people access to AI tools is necessary, but it’s just the first step. To create a meaningful impact, leaders must pair access to tools with training.

CodeSignal does this by asking every team member to complete AI literacy training, where they build skills in using and interacting with LLMs with hands-on practice. Our team recently finished a “spring training” in generative AI literacy, where everyone at the company (even me!) completed a series of experiential learning courses online and shared our learnings, questions and ah-ha moments in a Slack channel. We boosted motivation for completing the training by setting up a goal of 95% participation — rewarded by cool new swag when we met the goal.

Next, we’re building on this foundation of AI literacy by running an AI hackathon at our next in-person meetup. Here, team members will break into teams based on how they use AI and their depth of knowledge. Some teams will explore using LLMs to draft creative campaigns and set project timelines, for example, while others will be building custom GPTs to automate actual parts of their job. The machine learning experts on our team, meanwhile, will be working on building innovative new AI applications from the ground up.

The goal here is to set the expectation that everyone uses AI, yes — but more than that, to give team members ownership of what they do with it and the freedom to choose which parts of their job can best be complemented by AI.

For some organizations and teams, adopting AI will be uncomfortable at first. AI tools raise a range of new technical, regulatory and ethical questions. Many employees fear that AI will displace them from their jobs. That discomfort is real — and it deserves our attention.

As leaders, our responsibility is to guide our teams through uncertainty with integrity and transparency by showing how embracing AI can help them become even more impactful in their jobs. I do this by modeling AI use in my everyday work and openly sharing my learnings with my team. This gives team members permission to experiment on their own and helps move them from a mindset of fear to curiosity about how AI can be a partner to them in their jobs.

To return to the analogy of the automotive revolution: We’re teaching our carriage-makers how to build self-driving cars.

If you’re a business leader, ask yourself: Am I modeling what it looks like to learn and take risks? Am I giving my team the tools and training they need to build AI literacy? Am I fostering a culture of exploration and experimentation on my team?

The AI revolution is already here, and the future isn’t going to wait for companies to catch up. Neither should we.

In the early 1900s, as the automotive revolution reshaped industries, blacksmiths and carriage-makers struggled to adapt. More than a century later, we face a similar inflection point with AI. Just as horse-drawn carriages gave way to automobiles, entire industries are being redefined by algorithms today.

The question isn’t whether your company will adopt AI, but how. And the answer hinges on one critical factor: culture.

Your body knows how to heal. Think about it — if a poor diet and lifestyle can contribute to an unhealthy body, it stands to reason that a nutrient-rich diet and lifestyle can conversely contribute to a healthy body. That’s not too hard to figure out.

What is hard to figure out is what is bad for your health and what is good. Are statins good or are they bad? Should you take them? Are there alternatives? If so, what are they?

There are many conflicting stories because cholesterol metabolism is complex, making it a perpetually confusing topic. You deserve to understand your health before blindly accepting treatments.

I get a lot of questions about cholesterol, statin drugs, and how to lower cholesterol without taking statins. The good news is that certain plants and lifestyles have been scientifically proven to lower cholesterol. So, let’s break it all down. In this post, I cover:

What is cholesterol, and why do we need it?

Triglycerides and their relationship to cholesterol.

How triglycerides and cholesterol interact.

The Pareto Principle, cholesterol, and statins.

Herbs and plants with evidence for cholesterol-lowering effects.

Key metabolic biomarkers.

With the proper knowledge and approach, you have the power to control your health.

What Is Cholesterol?

Cholesterol is a fatty, waxy substance found in every cell in the body. Roughly 20% comes from dietary sources, while 80% is primarily manufactured in the liver and other cells. Cholesterol metabolism studies show that this ratio can vary slightly depending on individual factors like genetics, diet, and lifestyle.

Excess sugar, particularly artificial sugars, refined carbohydrates, and genetic errors of liver metabolism, are mainly to blame for high cholesterol. Plant fibers can lower cholesterol, so a diet high in fruits and vegetables and whole grains with minimal fats helps maintain normal cholesterol levels.

• Types of cholesterol:

1. Low-density lipoprotein, LDL, is often called bad cholesterol because high levels are theorized to build plaque in the arteries.

2. High-density lipoprotein, HDL, is called the good cholesterol because it helps to remove excess cholesterol from the bloodstream and returns it to the liver for disposal.

3. Very low-density lipoprotein, VLDL, mainly carries triglycerides in the blood and is less commonly measured.

• Why do we need cholesterol? Cholesterol is present in every cell of the human body and is essential for cellular metabolism.

• Cholesterol is essential for several biological functions:1

◦Cell membrane structure — Cholesterol is a key component of cell membranes, providing stability.

◦Hormone production — The building block for steroid hormones, including sex hormones (estrogen, testosterone), cortisol, and aldosterone.

◦Vitamin D synthesis — When the skin is exposed to sunlight, the body uses cholesterol to make vitamin D.

◦Bile acid production — Cholesterol is converted into bile acids in the liver, which help digest fats.

• Cholesterol and brain health:

◦Myelin sheath formation — Cholesterol is a major component of myelin, the protective sheath around nerve fibers that speeds up electrical signaling.

◦Neurotransmitter function — It is involved in the communication between neurons, supporting the function of neurotransmitters like dopamine and serotonin.

◦Cell signaling — Cholesterol is crucial for forming “lipid rafts,” specialized areas in cell membranes that facilitate cell signaling in the brain.

◦Learning and memory — Proper cholesterol metabolism in the brain is necessary for synaptic plasticity, learning, and memory.

Triglycerides and Their Relationship to Cholesterol

Triglycerides, another type of fat (lipid) in the blood, come from foods and are synthesized in the liver. Triglycerides also come from extra calories your body does not need right away.

Excess calories are converted to triglycerides and stored as fat in the body for later use. While cholesterol is used for structural and hormonal functions, triglycerides serve primarily as an energy source:

• Energy storage — Excess calories from food are converted into triglycerides and stored in fat cells for later use.

• Transport — Triglycerides circulate in the blood within lipoproteins, especially very-low-density lipoproteins (VLDL), which also carry some cholesterol.

How Triglycerides and Cholesterol Interact

• Both are transported in the bloodstream via lipoproteins (VLDL, LDL, HDL).

• VLDL particles mainly carry triglycerides but also transport cholesterol. As triglycerides are removed from VLDL, the particles become LDL, which is richer in cholesterol.

• HDL particles help remove excess cholesterol from tissues and return it to the liver for disposal.

So while cholesterol is used for building cell walls, hormone production, and other structural and metabolic functions, triglycerides are used primarily for energy supply and storage.

In a blood test, the total cholesterol level includes LDL, HDL, triglycerides, and sometimes VLDL, and means very little as a combined total. High triglycerides are more concerning because people with high triglyceride levels have an 80% higher risk of having a heart attack compared to people with normal triglyceride levels.2

Inflammation, fibrinogen, triglycerides, homocysteine, belly fat, triglyceride to HDL ratios, and high glycemic levels are the underlying drivers of heart disease.3

“Emerging science is showing that cholesterol levels are a poor predictor of heart disease and that standard prescriptions for lowering it, such as ineffective low-fat/high-carb diets and serious, side-effect-causing statin drugs, obscure the real causes of heart disease.”

~ The Great Cholesterol Myth

The Pareto Principle and Cholesterol

The Pareto Principle states that 80% of outcomes often stem from just 20% of causes, also known as the 80/20 rule. While commonly used in business, this principle can be metaphorically applied to biology and health, especially when identifying the key drivers behind complex issues.

As I mentioned, about 80% of the body’s cholesterol is made in the liver, while only 20% comes directly from the diet. Statins target this liver production by blocking the enzyme HMG-CoA reductase, which seems logical on the surface. But this approach overlooks why the liver is overproducing cholesterol in the first place — it treats the symptom, not the cause.

In truth, suppressing that 80% of cholesterol production without addressing the underlying 20% of triggers of metabolic disorders, such as insulin resistance, chronic inflammation, stress, and hormonal imbalances, can be counterproductive.

Even though dietary cholesterol accounts for just 20%, certain foods (like excess sugar, refined carbs, trans fats, and high-fructose corn syrup) can prompt the liver to increase its cholesterol output. A small subset of poor dietary choices may be responsible for most of the problem — a textbook 80/20 scenario.

For many people, small, focused lifestyle changes — such as eliminating processed foods, walking regularly, or improving sleep — can lead to significant improvements in cholesterol levels. Thus, 20% of your effort may yield 80% of the results.

Herbs and Plants with Evidence for Cholesterol-Lowering Effects

Anna McIntyre writes in “The Complete Herbal Tutor”:4

• Antioxidant herbs protect arteries, inhibit the formation of atherosclerotic plaque, lower cholesterol, and help prevent cardiovascular disease.

• Useful herbs include hawthorn, cayenne, amalaki, guggulu, bilberry, elderberry, ginger, turmeric, evening primrose, Chinese Angelica, and licorice.

• Shiitake and reishi mushrooms and oats contain beta-glucans, which help lower cholesterol.

• A clove of garlic a day can substantially lower cholesterol levels.

• Red clover reduces its absorption.

• Artichoke leaves help lower cholesterol by helping the liver‘s metabolism of cholesterol.

Some of these herbs and plants studied for their potential to lower cholesterol levels are listed below in more detail. They are the most researched options, with scientific evidence and study findings cited here.5,6,7,8

• Red yeast rice (Monascus purpureus)

◦Red yeast rice contains monacolin K, a compound chemically identical to the statin drug lovastatin, with all the risks and side effects of taking a statin.9

◦Multiple randomized clinical trials and systematic reviews have shown that red yeast rice can reduce total cholesterol and LDL cholesterol by 10% to 33%.

◦It is considered one of the most effective natural products for lowering cholesterol, but quality and safety concerns exist due to variability in monacolin K content and potential contamination with citrinin, a nephrotoxin (kidney-damaging substance).

• Plant sterols and stanols

◦Found naturally in plant-based foods like fruits, vegetables, nuts, oils, seeds, and grains.

◦A 2022 network meta-analysis found that plant sterol supplementation leads to modest LDL and total cholesterol reductions.

◦They work by blocking cholesterol absorption in the small intestine.

• Bergamot (Citrus bergamia)

◦Bergamot extract and its polyphenols have shown promising lipid-lowering effects.

◦A 2022 systematic review and meta-analysis found significant decreases in total cholesterol, LDL cholesterol, and triglycerides, and an increase in HDL cholesterol. However, a small number of studies limit the evidence.

• Artichoke (Cynara scolymus)

◦Randomized trials have shown reductions in total cholesterol by up to 18.5% compared to placebo.

◦The evidence base is limited but promising, with good safety profiles reported in studies.

• Fenugreek (Trigonella foenum-graecum)

◦Several trials, mainly from India, have shown reductions in total cholesterol ranging from 15% to 33%.

◦Some studies also found reductions in LDL cholesterol, though methodological quality varies.

• Guggul (Commiphora mukul)

◦Some randomized trials have reported 10% to 27% reductions in total cholesterol.

◦Although results have been inconsistent, and quality concerns exist, it remains one of the more extensively studied herbal options.

• Garlic (Allium sativum)

◦Ancient history and a wealth of modern research support the use of garlic. More than 3,000 scientific papers cover its chemistry, pharmacology, and clinical uses.10

◦The therapeutic uses of garlic are extensive, but those specific to the cardiovascular system include reducing elevated cholesterol, preventing atherosclerosis and hypertension, treating poor circulation to the legs, and improving overall blood flow through antiplatelet actions.

• Red clover (Trifolium pratense)

◦Systematic reviews have found significant reductions in total cholesterol and increases in HDL cholesterol in postmenopausal women, but effects on LDL cholesterol are inconsistent.

• Green tea (Camellia sinensis)

◦An American Journal of Clinical Nutrition meta-analysis suggests that green tea significantly reduces total cholesterol, including LDL or “bad” cholesterol, to 2.19 mg/dL in the blood. However, green tea didn’t affect HDL, or “good” cholesterol.11

Biomarkers and Blood Work

When examining bloodwork to evaluate cardiac risk and metabolic health, cholesterol alone is insufficient. These parameters and other risk factors, such as diabetes, cardiovascular issues, and liver function, must all be considered.

High LDL cholesterol was once thought to contribute to plaque buildup in the arteries, which could lead to the plaque becoming dislodged at some point, leading to a heart attack or stroke. Newer schools of thought don’t point to LDL as causing plaque buildup in the arteries but rather to chronic inflammation as being the cause.12

The newer cardiovascular assessment blood tests measure a specific protein called Apolipoprotein B (ApoB) within the LDL, which directly counts the number of atherogenic (plaque-producing) particles in the blood.

If ApoB is not measured, C-reactive protein (CRP) may be measured. CRP measures overall inflammation in the body and screens for cardiovascular risk. That’s important because many chronic diseases result from chronic inflammation. Metabolic biomarkers are key indicators of overall cellular health and disease risk.

The specific thresholds depend on your risk factors, and each lab has its parameters, but for reference, these are the normal ranges from LabCorp:

• LDL

◦Optimal — <100 mg/dL

◦Near-optimal — 100–129 mg/dL

◦Borderline high — 130–159 mg/dL

◦High — 160–189 mg/dL

◦Very high — ≥190 mg/dL

• HDL Cholesterol

◦Optimal — >39 mg/dL

• VLDL Cholesterol Cal

◦Optimal — 5–40 mg/dL

• Triglycerides

◦Optimal — 0–149 mg/dL

• Apolipoprotein B (ApoB)

◦Optimal — <130 mg/dL.

• C-reactive protein (CRP)

◦< 1.0 mg/dL or 10.0 mg/L

Relationship of Total Cholesterol to HDL

“Neither type of cholesterol is inherently bad or good. Both are necessary for good health. They need to be balanced in the body. Divide your total cholesterol by your HDL cholesterol. If the resulting number is 4 or less, you are at low risk, regardless what your total cholesterol number is. The ratio of total cholesterol to HDL is a much better predictor of risk than simply your total cholesterol number.13”

In her book “Good Energy,” Casey Means, M.D., writes about the five specific biomarkers to evaluate for overall metabolic health.14 Research shows that exercise improves all five of the following basic biomarkers of metabolism:

• Glucose levels above 100 mg/dL — Twelve-week exercise programs of either high-intensity running (40 minutes per week) or low-intensity running (150 minutes per week) both brought participants’ blood sugar from the prediabetic range (100 mg/dL or greater) to the nondiabetic range.

• HDL cholesterol less than 40 mg/dL — A 2019 review of the literature showed that exercise increased HDL cholesterol, “with exercise volume, rather than intensity, having a greater influence.” Meanwhile, “raising HDL levels pharmacologically has not shown convincing clinical benefits.”

• Triglycerides above 150 mg/dL — Numerous studies have demonstrated that physical activity effectively lowers triglyceride levels. In a 2019 study, an eight-week moderate aerobic exercise program significantly reduced triglyceride levels in participants. Furthermore, even a single session of intense aerobic exercise has been found to decrease triglyceride levels the following day.

This positive effect could be due to the increased activity of hepatic lipase in the liver, an enzyme that facilitates the absorption of triglyceride from the bloodstream.

• Blood pressure of 130/85 mm Hg or higher — Research has shown the effects of exercise among populations with high blood pressure were similar to the effects of commonly used medications.

(Note: blood pressure parameters considered high used to be above 140/90 mm Hg. This study15 changed that. The top number (systolic) measures artery pressure during a heartbeat; the bottom (diastolic) measures it between beats. Both are important but know systolic pressure can spike with stress. Blood pressure should be measured in both arms over time — not based on a single reading — especially before starting medication.)

• A waistline of more than 35 inches for women and 40 inches for men — Not surprisingly, regular exercise can help decrease obesity by increasing energy expenditure and promoting weight loss.

Research shows a clear inverse relationship between the amount of movement people do each week and the size of their waistline: more movement, smaller waist circumference. What’s more, lower activity (fewer than 5,100 steps per day) yields a 2.5 times higher risk of central obesity than higher activity (more than 8,985 steps per day).

Key Takeaways

With the proper knowledge and approach, you have the power to control your health.

• Reduce sugar, HFCS, refined carbohydrates, and other highly processed foods.

• Eat a diet high in vegetables, whole grains, especially oats, beans, legumes, pulses (such as beans, lentils, chickpeas), good fats, and oily fish.

• Take regular aerobic exercise and daily walking.

• There is no “one size fits all” diet for heart health. Eat whole foods without preservatives and additives, and concentrate on plant foods.

One important caveat:

• Statins lower LDL cholesterol quickly by blocking an enzyme (HMG-CoA reductase) the liver uses to make cholesterol. Results are often seen in 4 to 6 weeks.

• Diet and lifestyle can be highly effective, but changes may take 3 to 6 months or more. The degree of improvement depends on adherence, genetics, and overall health.

Live life well.

About Author

Mary Ann Rollano is a writer, registered nurse, and award-winning tea specialist with 40 years of experience in health and wellness. Passionate about the four pillars of health — physical, emotional, spiritual, and social harmony — she blends her expertise in tea, herbs, and nutrition to inspire meaningful connections and happier, healthier lives. Connect with her through her Steeped Stories newsletter.

It is a Signature Event week on the PGA Tour and one of the larger ones at that with play happening at Jack’s place at the Memorial.

Jack Nicklaus is in fact hosting the Memorial Tournament per usual and if you are a professional golfer it is likely a dream of yours to walk off of 18 and shake the hand of one of the greatest people to ever swing a club. That makes sense.

Reigning Masters Champion Rory McIlroy will not be in attendance at the Memorial, something that sparked some criticism when it was first announced last week. Players are entitled to construct and adjust their schedules as they wish and it is worth noting that the PGA Championship was just two weeks ago, but this is the Memorial. It is Jack’s place.

This may sound like posturing, but the reality of the situation is that missing it raises eyebrows from some. Given who Rory is, a Career Grand Slam winner, some people feel he has an obligation to the game of golf to be at events such as these. We can debate that idea forever, obviously.

One thing that is seemingly less open for interpretation is that Rory could have handled his absence from the Memorial with a bit more tact. Speaking on Wednesday, Mr. Nicklaus noted that Rory did not reach out to him to share that he would not be playing in the event.

Mr. Nicklaus shared that he was surprised that Rory was not attending, but he did note tht players have things they have to structure their careers around and shared that he had to go through that himself when he was an active player. That makes sense as well.

If you watch the clip above in its entirety it is clear that Mr. Nicklaus does not want to imply anything negative about Rory missing the Memorial. That is respectable and commendable.

No one is saying that Rory is being disrespectful in going about things the way that he is, but a phone call in this instance would have maybe been a proper move.

Beyond the element that involves Jack Nicklaus, this is now the third Signature Event of the season that Rory is skipping. The days of arguing about the PGA Tour against LIV and what is right and what makes sense and all of that are not worth re-visiting, but it is worth noting that Rory was one of the proponents for the structure that his Tour has in existence right now. Missing a Signature Event is reasonable, but. missing three before June is going to draw criticism in and of itself.

There is no specifically right or wrong thing happening here as Rory is still a global ambassador for the game. We can argue about the manner in which he chose to go about not playing in the Memorial and whether or not he should play in it at all, but that speaks to larger issues surrounding professional golf at the moment (as if that weren’t obvious enough).

Does Rory owe the game more because of who he is and the stature that he carries? That argument can be made. Equally though one could offer that Rory has earned some grace and freedom to operate as he sees fit.

This post is part of a series sponsored by AgentSync.

Today’s insurance agencies rely on an average of 5.7 to 11.9 different technology platforms for day-to-day operations, depending on their total revenue. For large-scale carriers managing multiple agencies and their downstream producers, it’s likely that number is even higher. While this level of digital innovation represents a positive change in the insurance industry’s ability to offer modern experiences to its consumers and efficient workflows to its employees, cultivating a more robust tech stack doesn’t come without challenges.

Each time an insurance organization invests in a new digital solution, it’s creating greater efficiencies for at least one piece of the insurance distribution puzzle. When a business starts out, it may only have the resources to purchase the most essential technology, like an email application and a bookkeeping software. As the business grows, it invests in more technology to help manage the increase in clients and employees — an HR system, a customer relationship management (CRM) system, a compliance management solution, and so on.

While these systems no doubt create greater efficiencies for the business, there’s no denying the irony that the more complex your tech stack gets, the more inefficient it can become. In fact, it’s not uncommon that, as carriers and agencies purchase more systems, they discover some big problems.

How does a complex tech stack impact your insurance business?

Poor integration capabilities lead to fragmented systems

The more systems you add to your tech stack, the more important it is for those technologies to communicate with one another. But with as much as 74 percent of insurance companies still relying on legacy technology for their core business functions, seamlessly linking existing systems to new ones so that they function together in a meaningful way isn’t exactly the norm. Older systems use different data formats, protocols, and structures than modern solutions. These differences can cause significant compatibility issues that make integrations more complex and ultimately lead to system fragmentation.

Silos limit smart, data-driven business decisions

Your distribution channel is filled with data on every downstream partner you work with. Proactive insurance organizations use this data to intelligently expand, contract, and restructure their distribution channels in response to shifting market opportunities and challenges. As a result, data-driven businesses are 23 times more likely to acquire new customers and 19 times more likely to achieve above-average profitability than their less data-driven counterparts. However, data silos, a common symptom of lackluster integrations between multiple systems, make it difficult to leverage producer data for informed decisions. Silos prevent producer data from flowing seamlessly through your systems, creating multiple versions of truth in your records and making it difficult to decipher where the most accurate information actually lives.

Scalability issues prevent profitable growth

When it comes to sustainable growth, automated solutions have been a real game-changer for the insurance industry. For example, these days, with the right distribution channel managementsolution, any carrier onboarding an agency and its multiple downstream producers can validate multiple licenses across multiple lines of authority and multiple states all at the click of a button. Not all that long ago, the same process was only achievable through hours, if not days, of manual work. However, not all automations are created equally and many legacy technologies lack the ability to scale efficiently, making it just as difficult to grow without also increasing overhead costs.

Disjointed systems increase security and compliance risks

Complex and ever-changing regulatory requirements form the backbone of the insurance industry (seriously, we have a whole series about it), making compliance increasingly complex to maintain. Staying on top of regulations and avoiding penalties is particularly challenging when you’re dealing with disjointed systems that are unable to update in real-time, creating inconsistencies in your distribution network data. On top of compliance risk, data security is a major concern for businesses with a complex tech infrastructure. In a study examining the state of cybersecurity across the insurance sector, SecurityScorecard found that third-party software and IT vulnerabilities were to blame for half of the data breaches reported by 150 top insurance firms.

Budget predictions reveal a greater focus on reducing IT complexity

The focus shift makes even more sense when you consider the fact that many insurance carriers and agencies have already invested decades of time and millions of dollars into their existing systems. When it comes to their IT, these folks aren’t looking to reinvent the wheel so much as they’re looking for supplement solutions that will boost their efficiency with as little business interruption as possible.

The solution: Investing in APIs to reduce tech complexity and boost operational efficiency

For businesses with existing distribution channel management ecosystems, application programming interfaces (APIs) offer a solution for improving operational efficiency without ripping and replacing current systems. Modernizing large and complex systems, like those used to manage your insurance distribution channels, can take months or years. APIs reduce tech complexity and get the most complete and up-to-date producer data flowing through your systems more quickly and efficiently than ever before. Carriers and agencies that invest in APIs benefit from their:

Improved integration capabilities: APIs integrate directly into an organization’s existing platforms, opening the door for more seamless data exchange between disparate systems and eliminating bottlenecks in daily workflows.

Seamless, secure scalability: By leveraging APIs that derive data from industry sources of truth, businesses can focus less of their time and resources on data maintenance as their business grows, and more on making the most of the tech infrastructure that drives their core business processes.

Real-time data: APIs can elevate distribution network data quality by synchronizing an organization’s existing tech (and the data that lives within it) with industry sources of truth. Rather than relying on manual data validation, APIs automatically ensure producer data is always up-to-date and useful.

By leveraging APIs, insurance carriers and agencies can transform their tech infrastructure from complex, fragmented, and inefficent to agile, connected, and modern. As a result, they’ll avoid spending the time and money needed to complete a total system overhaul and gain greater visibility into their distribution channel data across their existing platforms.

Let AgentSync’s ProducerSync API meet you where you’re at

If tech complexity is blocking key distribution channel data from flowing through your existing systems, then your data’s not doing you much good. From surfacing key producer data when and where you need it (think before binding a policy or paying out a commission), to highly sophisticated analyses on how to optimize your distribution channel for maximum success, ProducerSync API can be the tech enhancement your business needs at the cost and implementation timeline it wants.

And the hard part of all this, beyond the spending, is that it requires a lot of work.

Or you pay for a service to help you find it.

And while 90% of the benefits can be captured doing those three steps, there are still a lot of different ways you can earn points and miles without a credit card.

If you don’t have time to read it all, here are the top three:

Make sure you’re shopping through a shopping portal to maximize your miles and points

Join the dining programs so you earn points for restaurant visits

Sign up to their emails so you learn about new promotions

The Bilt Mastercard is a card that gives you points when you spend it on rent, up to 100,000 points a year. You will earn 1 point for each $1 spent on rent and it’s the only credit card that lets you do this and it has no annual fee. If you rent and aren’t using this card, you’re leaving points on the table.

You can transfer your Bilt points to a variety of other loyalty programs and sometimes there are even transfer bonuses. Our Bilt review discusses this program in much greater detail.

Shopping portals are websites that you visit first to ensure you earn miles and points for your purchase. If you’ve ever used cashback shopping portals, like Rakuten/eBates or Topcashback, you’re familiar with these websites. You click through to your intended website from a portal and get a small percentage back as cash.

With travel shopping portals, you don’t get cash back but points and miles.

Just search for “[loyalty program] shopping portal” and you’ll probably find it. The exception to this are hotels, it doesn’t appear many hotel loyalty programs have a shopping portal.

Car Rentals

The major car rental companies have partnerships with airlines and can earn miles and points if you enter in a loyalty reward number when renting.

For example, Avis has a partnership with United MileagePlus in which you earn miles based on the rental and your membership level:

General members can earn 500 base miles per rental.

Chase card members can earn 750 base miles per rental.

Premier® Silver and Premier Gold members can earn 1,000 base miles per rental.

Premier Platinum and Premier 1K® members earn 1,250 base miles per rental.

Sign Up For Emails

From time to time, loyalty programs will offer limited time offers which may include free points. They might offer a few hundred points for downloading an app or referring a friend, they only notify folks on social media (which is unreliable) or email, which you have to be subscribed to receive. Make sure you’re subscribed!

Rocketmiles

If you’re booking a hotel, consider using Rocketmiles as it’ll help you earn rewards from a variety of partnerships including airlines as well as Amazon and Amtrak. They have partnerships with more than 40 programs.

Dining Programs

Several loyalty programs are looking to make their way into the OpenTable and Resy business by creating dining programs in which you can earn points for making and keeping reservations.

Many are operated by the Rewards Network and similarly structured.

These include bonus miles for signing up to the program too:

Hotels offer this as well:

Survey Groups

There are some survey groups that pay in miles, which is not exactly an “easy” way to earn miles but one that available to some folks regardless.

Miles for Opinions is a survey company that pays you in American Airlines AAdvantage Miles. You get 250 bonus miles for completing your first survey.

e-Rewards is another survey company that pays in “points” but you can redeem those points for points and miles at a variety of loyalty programs.

Utilities

Did you know that you can earn rewards for various loyalty programs if you select a utility provider through an airline or hotel partnership? You usually get a sign up bonus after two months of service plus points based on spending.

For example, if you live in IL, MA, MD, NJ, or PA and can select an electric supplier, you can earn bonus points from Southwest by selecting this deal with NRG Home. You will earn 10,000 Rapid Rewards points after two months of service plus 2 points for ever $1 spent on the supply portion of your bill. You will have to compare the rates to know if you’re coming out ahead but this is an option.

If you live in CT, MD, NJ, NY, or Ohio and are contemplating going with Energy Plus, you could take this deal and get American Airlines AAdvantage miles. You get 10,000 AAdvantage miles after the second month and you also earn 2 miles for every $1 spent on the supply portion of your bill.

Magazine Subscriptions

If you’re paying a magazine directly for a subscription, you’re probably 1. overpaying and 2. not getting your just rewards.

Within each of the shopping portals, there are partnerships with magazine sellers like Magazines.com and DiscountMags.com. In each case, you can not only earn miles and points for your spending but there are special discount too.

Making that transition will likely save you money and earn you a few points and miles.

Spring is here, but amid the colorfully blooming flowers and lush plant growth lurk triggers of pollen, mold and temperature changes. It’s difficult to enjoy the pleasures of spring when your asthma makes you feel like you have an elephant sitting on your chest. Here are five medication-free techniques to help you breathe easier this season.

Understanding Asthma

Asthma is a chronic respiratory condition that causes inflammation around the lungs and airways. In America, over 24 million people live with asthma. Symptoms include shortness of breath, chest pains, wheezing and cough attacks. Some asthma triggers include food, allergies, the common cold, medication side effects, pollution, physical activity and stress.

While there’s no cure for asthma, you can create an asthma management plan that includes breathing exercises to prevent flare-ups.

1. Pursed-Lip Breathing

This method works for shortness of breath because the exercise gives you more air, making it easier to breathe comfortably.

How to Do It

Relax your body and inhale through your nose for two seconds, but keep your mouth closed — these can be normal breaths. Purse your lips like you’re about to whistle and exhale through your mouth for four seconds. Your exhales should be longer than your inhales.

2. Diaphragmatic Breathing

Training your diaphragm muscles can significantly improve your breathing.

How to Do It

Sit or lie down in a comfortable position.

Place one hand on your chest and the other on your stomach.

Breathe in through your nose, feeling your belly rise.

Using the pursed-lip method, breathe out through your mouth.

3. Buteyko Breathing

Stress and anxiety can trigger asthma attacks, often leading to hyperventilation. While practicing medicine in Moscow, Dr. Konstantin Buteyko studied the connection between breathing and health. His techniques emphasize controlled breathing to manage anxiety and prevent asthma symptoms. Focusing on your breath reduces the risk of triggering an attack.

How to Do It

Sit upright on the floor and take a few normal breaths while relaxing your body. Exhale and hold your nose until you need to breathe again, then inhale. You should then breathe normally for 10 seconds before attempting the exercise again. This method should strengthen your diaphragm.

4. Papworth Method

More than 65% of children have allergies, and research indicates that allergy-prone people are more likely to develop asthma than their peers. Shortness of breath can be frightening for children, making early awareness and management crucial. The Papworth method combines breathing and relaxation to manage triggers.

How to Do It

Breathe in through your nose, letting the breath fill your lungs. Exhale through pursed lips or a relaxed mouth. Lastly, coordinate your breathing with relaxation and moderate movements.

Start by taking deep breaths. Place your hand on your stomach and feel it rise — that’s how you’ll know you’re doing it correctly. After breathing for about a minute, begin your box breathing exercise by inhaling while slowly counting to four. Hold your breath for a slow count of four, then exhale through your mouth for another four seconds. Wait four seconds before your next attempt.

These Techniques Will Help Your Breathing

Breathing techniques don’t replace your inhaler or medication, but learning control with breathwork is a natural stress and anxiety reducer. Practice these exercises daily, and speak to your doctor if a method seems strenuous. Breathe deep and stay calm so you can bloom with the flowers.

Two lawsuits filed in Los Angeles claim major California insurers colluded illegally to impede coverage in wildfire-prone areas, forcing homeowners into the state’s last-resort FAIR Plan. Accusing carriers of violating antitrust and unfair competition laws, the two suits exemplify an ongoing disconnect between public and insurer perceptions of insurance market dynamics, exacerbated by legislators’ resistance to accommodating the state’s evolving risk profile.

An untenable situation

Both suits claim the insurers conspired to “suddenly and simultaneously” drop existing policies and cease writing new ones in high-risk communities, deliberately pushing consumers into the FAIR Plan. Left underinsured by the FAIR Plan, the plaintiffs argue they were wrongfully denied “coverage that they were ready, willing, and able to purchase to ensure that they could recover after a disaster,” Michael J. Bidart, who represents homeowners in one of the cases, said in a statement.

Established in response to the 1965 Watts Rebellion, the California FAIR Plan provides an insurance option for homeowners unable to purchase from the traditional market. Though FAIR Plans offer less coverage for a higher premium, they cover properties where insurance protection would otherwise not exist. California law requires licensed property insurers to contribute to the FAIR Plan insurance pool to conduct any business within the state, meaning they share the risks associated with those properties.

Intended as a temporary solution until homeowners can secure policies elsewhere, the FAIR Plan has become overwhelmed in recent years as more insurers pull back from the market. As of December 2024, the FAIR plan’s exposure was $529 billion – a 15 percent increase since September 2024 (the prior fiscal year end) and a 217 percent increase since fiscal year end 2021. In 2025, that exposure will increase further as FAIR begins offering higher commercial coverage for farmers, homebuilders, and other business owners.

With a policyholder count that has more than doubled since 2020, the FAIR Plan faces an estimated $4 billion total loss from the January fires alone.

Out of touch regulations

Homeowners are understandably frustrated with dwindling coverage availability, which currently afflicts many other disaster-prone states. Supply-chain and inflationary pressures, which could intensify under oncoming U.S. tariff policies, help fuel the crisis. But California’s problems stem largely from an antiquated regulatory measure that severely constrains insurers’ ability to manage and price risk effectively.

Despite a global rise in natural catastrophe frequency and severity, regulators have applied the 1988 measure, Proposition 103, in ways that bar insurers from using advanced modeling technologies to price prospectively, requiring them to price based only on historical data. It also blocks insurers from incorporating reinsurance costs into their prices, forcing them to pay for these costs from policyholder surplus and/or reduce their presence in the state.

Insurers must adjust their risk appetite to reflect these constraints, as they cannot profitably underwrite otherwise. Underwriting profitability is essential to maintain policyholder surplus. Regulators require insurers to maintain policyholder surplus at levels that ensure that every policyholder is adequately protected.

Restricting insurers’ use of prospective data, however, inhibits risk-based pricing and weakens policyholder surplus, facilitating policy nonrenewals and, in serious cases, insolvencies.

Insurance Commissioner Ricardo Lara implemented a Sustainable Insurance Strategy to mitigate these trends, including a new measure that authorizes insurers to use catastrophe modeling if they agree to offer coverage in wildfire-prone areas. The strategy has garnered criticism from legislators and consumer groups, one of whom is suing Lara and the California Department of Insurance over a 2024 policy aimed at expediting insurance market recovery after an extreme disaster.

“Insurers are committed to helping Californians recover and rebuild from the devastating Southern California wildfires,” Denni Ritter, the American Property Casualty Insurance Association’s department vice president for state government relations, said in a statement about the suit. “Insurers have already paid tens of billions in claims and contributed more than $500 million to support the FAIR Plan’s solvency – even though they do not collect premiums from FAIR Plan policyholders.”

A call for collective action

Litigation prolongs – it does not alleviate – California’s risk crisis. Government has a crucial role to play in addressing it, from adopting smarter land-use planning regulations to investing in long-term resilience solutions.

For instance, Dixon Trail, a San Diego County subdivision dubbed the country’s first “wildfire resilient neighborhood,” models the Insurance Institute for Business & Home Safety (IBHS) standards for wildfire preparedness, but not at a cost attainable to most communities, and few local governments incentivize them. Launched by state legislature in 2019, the California Wildfire Mitigation Program is on track to retrofit some 2,000 houses along these guidelines, with the goal of solving how to fortify homes more quickly and inexpensively. Funded primarily by FEMA’s Hazard Mitigation Assistance Grant program, the pilot has thus far avoided the same cuts befalling FEMA’s sister programs under the Trump Administration.

Regardless of what legislators do, California homeowners’ insurance premiums will need to rise. The state’s current home and auto rates are below average as a percentage of median household income, reflecting a combination of the increased climate risk and of the regulatory limitations preventing insurers from setting actuarially sound rates. Insurance availability will not improve if these rates persist.

To quote Gabriel Sanchez, spokesperson for the state’s Department of Insurance: “Californians deserve a system that works – one where decisions are made openly, rates reflect real risk, and no one is left without options.” Insurers do not wield absolute control over that system, and neither do legislators, regulators, consumer advocates, or any other singular group. Confronting the root causes of these issues – i.e., the risks – rather than the symptoms is the only path towards systemic change.

One thing that unites the world is the mobile phone. When you travel internationally, everywhere you go, people have their phones. Most hotels and many restaurants have Wi-Fi. Still, it’s much easier if you have mobile data when you’re out and about. You can call an Uber, look for restaurants nearby, or find walking directions to attractions or public transit stations.

U.S. Carriers Are Expensive

Mobile data is expensive in the U.S. According to a website, the United States ranked #219 among 237 countries in the world for the cost of mobile data (from the least expensive to the most expensive). Some say it’s primarily due to limited competition, high infrastructure costs, and a poor market structure.

As expensive as it is in the U.S., the U.S. carriers charge multiple times more when you travel outside the country. Some plans charge as much as $10 per day. If you’re out 30 days, that would be $300. And that’s only if you buy the international travel pass before you travel. If you use international roaming without pre-arrangement, your mobile data bill could be enormous. A plan I used to use charges $100 to $150 per GB of mobile data in some countries. If you use 4 GB of mobile data, that would be $400 to $600.

A reasonable cost should be more like $10 — not $10 per day — $10 for the whole trip.

Buy a Local SIM Card

A way to avoid the exorbitant charges from your U.S. carrier is to buy a SIM card locally after you arrive in the foreign country. You find a shop at the airport or on the street to buy a SIM card that covers the length of your stay. You put it into your phone but you have to carefully save your existing SIM card. You’ll need it again when you come back to the U.S.

I did this when I traveled to New Zealand in 2016. I bought a SIM card at a store for $5 that covered a whole month.

This works, but it isn’t always easy to find a store that sells SIM cards to international travelers. You may have a language barrier. You have to take precious time out of your vacation to do it. If you lose the tiny SIM card from the U.S., you’ll have to spend time again to replace it after you return.

eSIM

Technology advances since 2016 gave us eSIMs. An eSIM is an electronic equivalent of the tiny physical SIM card. iPhones sold in the U.S. only use eSIMs after iPhone 14 was released in 2022. Other phones released in recent years that still support physical SIM cards also work with eSIMs.

eSIMs don’t have the limitations of physical card trays and card reading contacts. A phone can simultaneously hold two or more eSIMs or one physical SIM plus another eSIM. You can toggle between two SIMs without worrying about losing one.

It also made it much easier to buy a SIM for international travel. You don’t have to find that local store in a foreign country. You can shop online for a wide selection and the best price before you leave.

Chances are that your current phone already supports eSIMs. If you’re not sure, Google your phone’s model plus the word “eSIM” or ask AI.

I use the website esimdb.com when I buy an eSIM. It’s like a search engine for online eSIM vendors. It gets paid a commission by the vendors. I’m not affiliated with it. I use it only because it includes a wide selection.

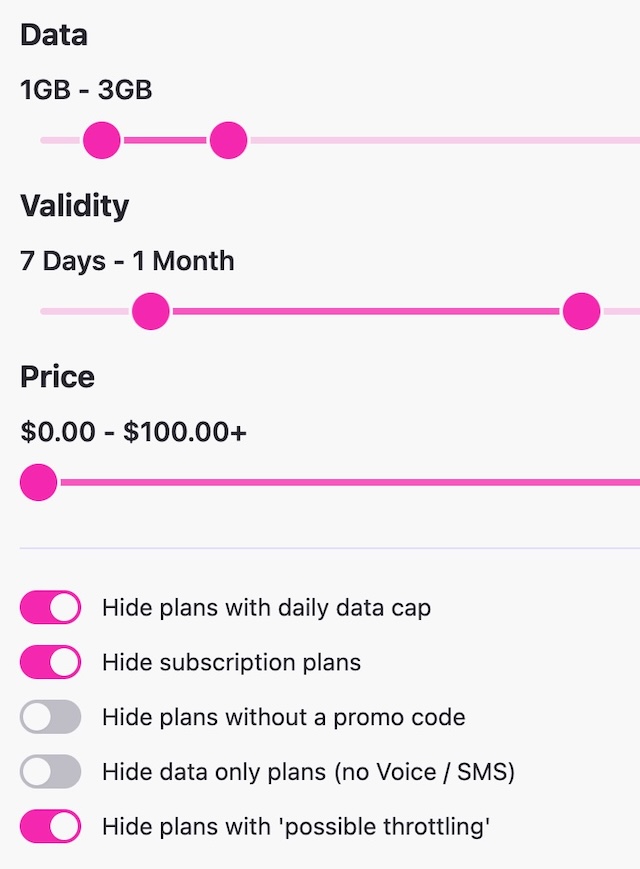

You search by which country you’re traveling to, for how many days, and how much data you need. Some eSIMs cover multiple countries. If you’re going to several countries in a region, get an eSIM that covers all your destinations.

esimdb.com filters

For my typical usage while traveling, 1 GB per week is plenty when hotels have Wi-Fi and I pre-download offline maps. I’m going to Quebec, Canada, for a week. esimdb.com shows multiple vendors that sell a 1 GB eSIM for about $2.

Many eSIMs support top-ups. If you need more data than the amount you originally bought, you can go back to the eSIM vendor and pay more to add more data to your eSIM. eSIMs are quite inexpensive anyway. A 1 GB eSIM for Canada costs about $2. A 2 GB eSIM costs about $4. If I don’t want the hassle of possibly running out, paying $4 versus $2 is a rounding error in travel costs.

I look for eSIM vendors that accept Apple Pay, Google Pay, or PayPal because I don’t want to give them my credit card number directly. If a vendor doesn’t accept Apple Pay, Google Pay, or PayPal, I move on to the next one.

It doesn’t matter if you’ve never heard of the vendors listed on esimdb. I have bought eSIMs from several different vendors for different countries, and the eSIMs all worked as advertised.

You get a QR code by email after you buy the eSIM. You add the eSIM to your phone by scanning the QR code with your phone. Adding a new eSIM doesn’t overwrite your existing SIM. You can switch on and off which SIM should be active. Switch off your U.S. line after you board the plane to avoid international roaming charges.

You can add the eSIM before you leave the U.S., but it will drain your battery a little more when the eSIM keeps looking for its carrier and doesn’t find it. If you decide to add the eSIM when you first land in the foreign country, you must be on Wi-Fi when you add it. You also need to display the QR code on a second device, such as a tablet, to scan it, or you can print the QR code on paper and take it with you.

The inexpensive eSIMs are usually data-only eSIMs. You don’t get a local number for calls and texts, but that’s OK. You can use Wi-Fi calling and messaging apps, such as iMessage or WhatsApp. The eSIM uses a local carrier but it doesn’t necessarily come from a carrier in that country. The eSIM I bought for Spain was assigned a number from Austria. The data roaming setting must be enabled for it to work.

Unlocked Phone

Whether you buy a local physical SIM or eSIM, you need an unlocked phone. A phone locked to a specific carrier doesn’t work with a SIM from a different carrier. If you bought your phone directly from the manufacturer, it’s probably unlocked from day one. Your phone may be locked if you bought it from your carrier at a discounted price or if it’s still on a device payment plan with the phone company.

You can check whether your phone is unlocked if you’re not sure. On an iPhone, it’s under Settings -> General -> About -> Carrier Lock. The menu option for Android phones varies by model. Google the phone’s model and the phrase “carrier unlock status” or ask AI how to find it.

Some phones are still locked after you already satisfied the requirements from your carrier. You can call the carrier and request unlocking. If your current phone is still locked and you can’t unlock it, you may have an older phone that’s unlocked. Put the eSIM on that one and use it for international travel.

Summary

You’ll have mobile data for your phone for usually under $10 for your entire trip if you do these:

1. Check whether your phone supports eSIM. Most recent phones do.

2. Check whether your phone is unlocked. It probably is. Request unlocking from your carrier if it’s locked.

3. Buy an eSIM online for your destination(s) before you leave.

4. Add the eSIM to your phone and switch off your U.S. line at the airport. Remember to enable the data roaming setting for the eSIM.

5. Switch your U.S. line back on after you return and delete the travel eSIM.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.