After a week off, Formula 1 returns to action with the Austrian Grand Prix.

However, a few teams likely welcomed the week away from the track.

A dramatic collision between McLaren teammates Oscar Piastri and Lando Norris knocked Norris out of the race, and dropped him 17 points behind Piastri in the Drivers’ Championship standings, and opened the door to further speculation over how McLaren will handle a championship-caliber car, and two incredibly fast drivers.

That question, and more, are on the docket as the grid heads to Austria.

How does McLaren respond after the Canadian Grand Prix?

Photo by Clive Rose/Getty Images

As the 2025 F1 season began, everyone knew this moment was coming.

That belief did not make it any less shocking when the moment finally arrived.

With McLaren beginning the year as the dominant force on the grid, with the MCL39 the premier package, they looked destined to repeat as Constructors’ Champions, while Norris and Piastri appeared as frontrunners for the Drivers’ Championship.

But an eventual battle between the two — months removed from last year’s “Papaya Rules” storyline — loomed.

That came to a head in Montreal, as the teammates locked horns in the closing laps of the Canadian Grand Prix. As they battled for fourth in the final act of the race, they came together at the run into Turn 1, as Norris tried to squeeze by his teammate on the inside:

Norris took immediate responsibility for the incident (and for “being stupid” in his words) in the moments after the race, even apologizing to Piastri in the media pen. Team Principal Andrea Stella noted that apology in his own comments, as he outlined that a collision between two McLarens is “not acceptable.”

“Well, we never want to see a McLaren car involved in an accident and definitely we don’t want to see the two McLarens having contact, so this situation is a situation that we know is not acceptable,” began Stella after the Canadian Grand Prix.

“At the same time, we appreciate that Lando immediately owned it and apologized to the team, which for us sort of reset the situation. I’m sure he has an important learning point coming from this race, he paid a price in the championship.

“Like I said, we appreciate his behaviour straight after the accident and we will go racing again.”

They indeed go racing again this week in Austria. But as they remain one-two in the Drivers’ Championship standings, will there be another scrap like the one in Montreal between these fast teammates this season?

Marvelous Max Verstappen at Red Bull Ring

Two figures will loom over the festivities this week, one literal, another figurative.

The first is the massive statue that hangs over the circuit in Austria, that will cast a shadow over the sea of orange that assembles to cheer their hero:

Photo by Mark Thompson/Getty Images

The other is how well Max Verstappen has done in this home race for Red Bull.

While how Norris and McLaren rebound from Montreal is likely the main story heading into the Austrian Grand Prix, one cannot overlook Verstappen’s success at Red Bull’s home race. Verstappen has been nothing short of dominant at Red Bull Ring, notching four victories and five pole positions over his career at the Austrian Grand Prix.

One of those pole positions came a year ago, as Verstappen edged out Norris and George Russell to secure P1. While he did not win the 2024 Austrian Grand Prix — more on that in a minute — he did secure a win in the F1 Sprint race at Red Bull Ring last year.

This year is a standard Grand Prix weekend, with no F1 Sprint race, but Verstappen’s success at Red Bull Ring absolutely makes him a threat to win this week.

Still, he will have to keep things clean in Austria, as he remains one penalty point shy of a one-race suspension. The next two penalty points on his FIA Super License are set to expire after this weekend, points that he earned in this race a year ago.

Austria 2024, revisited

While the incident between Piastri and Norris at the Canadian Grand Prix was perhaps the first truly dramatic moment of the 2025 F1 season, it was this race a year ago that offered the first stunning incident of the 2024 campaign, and the battle between Norris and Verstappen.

After a slow pit stop on Lap 52 of last year’s Austrian Grand Prix, Verstappen was left to cling to a lead over Norris. The two battled over several laps, often at Turn 3, and then on Lap 64 the two clashed again, coming together again at Turn 3:

Both Verstappen and Norris suffered punctures, and the damage to Norris’ MCL38 was terminal. Verstappen was able to continue, but he was given a ten-second penalty for causing the collision. That penalty did not factor in his qualification, as he finished fifth, more than 14 seconds behind fourth-place Lewis Hamilton.

Verstappen was also given two penalty points on his Super License for causing the collision, points which expire following this year’s Austrian Grand Prix.

The incident truly kicked off the title fight between the two friends, and speculation about the relationship between the two followed them around the world over the rest of the season. While the two drivers brushed those aside in many a press conference, Austria was not the last time they clashed on the track last season.

Their clash at Red Bull Ring a year ago also opened the door for Russell, who was more than happy to pick up the pieces and claim a win at Red Bull Ring.

Mercedes on the rise

As for Russell, he and Mercedes are coming off a dream weekend at the Canadian Grand Prix. The Mercedes driver captured pole position for the second consecutive season in Montreal, and he was able to hold off Verstappen over the closing laps to secure his first win of the season.

As for his new teammate, rookie Kimi Antonelli, the 18-year-old became the third youngest driver to secure a podium in F1 history with his third-place finish at the Canadian Grand Prix. Only Verstappen and Lance Stroll were younger when they picked up their maiden F1 podium finishes.

Russell’s victory in Montreal pulled him to within 23 points of Verstappen for third place in the F1 Drivers’ Championship standings, and the double-podium result for Mercedes saw the Silver Arrows edge ahead of Ferrari in the battle for second in the Constructors’ standings.

Can they keep it rolling in Austria? It might come down to the weather. Mercedes has been strongest in cooler conditions the past season-plus, which might have Toto Wolff and company watching the weather more than anything else this week.

Frustration at Ferrari

Photo by Bradley Collyer/PA Images via Getty Images

The buildup to the Canadian Grand Prix saw some tension boil to the surface at Ferrari.

Team Principal Frederic Vasseur was forced to respond to reports from Italian media that he was under increasing pressure to keep his position. Both La Gazzetta della Sport and Corriere della Serareleasedreports in the days ahead of the Canadian Grand Prix that Vasseur, as well as other key management figures, were under threat of losing their jobs should the team keep underperforming.

Vasseur fired back in Montreal, with both Lewis Hamilton and Charles Leclerc coming to his defense.

“I don’t know the target. I don’t understand the target. Perhaps it’s to give shit to the team, but in this case I don’t see the point. Perhaps, for them, it’s the only way to exist but it’s really hurting the team,” said Vasseur in Montreal.

“At one stage, it’s the lack of focus and when you are fighting for the championship, every single detail makes the difference. And from the beginning of the weekend we are just speaking about this.

“If it’s their target to put the team in this situation, they reach their goal. But I think it’s really… It’s not like this that we will be able to win a championship. And at least not with this kind of journalist around us.”

“Things aren’t perfect,” said Hamilton. “But for me, I’m here to work with the team, but also with Fred. I want Fred here. I do believe Fred is the person to take us to the top.”

“We have a vision that we share, us three – Fred, Lewis and myself, in order to try and get back to winning. And we’ve been working to put that all together. This is our plan. And we should stick to it,” added Leclerc.

Both Leclerc and Hamilton finished in the points in Montreal, but the double-podium result from Mercedes saw the Silver Arrows slip ahead of Ferrari in the standings, dropping the Scuderia to third.

Can they take that spot back in Austria?

Sauber on the upward track

Change was in the air at Sauber as the 2025 F1 season began.

Last year’s driver pairing of Zhou Guanyu and Valtteri Bottas was out, with the two taking on reserve roles at Ferrari and Mercedes, respectively. In were veteran Nico Hülkenberg and rookie Gabriel Bortoleto, last season’s F2 Drivers’ Champion. Jonathan Wheatley joined the team in the spring as the new Team Principal, coming over from years of service as the Sporting Director at Red Bull.

And these changes come as more are on the horizon, as the team becomes the Audi works operation next year.

But despite the changes, and the tenth-place finish a season ago, Sauber has surprised this year. While they sit ninth in the standings they are coming off a pair of points results, as Hülkenberg finished eighth in the Canadian Grand Prix, and an impressive fifth in the Spanish Grand Prix, as he passed Lewis Hamilton on the final lap to secure a strong result.

Now Hülkenberg heads to another track where he delivered a strong result, as he finished sixth in this race a year ago.

Hülkenberg sat down with F1.com’s Lawrence Barretto ahead of the Spanish Grand Prix, and spoke about what lies ahead for him, and Sauber, as the transition to Audi continues.

“It’s such a reset and a white piece of paper that everyone starts from. It’s impossible to predict anything.

“The big four teams have an advantage in terms of infrastructure and all these kinds of things. But it’s a good opportunity, because it is a reset, it is a fresh start for everyone with these new regulations,” said Hülkenberg.

“It’s extremely exciting and a good opportunity for everyone, including ourselves. We need to work hard, we need to work focused on it and hopefully we’ll come out on the right side of it.”

But while that transition comes next season, can Hülkenberg and Sauber make it three consecutive finishes in the points this week?

Some things can take a “set-and-forget” approach, but your life insurance shouldn’t be one of them! A lot can happen in a year. Think about the changes you’ve seen in your own life: maybe you’ve taken a new job, expanded your family, bought a house, or any number of things.

Since life insurance provides vital financial protection to your family should anything happen to you, it’s important to review it annually to ensure you have sufficient coverage aligned with your ever-evolving life circumstances.

Let’s look at the key factors that make reviewing your life insurance annually a smart choice.

Why Should You Review Your Life Insurance Annually?

You’ve had a job change.

When you start a new job where your earnings are projected to increase, make sure to review your life insurance policy. As your income rises, your spending habits may also change, so ensure that your policy can still provide adequate coverage for your family’s growing financial needs. This same principle applies to a substantial raise or promotion at the same company too.

What about if you’ve recently retired or are planning to retire soon? While it might seem like your time for life insurance is over, this job change is also an important time to review your life insurance policy and make sure that you have the right amount of coverage as you look toward covering your final expenses, paying off any debt and leaving a legacy.

Moreover, if you rely on life insurance provided by your employer, changing jobs would mean that your insurance coverage will be directly affected since policies through work usually end when the job does. This makes checking your insurance policy even more important.

You’re starting a new business.

Starting a new business means incurring more financial and tax obligations. So, whether you’re starting an online store or establishing a brick-and-mortar business, ensure that your insurance coverage can meet your needs.

This way, your business and family can avoid financial turmoil in the event of your passing. Plus, you can also adjust your life insurance coverage to distribute your current estate—including your new business—equally among your beneficiaries.

You’ve had a change in your beneficiaries.

Every year, you should check whether your list of beneficiaries still has the people you want to benefit from your life insurance policy.

The main goal of life insurance is to provide cash to your loved ones when you die, so you want that money to go to exactly who you intended. For example, you may want to remove your ex-spouse as your beneficiary after a divorce or add your adult child as a beneficiary after they turn 18 or 21.

On top of reviewing the beneficiary list of your assets upon your death, you should also consider how your insurance payout would work for each beneficiary based on their location or your relationship. And, of course, it’s important to let your beneficiaries know about your policy and keep them in the loop!

You have a new marital status.

Whether you’re recently married or have gone through a divorce, it’s important to update your life insurance policy to match your current marital status.

If you’ve just tied the knot, reviewing your life insurance ensures that your spouse is protected financially if anything happens to you. You probably have more financial obligations now as a party of two than you did when you were single. How will your partner cover all those expenses without your salary?

Similarly, if you just got divorced, updating your policy guarantees that your children and loved ones are the ones who receive the death benefit rather than your ex-spouse.

Your family has grown.

Whether you’ve had a baby or adopted a child, it’s important to adjust your life insurance policy accordingly. You have more to protect with your life insurance coverage. As children enter the picture, the cost of your expenses goes up. How would your family pay for childcare, groceries, bills and even future college tuition if you were no longer there to contribute to the costs?

Life insurance can help cover those expenses and more so that your children can maintain the same lifestyle after your death.

You bought a house.

If you’ve recently purchased a house, review how you can adjust your insurance policy to ensure that your beneficiaries can cover the cost of your new property in the event of your death.

A period of grief is no time to be forced to sell your home, pack up the family belongings and move to a new neighborhood. Make sure your policy can cover the cost of your mortgage payments, so your spouse won’t have difficulty paying it on one income.

On the other hand, it’s also a good idea to review your policy if you’ve recently paid off your mortgage or refinanced your home.

Your health status has changed.

Updating your life insurance may not be the first thing you think of when you experience a health change, but it’s also an important time to review your policy.

If your health has taken a turn for the worse, that can be a reason to increase your coverage or examine additional coverage opportunities. On the flip side, an improved health diagnosis from losing weight or quitting smoking, for example, might help you get a better rate.

Life Insurance Policy Review Checklist

These life changes are just a few of many times that it makes sense to review your life insurance. When reviewing your policy annually, it’s best to make the necessary changes to ensure that it still addresses all of the factors below:

Your death benefit is sufficient to cover the current financial needs of your beneficiaries in the event of your passing.

Your beneficiary list includes everyone you want to benefit from your life insurance.

The type of life insurance policy you have still meets your needs and expectations.

Your premium payments are still manageable and affordable.

Your policy isn’t going to lapse soon.

You’re taking advantage of any new coverage options that your insurance company may offer.

One of the best ways to make sure your loved ones are fully protected is to work with a licensed insurance agent who can walk you through the entire process.

Apple Bank CD rates are very competitive. How much interest you can earn depends on the term lengths and deposits. One thing for sure is that the longer the term, the more money you’ll make over time. For example a 15-month Apple Bank CD rate is at 4.25% APY.

Of note, if you’re looking to earn more money on your investment, it might make sense to consider working with a financial advisor.

See the best Apple Bank CD rates that are available for you below:

Term

Interest Rate

APY

3 month

3.24%

3.30%

6 month

3.44%

3.50%

9 month

3.68%

3.75%

1 year

3.92%

4.00%

15-month

4.16%

4.25%

18-month

3.44%

3.50%

2-year

3.44%

3.50%

3-year

3.44%

3.50%

4-year

3.44%

3.50%

5-year

3.44%

3.50%

Apple Bank CD Rates: An Overview

Apple Bank CD rates are the most competitive out there. They offer higher rates than most Bank CDs. And you will certainly earn considerably more interest than a regular savings account or money market fund. While Apple Bank offer higher CD rates, it requires a minimum of $1,000. Apple Bank is based in New York City. It has several physical branches and you are able to receive customer service in person. You can open a CD for a 3-month term all the way to a 5-year term. The highest rate you can receive right now is 4.25% which represents the 15-month term. Other rates are still competitive than what most brick and mortar banks are offering.

What is a certificate of deposit (CD)?

CDs are certificates that banks or credit unions sell to you. Banks issue them to you for a specific dollar amount for a specific length of time. The time period could be anywhere from 1, 6, 12 or 24 months to several years. The bank pays you some interest. You get your full principal back plus interest you earn once the CD matures or “comes due.” If you want your money back before it matures, you can withdraw it.

But you will get hit with a penalty for early withdrawal. However, there are some banks, like CIT Bank, that offer CDs with no penalty. Certificate of deposits just like bank savings accounts are very safe. That is because they are FDIC insured for up to $250,000. So, if you’re looking for safety for your cash and competitive yield, CDs are some of the best short term investments to consider.

What is the difference between a bank CD and a brokerage CD?

Two types of certificates of deposits exist. One is Bank CD; the other is brokered CD. Apple Bank issues bank CDs. Others, such as Vanguard, offer “brokered CDs.” Brokered CDs are issued by banks. They are sold in bulk through brokerage firms such as Vanguard and Fidelity.

Bank CDs and brokered CDs are FDIC insured up to $250,000. Apple Bank CD rates are usually competitive, and they tend to provide higher yields than other bank CDs. The longer term CDs such as the Apple Bank 15-month CD offer high rates.

Are Apple Bank CDs right for you?

Given that Apple Bank CD rates are very competitive, they may be a good choice for you. So, you may want to consider them if:

You’re investing for a short-term goal, such as buying a house, in the next few years.

You are looking for peace of mind knowing that your money is insured by the FDIC.

You’re looking for an investment that provide higher yields than banks savings accounts;

You want a low-risk place to keep your cash.

What are the Apple Bank CD rates?

Apple Bank offers CDs ranging from 3 months to 5 years. As you can see in the table above, the longer the term of the CD, does not necessarily mean the higher the rate. For example, an Apple Bank CD for a 15-month term offers a 4.25% yield. Whereas a Apple Bank CD’s rate for a 5-year term is only 3.50%. You can buy Apple Bank CDs commission free and you can sell them commission free before they mature.

Apple Bank 5-Year CD Rates

The applicable rate for a 5-Year Apple Bank CD is currently 3.50%. And it requires a minimum deposit of $1,000. This is the longest Apple Bank CD term out there. And its interest rate exceeds most CD rates you’d get from banks. Learn more about this product and apply on Apple Bank’s secure website.

Apple Bank 4-Year CD Rates

This 4-year Apple Bank CD also requires a minimum deposit of $1,000. This CD’s yield is the same as the Apple Bank 5-year CD. Also, it’s higher than most bank CDs. The yield is currently is 3.50%.

Apple Bank 3-Year CD Rates

The applicable yield for a 3-Year Apple Bank CD is still very competitive. It’s 3.50% and requires a $1,000 deposit.

Apple Bank 2-Year CD Rates

The rate for a 2-Year Apple Bank CD is 3.50% and a minimum deposit of $1,000 is required.

Apple Bank 18-Month CD Rate

For a 18-Month Apple Bank CD, the yield is 3.50%. The minimum deposit is $1,000.

Apple Bank 15-Month CD Rates

For a 15-Month Apple Bank CD, the yield is 4.25%. This is the highest rate of all the CDs offered. The minimum deposit is still relatively low: $1,000.

Apple Bank 1-Year CD Rates

The yield for a 1-Year Apple Bank CD is 4.00% and a minimum deposit of $10,000 is required.

Apple Bank 9-Month CD Rate

The applicable yield for a 9-Month Apple Bank CD is still very competitive. It’s 3.75% and requires a $1,000 deposit.

Apple Bank 6-Month CD Rates

The yield for a 6-month Apple Bank CD is currently 3.50%. Apple Bank CD requires a $1,000 minimum deposit.

Apple Bank 3-Month CD Rate

For a 3-Month Apple Bank CD, the yield is 3.30%. The minimum deposit is $1,000.

Alternative to Apple Bank CDs: Best Vanguard Mutual Funds:

If Apple Bank CDs do not do it for you, or you’re looking to get more return on your money, then try to invest in the best Vanguard mutual funds out there. That way your money is still safe and you get more money.

Mutual funds are some of the best ways to invest your money. One thing to be aware is that mutual funds invest in stocks and bongs. These securities tend to be volatile. Therefore, you might lose some or most of your investment if the market goes down. So, beginner investors wishing to invest in these Vanguard Funds should also consider learning how the stock market works.

Bottom line

Apple Bank CDs might be a good choice for you if you want to avoid risky investments and you are saving your money for a short-term goal such as going on a vacation. Indeed, Apple Bank CD rates are better than bank savings accounts and money market funds. But the money is only available after the CD “matures.” On the other hand, if access to your money at anytime is a priority, check out the best Vanguard Mutual Funds.

Tips for Maximizing Your Savings

If you have questions beyond Apple Bank CD rates, you can talk to a financial advisor who can review your finances and help you reach your goals. Find one who meets your needs with SmartAsset’s free financial advisor matching service. You answer a few questions and they match you with up to three financial advisors in your area. So, if you want help developing a plan to reach your financial goals, get started now.

Hi friends! Happy Friday! How are you? I hope that you’ve had an amazing week. I’m sorry for the crickets over here this week – I only managed to publish two posts because we were living up our last few days in Sevilla. One of the biggest gifts to myself during this long trip was that I pre-wrote 12 blog posts before we left. It gave me the chance to truly unplug and enjoy, and now we’re home and it’s back to the routine!

He was finishing up training since he headed back to the airlines, and while we were hopeful the timing would work out with the trip, I didn’t work out that way. Since he was going to be gone anyway, the girls and I went for it and I’m so so glad we did. They’re older now which makes things easier, but it was definitely a core memory girls’ trip! I still have some Spain posts on the way, including some of my tips, Airbnb recipes, how I travel with zero jet lag, Barcelona’s gluten-free food tour, and the food, so stay tuned for those!! If you have any questions for upcoming posts, please lmk!

In the meantime, I’m here in a hoodie from the copius air conditioning (bless it) and snuggling with Miasey. I’d love to hear what you’ve been up and what you have going on this weekend!

Some pics from our last week:

An incredible dinner at Petra. This spot wins for my favorite tortilla, and I tried a LOT of them while we were there 😉

Pollo Asado aka Chicken Man. We had pollo asado SO many times while we were in Sevilla, since it was right down the street from our Airbnb. They had chickens roasting and you just had to tell the guy how many you’d like, he’d get your chicken, cut it up and put it into a container, and drizzle with juice from the roasting dish. It was $11 and the BEST chicken. I’m going to miss it!

The Pilot made it! He finished up training and hopped on a jumpseat out to meet us. He got there just in time for the Father’s Day celebration at Isla Mágica, which is a water park and theme park. We were with four other families and all of the kids (and adults) loved it.

That night, we walked to La Cabonería, which is a bar with live flamenco. We got there just in time for the show; it was perfect! We enjoyed some tinto de verano and amaaazing flamenco.

Bullfighting ring and museum. While I would never attend a bullfight, I was interested to see the museum and such an important part of Sevillano culture and history.

Cañabota. Enjoyed a lil Michelin star double date night with Sam and Tony. This meal was EPIC. Everything was so fresh and beautifully prepared. 10/10 recommend.

(the liquid in the glass to the far right was “water gazpacho.” It was clear but tasted exactly like gazpacho!)

My beautiful friend Sam! I’m so glad that our babies decided that they were best friends forever when they were barely 3 years old.

It’s time for the weekly Friday Faves party. This is where I share some of my favorite finds from the week and around the web. I always love to hear about your faves, too, so please shout out something you’re loving in the comments section below.

6.20 Friday Faves

Fashion + beauty + random:

New dress find! I grabbed this at Corte Inglés (my favorite multi-level department store in Spain) before we left. The brand is Maksu.

Giving a round of applause to my pre-Spain manicure. I was determined for them to be zero maintenance while we were gone, so I asked for flowers + a shade that matched my natural nails so they could grow out. The tech nailed it. This is 7 weeks of growth and you can only see it if you look closely. From a distance, they still look fine.

Read, watch, listen:

Don’t forget to check out this week’s podcast episode here about why you’re not losing weight, even if you’re doing all the things.

I watched four movies on the flight home! West Side Story (the new version is really above and beyond from the acting, costumes, choreography, casting), new Father of the Bride (super cute and fun), new Snow White (I feel like despite the bad press/reviews, it was fine) and Pearl Harbor (can you believe I’ve never seen the entire thing???). My eyes were BURNING afterwards, but it was a once every 10 years kind of thing lol.

Fitness, health, and good eats:

Back home to my red light. It felt so good to use this again and I felt an instant energy boost. (FITNESSISTA saves you $260)

The Sangre de Cristo mountains loom over Colorado’s San Luis Valley. Many in this agricultural region voted for President Trump and are deeply concerned about cuts to Medicaid.

Hart Van Denburg/CPR News

hide caption

toggle caption

Hart Van Denburg/CPR News

In southern Colorado’s San Luis Valley, clouds billow above the towering mountains of the Sangre de Cristo range. A chorus of blackbirds whistle, as they flit among the reeds of a wildlife refuge. Big circular fields of crops, interspersed with native shrubs, give it a feel of bucolic quiet.

Despite the stark beauty in one of the state’s most productive agricultural regions, there’s a sense of unease among the community’s leaders as Congress debates a budget bill that could radically reshape Medicaid, the government health program for low-income people.

“I’m trying to be worried — and optimistic,” said Konnie Martin, CEO of San Luis Valley Health in Alamosa. It’s the flagship health care facility for 50,000 people in six agricultural counties — Alamosa, Conejos, Costilla, Mineral, Rio Grande and Saguache.

The numbers out of the bill about deep Medicaid cuts were “incredibly frightening,” Martin said, “because Medicaid is such a vital program to rural health care.”

Konnie Martin is CEO of San Luis Valley Health in Alamosa.

Hart Van Denburg/CPR News

hide caption

toggle caption

Hart Van Denburg/CPR News

Martin’s hospital is not alone. “I think in Colorado right now, nearly 70 percent of rural hospitals are operating in a negative margin,” in the red, Martin said.

Across the hall from her office is Shane Mortensen, the chief financial officer. “The bean counter,” he said with a slight grin.

The hospital’s annual budget is $140 million, and Medicaid revenues make up nearly a third of that, according to Mortensen.

The operating margin is razor thin, so federal cuts to Medicaid could force difficult cuts. “It will be devastating to us,” Mortensen said.

Lifeline for health care

The region is one of the state’s poorest. Two in five of Alamosa County’s residents are enrolled in Health First Colorado, the state’s Medicaid program.

It’s a lifeline, especially for people who wouldn’t otherwise have easy access to health care. That includes low-income seniors who need supplemental coverage over and above Medicare, and people of all ages with disabilities. More than 2,500 working age adults in the county with incomes lower than $20,820 a year also qualify, and would be among those most likely to lose coverage under current proposals.

Envisioning a future with deep cutbacks leaves many patients on edge.

“I looked into our insurance and, oh my goodness, it’s just going to take half my check to pay insurance,” said Julianna Mascarenas, a mother of six. She says Medicaid has helped her cover her family for years. “Then how do I live? Do I insure my kids or do I keep a roof over their head?”

Julianna Mascarenas, a mother of six, says Medicaid has helped cover health care for her family for years.

Hart Van Denburg/CPR News

hide caption

toggle caption

Hart Van Denburg/CPR News

Mascarenas works as a counselor treating people with substance use disorder. Her ex-husband farms, potatoes and cattle, for employers that don’t offer health insurance.

“So those moments that I was a stay-at-home mom and he’s working agriculture, what would’ve we even done? I don’t even know,” she said, when asked what would have happened if Medicaid wasn’t there. “Now that I think back, what would have we done? We would’ve had to pay out of pocket.”

Or go without. Across the state, Medicaid covers one in five Coloradans, more than a million people.

That includes children in foster care.

“We’ve had 13 kids in and out of our home, six of which have been born here at this hospital with drugs in their system,” said Chance Padilla, a foster parent. “Medicaid has played a huge part in just being able to give them the normal life that they deserve.”

He and his husband, Chris, who are both clinic managers, get reimbursed by Medicaid for the costs of providing for the kids that have lived with them. “These kids require a lot of medical intervention,” said Chance Padilla.

The program also covers mental health services for foster children. “At one point, we had a preteen that needed to be seen three times a week by a mental health professional,” Chris Padilla said. “There’s no way that we could have done that without Medicaid.”

What happens to cancer and maternity care?

San Luis Valley Health’s lobby is modern, built of red brick and glass. Down a hallway is the cancer center where patients come for chemotherapy transfusions. Nurse Amy Oaks demonstrates how they ring a ceremonial bell, to celebrate each time a patient finishes a course of treatment.

“It’s just a happy time,” said Oaks. “It’s exciting. It gives you the chills, makes you cry.”

But hospital staff and administrators wonder whether federal cuts would make it hard for the hospital to keep the cancer center running.

“It could be pretty dramatically affected,” said Dr. Carmelo Hernandez, the chief medical officer.

Hernandez’s specialty is obstetrics and gynecology. The hospital has its own labor and delivery unit, the type of service that other rural hospitals across the U.S. have struggled to keep open.

Dr. Carmelo Hernandez, the chief medical officer at San Luis Valley Health in Alamosa, specializes in obstetrics and gynecology. He and other hospital leaders wonder if some services, including obstetrics, can stay open after deep Medicaid cuts.

Hart Van Denburg/CPR News

hide caption

toggle caption

Hart Van Denburg/CPR News

“If we don’t have obstetric services here, then where are they going to go?” Hernandez asked. “They’re going to travel an hour and 20 minutes north to Salida to get health care, or they can travel to Pueblo, another two hour drive over a mountain pass to get health care.”

Tiffany Martinez, 34, works with kids who have disabilities. She was recently forced to think about that possibility after giving birth to her fourth child, Esme, three weeks ago.

Her pregnancy was high risk, requiring twice-a-week ultrasounds and stress tests at the hospital. She’s enrolled in Medicaid and said it’s critical for many moms in the valley.

“Everything down here is low pay,” said Martinez. “It’s not like we have money to just be able to pay for the doctor. It’s not like we have money to travel often to go to the doctor, so it’s definitely beneficial.”

About 85 percent of the hospital’s labor and delivery patients are covered by Medicaid. As the program has expanded over the years, many of the patients who got added were married women from working families.

“It impacted the whole family because of course that’s a little nucleus then that grows with the care of the family and the well-being of the family,” said Christine Hettinger-Hunt, the hospital’s chief operating officer.

Hospital heals, and also employs

With 750 workers, the hospital is the valley’s largest employer. One of those employees is Dr. Clint Sowards, a primary care physician. He grew up in the region, went away for school and came back to a good-paying job.

Sowards is focused on the fact that fewer Medicaid funds will make it harder to attract the next generation of doctors, nurses and other health providers.

Certain medical specialties might no longer be available, Sowards explained. “People will have to leave. They will have to leave the San Luis Valley.”

Dr. Kristina Steinberg is a family medicine physician with Valley Wide Health Systems, a network of small clinics serving thousands. She said Medicaid covers most nursing home residents in the area. “If seniors lost access to Medicaid for long-term care, we would lose some nursing homes,” she said. “They would consolidate.”

The program also pays for vaccines for children. In two nearby communities, Colorado recently recorded its first cases of measles this year, which is highly contagious.

“If you are on Medicaid, you don’t have any insurance, you pretty much qualify for free vaccines for children,” Steinberg said. “And I can see our vaccines dropping off dramatically if people have to pay for vaccines, because some of them are very expensive.”

Medicaid sustains a local level of health care that is then available to the wider population, including patients on Medicare and commercial insurance, according to administrators and clinicians.

“We really utilize Medicaid as sort of the backbone of our infrastructure,” said Audrey Reich Loy, a licensed social worker and the hospital’s director of programs.

“It doesn’t just support those that are recipients of Medicaid, but as a result of what it brings to our community, it allows us to ensure that we have sort of a safety net of services that we can then expand upon and provide for the entire community.”

Seeking more efficiency

Republicans in Congress say they want to save money and make the government more efficient. Their budget would cut taxes by trillions of dollars — and possibly cut social safety net programs like Medicaid.

Many in this region voted for President Trump — in Alamosa County, he topped 54 percent. Hernandez admits Medicaid cuts could give people here second thoughts.

“He’s potentially affecting his voter base pretty dramatically,” said Hernandez, noting politics is a sensitive topic that he mostly doesn’t discuss with patients. “I can’t imagine that hasn’t crossed some people’s minds.”

Sowards, the family medicine physician, says he’s baffled by the idea of potentially slashing Medicaid spending. He understands that some people believe the Medicaid system is ailing and costly. But he has grave doubts about the proposed cure.

“Just because we fall and break our wrists and our wrist is broken, doesn’t mean that we need to cut off our arm, okay?,” he said. “Losing Medicaid would have drastic repercussions that we can’t foresee.”

Local economy depends on health care

Deep Medicaid cuts could pack a punch for the wider regional economy as well.

The small city of Alamosa is the hub of the San Luis Valley. It has a main street in the midst of revitalization. It has hotels, restaurants, shops and a coffee shop called Roast Cafe.

On a recent Wednesday, barista Ethan Bowen prepped a specialty drink called a Drooling Moose. “It’s a white chocolate mocha with a little bit of caramel in there,” he said.

The coffee shop and its adjacent brew pub do pretty good business here — in part because of foot traffic from nearby San Luis Valley Health, which is a “huge part of the local economy,” Bowen said.

Joe Martinez is president of San Luis Valley Federal Bank, the valley’s oldest financial institution. It’s on the next block.

He said the valley is home to three of the poorest counties in the nation. A lot of its people are enrolled in Medicaid “and the individuals that partake in the program don’t necessarily have the financial means to travel outside of the San Luis Valley for health care.”

Cuts would hit hard

The hospital’s regional economic impact is more than $100 million a year, with Medicaid accounting for a major part of that, Martinez said.

Any Medicaid cuts would hit the hospitals hard, but also affect small businesses and their employees. The region is already feeling economic stress from other changes, like recent cuts the Trump administration made to the federal workforce.

The San Luis Valley is home to the Monte Vista National Wildlife Refuge, Great San Dunes National Park and other federally-managed lands.

Martinez said recently laid off federal workers are already coming to banks, saying, “‘Can I find a way to get my next two months mortgage payments forgiven? Or can we do an extension? Or I lost my job, what can we do to make sure that I don’t lose my vehicle?’”

Ty Coleman, Alamosa’s mayor, traveled to Washington, D.C., in April to talk to the state’s Congressional delegation. He said his message about Medicaid cuts was straightforward: “It can have a devastating economic impact.” Coleman put together a long list of possible troubles: more chronic disease and mortality, longer wait times for care, medical debt and financial strain on families.

Downtown Alamosa, a hub for the San Luis Valley’s agricultural economy, is also home to breweries, coffee houses, retail, and public art.

Hart Van Denburg/CPR News

hide caption

toggle caption

Hart Van Denburg/CPR News

“It’s not just our rural community, but the communities, rural communities, across Colorado as well and the United States,” Coleman said. “And I don’t think people are getting it.”

Cuts would create ripple effect

Medicaid cuts indirectly can impact other economic sectors, like education.

“One of the biggest factors driving state higher education funding downis state spending on health care,” said David Tandberg, president of Adams State University in Alamosa. The college has roughly 3000 students and is next door to the hospital. It’s the region’s second-largest employer.

If federal cuts are made to Medicaid, Tandberg said, the state of Colorado will then be forced to pay more to maintain health care services. This year, Colorado is facing a billion-dollar budget deficit. Public universities like his will find they’re competing with medical institutions for precious state funding. “So anytime I hear about Medicaid cuts, it makes me nervous,” he said.

Waymo has announced plans to test self-driving cars in 10 more U.S. cities, including San Diego and Las Vegas, in 2025. After years of slow progress and technical roadblocks, this expansion signals that autonomous vehicle (AV) technology is finally gaining ground.

But not everyone’s on board. A recent AAA survey revealed that 6 in 10 U.S. drivers are scared to ride in a self-driving car. This fear is holding back adoption, even as companies like Waymo, Tesla, and Cruise continue testing and expanding AV programs across the country.

With this in mind, The General decided to look into the safety of autonomous vehicles using real-world data from the National Highway Traffic Safety Administration (NHTSA), the U.S. Department of Transportation, and The Robot Report. This article breaks down how the technology works, crash rates, disengagement factors, and what problems still need solving.

How Autonomous Vehicle Technology Works

Autonomous vehicles use a mix of sensors, machine learning, and real-time decision-making to drive without human input, but not all systems are created equal. The NHTSA makes an important distinction between Automated Driving Systems (ADS) and Advanced Driver Assistance Systems (ADAS). ADS controls the car entirely in specific conditions, while ADAS supports human drivers with features like lane-keeping or automatic braking.

Self-driving cars use radar, lidar, cameras, and onboard computers to monitor their surroundings and respond quickly to what’s happening on the road. These tools help the vehicle track traffic, road conditions, and obstacles. Artificial intelligence takes in all that information and makes fast decisions, similar to how a human driver would react. Even with all that tech, companies like Waymo still rely on human drivers during testing as part of their safety practices. These drivers are trained to jump in if something goes wrong.

Waymo’s autonomous vehicles have driven over 56 million miles in the U.S. so far. Data from these experiences helps refine the technology, improve safety protocols, and build trust with the public and regulators.

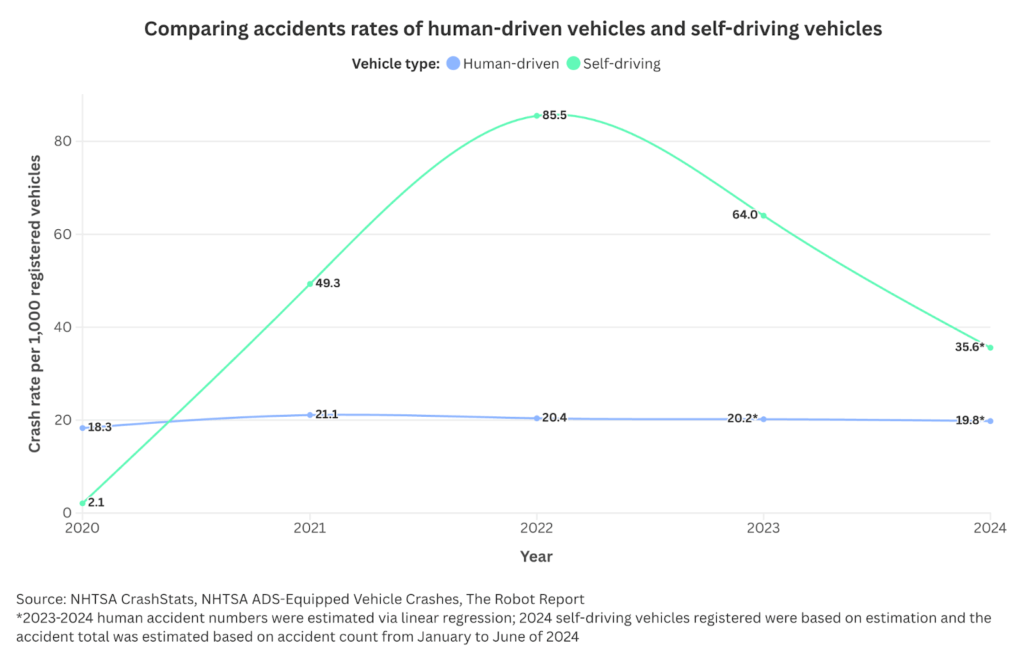

As self-driving cars log more miles, the big question isn’t how many crashes they’re involved in, but how often. Raw numbers don’t tell the whole story, especially as more AVs hit the road.

From 2021 and 2023, self-driving cars had a much higher crash rate per 1,000 vehicles than human-driven ones. The gap has narrowed, dropping from 85.5 per 1,000 in 2022 to an estimated 35.6 in 2024, but that’s still almost double the human driver rate, which hovered near 20 per 1,000 vehicles.

AV tech still has room to grow, but it’s improving. According to Waymo’s safety impact report, their self-driving cars have significantly reduced the rates of crashes involving injuries, airbag deployments, and police reports compared to human drivers in Phoenix and San Francisco.

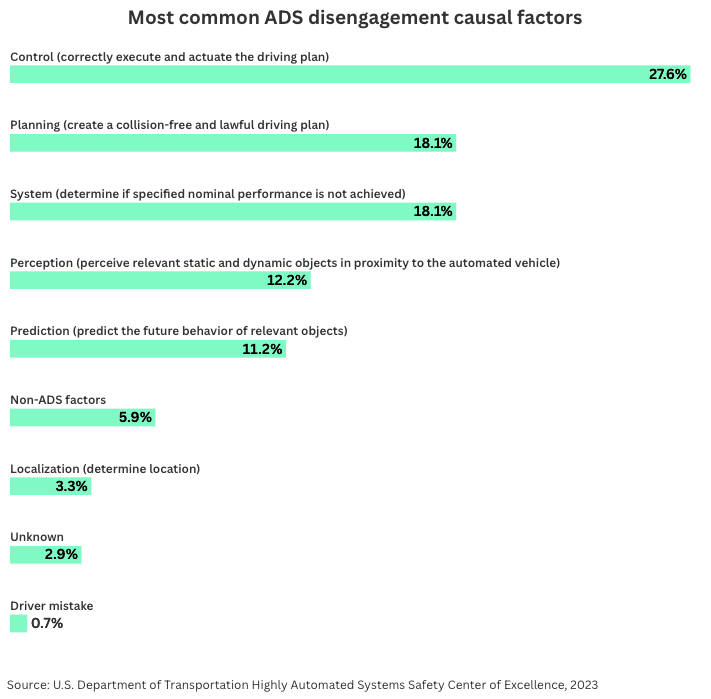

Disengagements: When Humans Take Over

Even the most advanced self-driving cars aren’t fully self-sufficient yet. A key measure of progress in AVs is the disengagement rate, when the vehicle either hands control back to a human or the human safety driver decides to take over. These moments are important for spotting weak points in the technology.

Control errors. The car failed to execute the driving plan correctly, such as turning, stopping, or steering.

Planning failures. The system couldn’t figure out a safe, legal path to keep driving.

System issues. The car didn’t perform the way it was supposed to during regular driving conditions.

Perception gaps. The AV struggled to detect nearby objects or traffic accurately.

Prediction errors. The system couldn’t correctly forecast how other drivers or pedestrians would move.

Ongoing Issues and Challenges

One of the biggest challenges for self-driving cars is handling complex, unpredictable situations. Things like human behavior, construction zones, and bad weather can throw them off. They also struggle with subtler moments, like reading signals from a traffic cop or reacting to drivers who break the rules. These movements can be difficult to account for in advance, which makes it hard to guarantee safety in every scenario.

Today’s AI isn’t ready for everything the road can throw at it. That’s why companies like Waymo are putting so much time and energy into making it smarter. Waymo is building AI models that don’t just follow the rules. They’ll also be designed to see and react to the world around them more like a human would. These models aim to combine driving experience with broader reasoning skills, so the system recognizes patterns, predicts how others might behave, and makes smarter decisions in real time.

But there’s still the problem of AV data collection and reporting. Safety and disengagement reports vary from one manufacturer, state, and testing program to the next. A lack of standardization or clear benchmarks makes it difficult to compare performance results and get a clear picture of what’s working, what’s not, and how safe these vehicles actually are.

Moving Forward: Trust, Testing, and Transparency

No longer a futuristic concept, self-driving cars are here, and they’re improving. AVs have logged millions of miles and learned from thousands of incidents. They’ve also started to narrow the safety gap with human drivers, but they’re not there yet when it comes to fully replacing people behind the wheel.

Disengagements, perception errors, and planning failures are still common. To move forward, the industry needs transparent safety data and standardized reporting. Without that, it’s hard to know which systems are truly getting better and which just look good on paper.

Public trust also matters. Most drivers still feel uneasy about self-driving cars. Building confidence will take more real-world testing, smarter regulations, and continual tech improvements, not just promises from AV companies.

Autonomous driving isn’t perfect, but it’s evolving fast. If the industry can balance innovation with responsibility, the next few years will be a turning point.

Home » Insurance » Life » How Much Does A Million Dollar Life Insurance Policy Cost?

Understanding the cost of a million-dollar life insurance policy can be pivotal in securing your family’s financial future. But have you ever wondered just how accessible or costly such a policy might be?

Do you think a million-dollar term life insurance policy sounds like too much insurance?

As a Certified Financial Planner, I see underinsured people every day.

What do I tell them?

A million-dollar term life insurance policy might actually be the minimum coverage needed for the typical middle-class household, but it’s affordable.

That might sound like an exaggeration, but if you crunch the numbers – just as we’ll be doing a little bit – you’ll realize that a million-dollar policy might be just what you need.

The good news is term life insurance isn’t nearly as costly as most people think.

What makes term life insurance even better is that larger policies cost less on a per thousand basis than smaller policies do. You may find the premium on a $1 million policy is only a little bit higher than it is for $500,000.

Do You Really Need a $1 Million Term Life Insurance Policy?

Probably, but let’s find out. A general rule of thumb is that you should get 10x your income as baseline coverage for life insurance.

If you’re young, that may be low because you may want to provide your family with enough to replace your income for 15 years or more.

Today, $1 million has become the new baseline forlife insurance by a primary breadwinner. Anything less could leave your family financially impaired.

Typical Obligations to Add When Calculating the Amount You Need

Here’s a list of all the different obligations you may want to have life insurance cover in the unfortunate event you pass away early.

Your Income (And for How Many Years)

Any Debt You May Want to Be Settled

Future Obligations Such as College for Children

Other Obligations Such as Business

Typical Items You Can Subtract When Calculating the Amount You Need

Current Life Insurance Policies

Assets (Like Cash or Stock) You Might Choose to Use Instead of Life Insurance

Now that you have an idea of these obligations, let’s punch them into this life insurance calculator to find out if you need a million-dollar policy.

Choosing A Million Dollar Insurance Policy

According to PolicyGenius, the average cost for a 20-year $1 million term life insurance policy for a 35-year-old male is $53 per month. However, your rate will vary according to the following factors.

Factors that affect your rate:

Your Coverage Amount and Policy Term

Where to start?

The best, and easiest place to start is online. I recommend having two or three insurers compete for your business to make sure you get the best rate and coverage. To see how cheap term life can be, choose your state from the map above to be matched with top life insurance providers instantly.

Factors That Affect How Much You Need

Let’s look at the individual components that can quickly add up to over a million-dollar policy.

Income Replacement

This is where things can get a bit intimidating. Even if you earn a modest income, you may need close to $1 million to replace that income after your death in order to provide for your family’s basic living expenses.

The conventional wisdom in the insurance industry is that you should maintain a life insurance policy equal to between 10 times and 20 times your annual income. So if you earn around $50K per year, that would mean policy coverage between $500K and $1 million.

The complication today is that with interest rates being as low as they are that might not be enough either.

For example, if you have a $1 million policy that could be invested at 5% per year, your family could live on the interest earned – which conveniently comes to $50,000 per year – for the next 20 years.

That would still leave the original $1 million intact to cover other expenses. But with today’s microscopic interest rates, there’s no way to get a guaranteed return of 5% on your money, certainly not for 15 or 20 years.

EXPERT TIP

That brings us back to simple math – multiplying your annual income times the number of years your family’s living expenses will need to be covered. This alone can require a $1 million life insurance policy.

Also, keep in mind that most insurance companies have a maximum multiplier you can apply to your income for life insurance coverage. For example, it wouldn’t make much sense for a 22-year-old making $27,000 per year to get a $2 million life insurance. Or a 65-year-old that is retired to secure a $3 million dollar policy.

The table below is approximately how much you’re allowed to multiply your income based on your age and income:

Applicant’s Age

Annual Income Multiplier

18-29

35x

30-39

30x

40-49

25x

50-59

20x

60-69

15x

70-79

10x

80+

5x

Using the table above as a guide, a 35-year-old making $150,000 per year would be capped at taking out a $4.5 million term policy ($150,000 x 30 = $4,500,000).

Your Final Expenses

Here we start with the basics – wrapping up your final affairs.

Crazy, right? You can get burial insurance to cover only the most basic of final expenses.

Outstanding Debt

Debt burdens are high in the US, and debt can be especially crushing on remaining family members. Many life insurance customers make sure they can pay off most of their debt with the policy.

Medical Debt

Medical costs are a serious variable. Even if you have excellent health insurance, there are likely to be unpaid medical bills lingering after your death. This has to do with copayments, deductibles, and coinsurance provisions.

Collectively, they can add up to many thousands of dollars. But where things get really complicated is if you die of a terminal illness.

For example, if you are stricken by an illness that lasts for several years, you could incur a number of expenses that are not covered by insurance. This may include the cost of personal care and even experimental treatments.

Mortgage

A home may be a large asset, but it’s also often a homeowner’s largest debt. The average mortgage balance in the US is roughly $236,443 according to Experian data. So you could easily use a life insurance policy to pay off that debt and relieve your loved ones of a monthly mortgage payment.

Personal Debt

Credit card debt and other personal debt are some of the most expensive obligations carrying rates upward of 20% in some cases. Make sure you have enough to cover this very expensive debt.

Future Obligations For Your Family

Below is a sampling of major expenses your family is likely to incur, either on an annual basis or at some point after your death.

College

Tuition costs continue to skyrocket. The Department of Education suggests that four-year public college tuition has been rising an average of 5% per year, far exceeding the rate of inflation. If you have one child who attends an in-state public school, a second at an out-of-state public school, and a third in a private university, the total expenditure will reach $416,560.

Annual cost at in-state public college: $20,770 ($83,080 for four years)

Annual cost at out-of-state public college: $36,420 ($145,680 for four years)

Annual cost at a private college: $46,950 ($187,800 for four years)

Transportation

Vehicles and other forms of transportation represent another large sum. Unfortunately, with increasing electronics and safety features, the average cost of a new car continues to grow.

Health Insurance

If your family relies on your work for healthcare, take notice. According to eHealth.com, the average health insurance premium for a family is $22,221. That’s a shade under $2,000 per month in additional cost. This cost will only rise, and the need could last for years.

Other Obligations You May Need to Cover

So far, we’ve been describing the financial obligations likely to affect a typical household. But there may be certain situations that will produce obligations that are less obvious.

Business Owners

For example, if you’re a business owner, there may be debts or other financial obligations that will need to be paid upon your death.

Even though no one in your family may be qualified or interested in taking over your business, the payoff of those obligations may be completely necessary to enable the sale of the business.

Real Estate Investor

Another possibility is that you’re a real estate investor.

If your properties are heavily indebted, extra insurance proceeds may be necessary either to carry the properties until they’re sold, or even to pay off existing indebtedness to free up cash flow for income.

You may even need additional funds if you are taking care of an extended family member, like an aging parent.

These are just some of the many possibilities of expenses that will need to be covered by insurance proceeds.

Factors Affecting Your Life Insurance Premiums

Before we move on to specific life insurance quotes, let’s first consider the factors that affect term life insurance premiums.

Age

This is typically the single most important premium factor. The older you are, the more likely you are to die within the term of the policy.

Health

This is a close second and why it’s so important to apply for a policy as early in life as possible. Premiums on life insurances rates literally increase by each year.

If you have any health conditions that may affect mortality, such as diabetes or hypertension, your premiums will be higher. This is another compelling reason to apply while you are young and in good health.

It’s not that policies are not available to people with health conditions, it’s just that they’re less expensive if you don’t have any.

Policy Term

A 10-year term policy will have a lower premium than a 20-year term policy, which will be lower than a 30-year term. The shorter the term, the less likely it is the insurance company will have to pay a claim before it expires.

Policy Size

Size of the policy matters, but not the way you might think. Yes, a $1 million policy will cost more than a $500,000 policy. But it won’t cost twice as much.

The larger the policy, the lower the per-thousand cost will be.

When the size of the death benefit is considered, the larger policy will always be more cost-effective.

Work, Hobbies, and Habits

For example, certain occupations are more hazardous than others (think policeman versus librarian). Deep-sea diving is higher risk than golf. And smoking is the one activity guaranteed to raise your premiums substantially.

With this information in mind, let’s take a look at whether you should consider a $1 million whole life policy instead.

$1 Million Term Life Insurance vs Whole Life?

Any discussion on life insurance should include a comparison of whole life and term life insurance coverage. After all, both products can be immensely valuable in the right situation, yet one product (whole life) costs considerably more than the other.

Most of the time, the debate is settled in favor of term life insurance based on cost alone.

A whole life insurance policy can easily cost 10x the same amount of coverage you can get with a term policy.

With that being said, whole life insurance and other investment-type life insurance coverage can be valuable in terms of the cash value you can build up over time. Whole life insurance also offers a fixed benefit amount for your heirs that will last for your entire life, yet the cost of your premiums are guaranteed to stay the same.

The cash value of a whole life insurance policy also grows on a tax-deferred basis, and you can borrow against this amount if you need a loan. Further, many whole life policies from reputable providers also pay out dividends during good years, which can be substantial.

Why Young Families Choose Term Coverage

The problem with whole life and other similar policies like universal life is the fact that premiums can be exorbitant for the amount of coverage you might need.

A couple with young children provides a good example since they might need a $1 million dollar policy or more to provide income protection for their working years and have money left for college tuition and other expenses.

With young families, expenses are already high.

This includes costs for food for a family, childcare, heavy use of health care, and the seemingly endless demand for clothing, furniture, and even entertainment as the children grow.

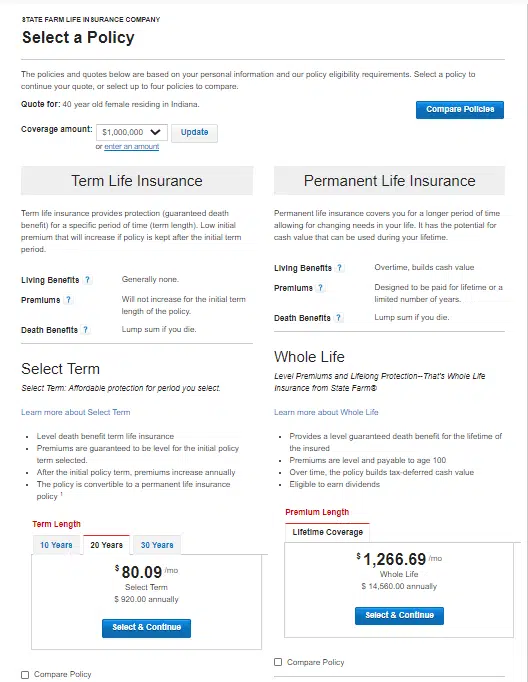

As you can see from the cost comparison below from State Farm, there’s not enough room in the typical family budget to afford the type of life insurance that’s needed.

A 40-year-old mother and breadwinner in excellent health would pay $80.09 per month for a term life policy that lasts 20 years, whereas a whole life policy in the same amount would cost $1,266.69 per month (or $14,560 annually).

This is a classic situation where term insurance rides to the rescue. The family can afford to buy the amount of coverage they need at an affordable price, whereas paying for permanent life insurance coverage in the same amount would be difficult to justify.

And just as important for people of any age and in any circumstance, the extra funds not being spent on insurance premiums can be invested to gradually improve your financial situation.

So absolutely, term insurance will work best for most people.

$1 Million Life Insurance Rate Examples

As you’ll notice, each table has a wide array of information. Knowing that everybody is in a different situation, I wanted to make sure that I offered term life quotes for almost every conceivable situation.

For those that think that a million-dollar term policy is expensive, you’ll quickly notice that a 25-year-old male in good health only costs $645 per year while a 35-year-old costs $795.

On a monthly basis that’s almost next to nothing!

AGE

SEX

COMPANY 1

COMPANY 2

COMPANY 3

25

MALE

BANNER LIFE $645

NORTH AMERICAN CO. $645

TRANSAMERICA $650

25

FEMALE

AMERICAN GENERAL $514

NORTH AMERICA CO. $515

SBLI $520

35

MALE

BANNER LIFE $795

GENWORTH FINANCIAL $804

ING $808

35

FEMALE

SBLI $640

AMERICAN GENERAL $694

GENWORTH FINANCIAL $695

45

MALE

BANNER LIFE $1,885

GENWORTH FINANCIAL $1891

AMERICAN GENERAL $1,894

45

FEMALE

SBLI $1,450

BANNER LIFE $1,455

AMERICAN GENERAL $1,456

20-Year $1 Million Term Life Policy

There is a big drop-off in life insurance rates between a 20 year and a 30 year since underwriters do not have to worry as much about life expectancy.

For many people, a 20-year policy gets them exactly where they want to be in life when the policy term runs out.

AGE

SEX

COMPANY 1

COMPANY 2

COMPANY 3

25

MALE

AMERICAN GENERAL $414

BANNER LIFE $425

SBLI $440

25

FEMALE

AMERICAN GENERAL $354

SBLI $360

BANNER LIFE $365

35

MALE

SBLI $450

BANNER LIFE $455

NORTH AMERICA CO. $485

35

FEMALE

SBLI $390

AMERICAN GENERAL $404

BANNER LIFE $405

45

MALE

BANNER LIFE $1,155

SBLI $1,160

GENWORTH FINANCIAL $1,173

45

FEMALE

SBLI $880

BANNER LIFE $895

TRANSAMERICA $930

10-Year $1 Million Term Life Policy

Once again, you get a $200 drop in the annual premium by losing another 10 years on the term.

If your life insurance agent isn’t giving you all these term options and is only focused on the death benefit, then you need a different agent.

AGE

SEX

COMPANY 1

COMPANY 2

COMPANY 3

25

MALE

SBLI $260

BANNER LIFE $285

MINNESOTA LIFE $290

25

FEMALE

SBLI $230

BANNER LIFE $245

ING $248

35

MALE

SBLI $270

BANNER LIFE $295

MINNESOTA LIFE $300

35

FEMALE

SBLI $240

BANNER LIFE $255

ING $258

45

MALE

BANNER LIFE $585

TRANSAMERICA $630

GENWORTH FINANCIAL $637

45

FEMALE

SBLI $520

BANNER LIFE $525

ING $528

$1 Million Policy for Smokers – Rates Increase

For all you smokers out there – beware! The cost of your life insurance balloons as you’ll see here. If you’re considering kicking the habit, now is as good time as any.

Some life insurance companies will give you a lower rate if you complete a recognized smoking cessation program, and go on without smoking for at least two years.

It won’t help your immediate situation, but when you see the premium on smoker life insurance rates below, you might agree that it’s something to work toward!

AGE

SEX

COMPANY 1

COMPANY 2

COMPANY 3

35

MALE

North American Co. $3595

SBLI $3630

MetLife $3639

35

FEMALE

North American Co. $2555

Transamerica $2720

Prudential $2765

10 steps to securing a million life insurance policy:

If you’ve made the decision that $1 million of life insurance is the right amount of coverage you need and you’re ready to purchase a policy, here are the steps you’ll need to follow.

1. Determine How Much Coverage You Need: This is the first and most important step in securing a million life insurance policies. You need to have a clear understanding of how much coverage you actually need.

2. Choose the Right Type of Policy: There are whole life, term life, and Universal life policies available. Choose the one that best suits your needs.

3. Shop Around: Don’t just go with the first life insurance company you come across. It’s important to compare life insurance rates and coverage from a few different companies before making a decision.

4. Consider Your Health: If you’re in good health, you’ll likely qualify for lower rates. However, if you have health issues, you may still be able to get coverage, but it will probably be more expensive.

5. Consider Your Lifestyle: If you have a risky job or hobby, that could affect your rates.

6. Get Quotes From Multiple Companies: This is the best way to compare rates and find the cheapest policy.

7. Read the Fine Print: Make sure you understand all the terms and conditions of the policy before buying it.

8. Buy Online: You can usually get cheaper rates by buying life insurance online.

9. Pay Attention to Your Payment Schedule: Most life insurance policies require monthly or annual payments. Be sure you can afford the payments before buying a policy.

10. Review Your Policy Regularly: Life changes, and so do life insurance needs. Be sure to review your policy regularly to make sure it still meets your needs.

Following these steps will help you get the best possible rate on a million-dollar life insurance policy.

Make sure you understand all the terms and conditions before signing on the dotted line. Also, make sure to shop around and compare rates from multiple companies before buying a policy.

Yes, I know I’ve said that a few times in this article, but it’s worth repeating. Many people go with the first life insurance company they call, and that isn’t kind to their checkbook. It pays to shop around.

Here’s what you need to know about choosing the best life insurance company for your $1 million policy:

The Best Companies to Purchase $1 Million Life Insurance

When choosing the best life insurance company, it’s important to consider the overall financial health of the insurance company. You want to make sure the company you choose is stable and will be around for years to come. You also want to consider things like the company’s customer service rating and claims-paying ability.

There are a lot of different life insurance companies out there, so it can be difficult to know which one is the best. Each company is rated by different organizations, so it’s important to look at multiple ratings before making a decision.

Rating agencies are the “Report Card” for life insurance companies. Choose a company with straight A’s!

The companies that rate insurance companies are A.M. Best, Moody’s, and Standard & Poor’s.

A.M. Best is a credit rating agency that specializes in the insurance industry. They rate insurance companies on their financial stability.

Moody’s is another credit rating agency. They also rate insurance companies on their financial stability.

Standard & Poor’s is a credit rating agency that rates companies on their financial stability.

The following life insurance companies are all rated A+ (Superior) by A.M. Best and are considered to be financially stable and have a good claim-paying ability.

These are just a few of the many life insurance companies out there that could provide you with a $1 million life insurance policy.

When choosing a life insurance company, it’s important to consider their financial stability, customer service rating, and claims-paying ability. The companies listed above are all rated A+ (Superior) by A.M. Best and are considered to be financially stable with a good claims-paying ability.

Northwestern Mutual, New York Life, MassMutual, Guardian Life, State Farm, Nationwide, USAA, MetLife, The Hartford, and Allstate are all good choices for life insurance companies.

You can’t put a price on peace of mind, and with a $1 million life insurance policy you can have the peace of mind knowing that your loved ones will be taken care of financially if something happens to you.

Bottom Line: How Much Does A $1 Million Dollar Life Insurance Policy Cost?

Getting a one-million-dollar term life insurance policy is not as expensive as most people believe. You can start getting quotes today from a variety of top life insurers by selecting your state from the map above.

Even those who opt for the more expensive permanent life insurance policy will many times be surprised at the price.

Either way, you can get these larger amounts of coverage and still not break the bank. But get your policy now, while you’re still young and in good health.

FAQ’s on $1 Million Life Insurance Policy

How much does a $1,000,000 term life insurance policy cost?

The cost of a $1,000,000 life insurance policy will vary based on factors like your age, health, and lifestyle. However, you can expect to pay around $250 per year for a healthy 30-year-old. According to Ladder Life, a $1 million term life policy for healthy 30-year-old males costs around $2.08 per day.

How does a $1,000,000 term life insurance policy work?

A $1 million term life insurance policy is a type of life insurance that provides coverage for a specific period of time, usually 10-20 years. If you die during the term of the policy, your beneficiaries will receive a death benefit of $1 million. If you live past the term of the policy, the policy will expire and you will not receive any death benefit.

A $1 million term life insurance policy is a good choice for people who want to make sure their loved ones are taken care of financially if something happens to them. It can also be a good choice for people with a lot of debt, like a mortgage or student loans, that they want to make sure is paid off if they die.

Can anyone buy a million-dollar life insurance policy?

For the most part, yes; but there are examples of people who cannot buy life insurance. For instance, people with a terminal illness or those who have been diagnosed with a life expectancy of fewer than two years are not able to purchase life insurance policies.

The other factors are your income, affordability, and suitability. If you cannot afford the premiums, then you will not be able to purchase the policy. And if your income is say less than $50,000 then the insurance company may not think it’s suitable to purchase a $1 million life insurance policy.

Is a million-dollar life insurance worth it?

A million-dollar life insurance policy may not be right for everyone, but it can be a good idea if you have a lot of debt or if you want to make sure your family is taken care of financially if something happens to you.

No one likes to think about their death, but it’s important to have a life insurance policy in place in case something happens to you. A million-dollar life insurance policy can give you and your loved one’s peace of mind knowing that they will be taken care of financially if something happens to you.

Who offers the best million-dollar life insurance policy?

There is no one-size-fits-all answer to this question, as the best policy for you will depend on your specific needs and preferences. However, some of the top providers of million-dollar life insurance policies include AIG, Banner Life, and Prudential. So be sure to explore your options and compare quotes from different providers before making a decision.

Do insurance companies offer million-dollar insurance policies with no medical exam?

Yes, insurance companies offer million-dollar insurance policies with no medical exam. However, the premiums for these policies are typically much higher than for policies with a medical exam.

We’re living longer than ever before—but are we living better?

Thanks to medical advancements and lifestyle shifts, the average lifespan has increased more than our great-grandparents ever imagined.

But there’s a catch: we’re spending more of those extra years in poor health. And for women, that reality hits even harder.

Lifespan vs. Healthspan: What’s the Difference?

Let’s break it down:

Lifespan is the number of years we live.

Healthspan is the number of those years we’re actually healthy.

In other words? Quantity vs. quality.

According to the World Health Organization, the average global gap between lifespan and healthspan is nearly 10 years. In the U.S., it’s worse: 12.4 years. And for women, the gap is even bigger. We’re looking at spending 13.7 years—more than a decade—in declining health, often battling chronic conditions like osteoporosis, heart disease, and cognitive decline.

Can We Control Our Healthspan?

Some health influencers would have us believe that our healthspan is entirely within our control. Even with genetic predispositions, they argue that our lifestyle choices and mindset influence how our genes express themselves.

And yes—many factors that support longevity are well-known: smart exercise, a nutritious diet, quality sleep, and caring for our mental health.

But this narrative overlooks major systemic barriers—food insecurity, limited access to wellness education or preventive care, biased public policy, social norms, and inequities that disproportionately affect women and marginalized communities.

The Gender Health Paradox: Why Women Suffer More

Here’s the kicker: Women live around six years longer than men—but we suffer more. It’s called the gender and health paradox.

The reasons for this are layered—hormonal shifts, caregiving responsibilities (for both our kids and our parents), healthcare inequities, and socio-economic barriers all play a role.

The Economist’s Health Inclusivity Index points out that women, especially older ones, face compounded disadvantages. Caregiving, work interruptions, and less access to preventative care leave many of us navigating aging with fewer resources and more strain.

And don’t forget: In 2023, the U.S. dropped from 27th to 43rd in the global gender parity rankings based on four main areas—work, education, health, and political leadership.

4 Longevity Habits That Support Healthspan

Aging is a complex and multidimensional topic. Even so, there are some research-backed longevity habits that can help put more life in our years. Let’s touch on a few of them.

1. Nourish Your Body with Protein-Rich Foods

There’s no magic-bullet diet, but whole, nutrient-dense foods that provide adequate macronutrients and micronutrients support long-term health.

For older adults, protein becomes especially important. Research shows that increased protein intake can help offset sarcopenia (age-related muscle loss) and the decline in physical performance that often comes with age. It’s not just about staying strong—it’s about maintaining independence and reducing fall risk.

You don’t need to count every gram, but do aim to include high-quality protein with every meal: think beans, fish, yogurt, eggs, and lean meats.

2. Prioritize Strength Training

Both cardio and strength training are essential to a long, healthy life. Most people are already aware that aerobic exercise boosts heart and vascular health, mood, and endurance—all essential. The rising piece for many women is strength training.

Why? Because building and maintaining muscle isn’t just about aesthetics—it’s about function, bone density, and disease prevention. Strength training reduces the risk of cardiovascular death in women by up to 30%, according to recent studies. While we should aim for 3-4 sessions per week, even one makes a measurable difference.

Yet fewer than 20% of women strength train consistently—often due to intimidation, misinformation, or outdated cultural norms. Let’s change that.

Start small. Lift something heavy. And reclaim your strength.

3. Community: The Underrated Longevity Tool

Strong relationships are a longevity superpower. According to Dr. Robert Waldinger, director of Harvard’s 80+ year Study of Adult Development, “the people who stayed healthiest and lived longest were the people who had the strongest connections to others.”

Yet more than 1 in 5 Americans report feeling lonely. And loneliness isn’t just emotionally painful—it’s biologically harmful, linked to everything from heart disease to dementia.

Connection doesn’t have to be complicated. Schedule a walk with a neighbor. Join a book club or volunteer group. Try something new—gardening, dance, painting, hiking—and do it with others. Community is medicine.

4. Change How You Think About Aging

Here’s a mind-blowing concept: how we think about aging can literally change how we age.