A sweeping new piece of legislation known as the “Big Beautiful Bill” is packed with tax breaks, expanded deductions, and changes to key government programs. This bill could dramatically alter the financial landscape for millions of Americans. Here’s what you need to know.

Read more:

Existing Tax Rates Become Permanent

PeopleImages.com – Yuri A/shutterstock.com

The lower tax rates from the Tax Cuts and Jobs Act of 2017 were set to expire in 2025. The “Big Beautiful Bill” will make those tax breaks permanent.

Taxpayers who receive tips will be able to deduct up to $25,000 per year in tips from their taxable income, provided they earn under $150,000 ($300,000 on joint returns). A “qualified tip” is money paid voluntarily by the payor; therefore, mandatory service charges do not qualify. Credit card tips are eligible, but the value of gifts are not. The taxpayer must be in an occupation that customarily and regularly receives tips.

For overtime, the deduction is capped at $12,500 ($25,000 for joint returns), provided they earn under $150,000 ($300,000 for joint returns).

Deduct Auto Loan Interest

shutterstock.com

Those with car loans can write off up to $10,000 in interest paid to qualifying car loans for the next three years, and you do not have to itemize to claim the deduction. A key factor, however, is that the car must be new and assembled in the U.S.

The Big Beautiful Bill calls for a $6,000 deduction for those 65 and older who earn $75,000 or less ($150,000 joint). This would effectively eliminate taxes on Social Security for 88% of seniors.

Cap on State and Local Deductions Increases

shutterstock.com

When you pay state and local taxes, you can deduct a portion of those funds from your federal taxable income. The cap on this amount is currently $10,000 but Trump’s bill increases that amount to $40,000 for the next five years.

Medicaid Work Requirement

Medicaid recipients in 40 states and D.C. will have to either work, volunteer, or go to school for at least 80 hours per month to continue to receive benefits. Recipients can receive exceptions, such as being disabled and having young children.

Some recipients may also see a $35 charge when seeing the doctor if their income is between 100% and 138% of the federal poverty line (between $15,650 and $21,597).

ACA Reporting Requirements

Photo by Nataliya Vaitkevich: https://www.pexels.com/photo/woman-in-black-long-sleeve-shirt-sitting-with-hand-on-her-head-6919757/

Those who receive their health insurance through the ACA marketplace will now have to update their income and other details every year, rather than being automatically re-enrolled.

Boost Child Tax Credit to $2,200

Photo by Robert Collins on Unsplash

The current child tax credit is $2,000, but that was set to expire in 2025, reverting back to $1,000. The bill permanently raises this credit to $2,200.

I don’t mess around when it comes to comfort. I am not the sacrifice-comfort-for-style kind of gal.

And bras? Whew. Bras are high stakes—especially when you wear a DD+ cup size. Too tight, too itchy, too stabby? NOPE. That’s why 90% of my daily bra rotation consists of stretchy bralettes and light-support sports bras that feel like a gentle hug, not a medieval torture device.

But here’s the twist: I also want to feel put together. You know—lifted, smoothed, like I care enough to wear appropriate underwear. I run a business, for goodness’ sake.

So it would be great to find the holy grail of bras: enough support to look polished, but without all the wires, seams, itchy lace, and other bra-related distractions.

It’s 2025. Surely that’s not too much to ask from a wire-free bra for DD+ sizes, right?

And since they came through last time with some great wired bras (all of which dethroned and booted all the wired bras I had been wearing), I asked them to help me find the wireless unicorn and bring her home to my underwear drawer.

Enter: Three Wire-Free Bras for DD+ Sizes That Actually Support from Wacoal

When Wacoal sent me a few of their wire-free bras to test, I was intrigued. Because, in my experience, wireless bra options for DD+ cup sizes tend to fall into one of two categories:

Comfortable but flimsy and droopy.

Supportive but … hmmmm how shall I put this … orthopedic.

Could these really thread the needle? Only one way to find out.

So I test drove the options and here are my top three picks.

Keeping It Real Disclosure: This post is sponsored by Wacoal, and the bras featured were provided for review. Additionally, some of the links in this post are affiliate links, which means that if you purchase through them, we receive a small commission—at no extra cost to you. This helps support our writers and everything we do here at Fit Bottomed Girls. As always, all thoughts, opinions, and unfiltered bra struggles are completely my own.

1. Feeling Flexible Bralette: A Second-Skin Wire-Free Bra for Ultimate Comfort

The vibe: Support but make it feel like I’m wearing nothing at all

This was the first one I tried, and friends—I did not expect to love this as much as I did.

Seriously, THE MOST COMFORTABLE BRA I’ve ever had on my body. Hands down, with zero exaggeration (and I’m really, really picky). I will be buying more of these so I don’t have to be without it or do laundry every day.

If your current bralette drawer is full of droopy lace triangles that do nothing and decorative straps that never let you forget you’re wearing a bra, this one’s going to blow your mind.

It’s insanely soft and smoothing with a full-coverage scoop neck that actually offers light support but feels amazing.

What I loved most: ✔ Taller back and side panels that eliminate that uncomfortable, pinching bra bulge

✔ Double-layer fabric for light support and second-skin feel ✔ Wide, non-digging straps and band that really stay put so there’s no fussing with fabric ✔ Super smooth finish that disappears under tanks and tees ✔ No itchy seams anywhere on this baby

I can – and have – comfortably slept in this bra AND it still gives me enough support for walking the dogs, running errands, or hopping on a Zoom call with clients and still look put-together.

The verdict: This is the elevated bralette of my dreams. I plan to live in this one for the foreseeable future.

2. Simply Done Wire-Free T-Shirt Bra: The Best Wireless Bra for Natural Lift and Everyday Wear

This one looks like your typical t-shirt bra—smooth cups, light contouring, clean lines. But unlike traditional t-shirt bras that secretly try to saw your ribs in half by lunchtime, this one skips the underwire and still delivers on shape and support.

Unlike the Feeling Flexible Bralette (above), this one has thinly-padded, molded cups that make it look and feel more like a bra so it would be perfect for those looking for more lift, separation, shaping, and support than a bralette offers.

What I loved: ✔ Thin foam cups for natural contouring and that traditional t-shirt bra shape ✔ Wire-free design that still gives the girls a lift ✔ Fully adjustable straps that can convert to crisscross style ✔ Stretchy, smooth band that lays flat without pinching

This one had more structure than the bralette but was still comfy enough for all day wear and let me forget I was wearing it. And honestly, it’s the better choice if you are wearing anything that’s lower cut or just prefer something with more lift and separation.

The verdict: Perfect if you want the classic molded cup look without the classic molded cup rib-digging misery.

3. Back Appeal Wire-Free T-Shirt Bra: A Structured, Wire-Free Bra That Smooths and Shapes

You know how sometimes you put on a bra and immediately feel a little taller and more streamlined—like you just got a mini posture upgrade?

That’s this one. First of all, it’s just so damn pretty. The texture and feel of the fabric gives it an elevated, luxurious feel.

It is the most structured of the two molded cup wireless bras I tried and the molded cups in this one are foam so they were slightly thicker than the Simply Done (above).

So if you like that lifted, no lumps, no bumps, no nipple show through—then this is your new best friend.

What I loved: ✔ Seamless full coverage foam cups that lift and shape

✔ Microthin spacer fabric band designed to minimize back and side bulge ✔ A smooth bottom band that stays put all day long

This one has a bit more of a “secure” feel to it—like you get from a wired bra but you know, without the wire. I’d reach for this on days when I want a little more structure, lift, and shape without wires.

The verdict: This is a confidence booster bra. You’ll feel fancy in it but you don’t have to sacrifice your comfort in the process.

Final Thoughts: Are Wacoal’s Wire-Free Bras for DD+ Sizes Worth It?

Absolutely. Here’s the deal:

They’re very thoughtfully designed. They fit real bodies that have to move around (not just mannequins). And they actually deliver on support without stabbing you in the sternum all day to remind you they’re there.

If you’re tired of choosing between “comfy but saggy” and “lifted but miserable,” Wacoal’s wire-free collection is 100% worth a try.

And with their free virtual fitting service, you can skip the awkward dressing room dance and actually get a bra that fits your body—without guessing your size in a fluorescent-lit panic.

Ready to upgrade your bra drawer?

🛍️ Check out Wacoal’s full wire-free collection right here.

Then come back and tell me: What’s your biggest wire-free bra complaint—and did Wacoal fix it? Let’s talk boobs in the comments. You know I’m always down. —Alison

A new report offers insights for U.K. efforts to improve areas with polluted water supplies.

PIEN HUANG, HOST:

England’s land – so goes an old song – is green and pleasant, but for years, many of its rivers have been dirty and gross. That’s because of sewage discharge that causes pollution and has led to considerable controversy around the nation’s privatized water system. Now, a major new review is shaking up the industry and cleaning up the waterways, as Willem Marx reports.

WILLEM MARX, BYLINE: Humans have lived near the River Kennet in the west of England for thousands of years. Today, so, too, does James Wallace, who’s shown me what was one of his family’s favorite swimming spots.

(SOUNDBITE OF BIRDS CHIRPING)

JAMES WALLACE: It is beautiful, but as we step towards the water edge, we can see this carpet going along the bottom of algae, which is snuffing out the opportunity for life. And it means that on the top, on the surface, we see a vibrant, healthy habitat, and beneath, we see a dead one. And that is because of sewage pollution.

MARX: The pollution comes from a nearby sewage treatment plant, run by a company called Thames Water. It’s now nationally notorious. In May, it was fined nearly $165 million, a record, for discharging untreated sewage into rivers, with a separate fine for paying hefty but unjustified dividends to its shareholders.

WALLACE: We’re seeing the places like this, which are highly protected, natural environment, are being trashed by corporate profits.

MARX: Wallace runs an environmental campaign group called River Action and wanted me to see Thames Water’s nearby treatment plant, a few miles upriver.

(SOUNDBITE OF FOOTSTEPS)

WALLACE: How about I show you some of the wilder bits?

MARX: Behind a green metal gate, the facility handles smelly household sewage and rainwater runoff. But as Britain’s population increases and its rainfall dwindles under climate change, pressure on the overall water system has increased, while spending on it has historically not.

WALLACE: The system was designed to cope with it years ago, but not now. Because of a lack of investment across the industry, not just Thames Water, it means the whole of Britain is exposed to a serious crisis in water pollution.

MARX: And after sewage started clogging the country’s waterways and stinking up shorelines, that systemwide crisis has prompted a massive public outcry. The U.K. was once known as the dirty man of Europe thanks to its industrial pollution. That improved with the introduction of environmental rules. But then Margaret Thatcher privatized the Victorian age system, and ever since, a couple dozen companies – of which Thames Water is the largest – have been responsible for providing fresh water and removing raw sewage. It’s a system that’s largely failing, says Bertie Wnek, an infrastructure expert at the policy consultancy Public First.

BERTIE WNEK: What we have is a situation where companies have been kind of incentivized to bring on a load of debt onto the system over time, and we’re finding now that we’re sort of paying the price for that behavior.

MARX: The U.K.’s water regulator had long prioritized low bills for customers, preventing companies from raising revenues as much as they wanted. So some like Thames relied instead on borrowing money to invest in new infrastructure and generate their profits, amassing huge debts along the way.

HUGO TAGHOLM: This is both an environmental issue. It’s a health issue, but it’s also a financial scandal.

MARX: Hugo Tagholm is a surfer and swimmer who led the campaign group Surfers Against Sewage. He’s now with the nonprofit Oceana and criticizes companies for extracting tens of billions of dollars from the industry as profits rather than reinvesting.

TAGHOLM: This is something that’s enraged the public. The system needs, you know, massive investment, and that really should come from shareholders and the owners of those businesses rather than the customer.

MARX: Many companies acknowledge investment is needed but argue responsibility for new funding should lie with regulators and political leaders, says Jeevan Jones, chief economist at the industry’s advocacy group, Water UK.

JEEVAN JONES: The way to get investment is through clear regulation, strong steers from governments and a system that brings in the finance and the investment projects that upgrade those networks and increase our supply.

MARX: For its part, Thames Water said in a statement this May that it takes its, quote, “responsibility towards the environment very seriously” and says the U.K.’s water regulator, quote, “acknowledges that we’ve already made progress to address issues raised.” Keir Starmer’s government has commissioned an independent report into these problems. The final findings come out this month and will likely suggest an entirely new system of regulation. That can’t come soon enough, says Bhikhu Samat, legal director at the U.K. law firm Shakespeare Martineau, where he specializes in water regulations.

BHIKHU SAMAT: It’s really a great way for us as a nation to look at what our goals are with water scarcity and climate change impacting us hugely. The recess is well overdue.

MARX: The water companies’ customers will hope any future changes could calm Britain’s troubled, sometimes dangerously dirty waters. For NPR News, I’m Willem Marx in Marlborough, England.

Accuracy and availability of NPR transcripts may vary. Transcript text may be revised to correct errors or match updates to audio. Audio on npr.org may be edited after its original broadcast or publication. The authoritative record of NPR’s programming is the audio record.

The 2025 Concacaf Gold Cup has wrapped up the group stage. Following three matches for each team, the knockout bracket is settled. The group stage consisted of 16 nations competing in four groups. The top two in each group advanced to the knockout bracket where they were seeded based on whether they finished first or second in their group.

2025 Gold Cup bracket

Final

Match 7: Mexico 2, United States 1

Semifinals

Match 5: United States 2, Guatemala 1 Match 6: Mexico 1, vs. Honduras 0

Quarterfinals

Match 1: United States 2, Costa Rica 2 (4-3 PKs) Match 2: Guatemala 1, Canada 1 (6-5 PKs) Match 3: Mexico 2, Saudi Arabia 0 Match 4: Honduras 1, Panama 1 (5-4 PKs)

Who has advanced

Group A: Mexico*, Costa Rica**

Group B: Canada*, Honduras**

Group C: Panama*, Guatemala**

Group D: United States*, Saudi Arabia**

*: Group winner **: Group runner-up

Costa Rica and Mexico were the first two nations to advance, with both claiming wins in their first two matches to eliminate the Dominican Republic and Suriname. Costa Rica and Mexico face off on June 22 with the winner claiming the group and the loser finishing as the runner-up. The United States followed in advancing after beating Saudi Arabia 1-0. They will clinch the group with a win or draw against Haiti. They have a six-goal lead on Saudi Arabia in goal differential (the first tiebreaker), which means they likely will clinch the group even with a loss to Haiti.

June 22 update: The US beat Haiti 2-1 to win Group D. Saudi Arabia played Trinidad & Tobago to a 1-1 draw, which clinched the Saudis second place in Group D and accompanying advancement to the knockout stage. Mexico and Costa Rica tied 0-0, which meant Mexico won the group and Costa Rica finished second due to the goal differential tiebreaker.

The United States and Canada are co-hosts of this year’s tournament. The United States and Mexico entered the tournament as co-favorites at FanDuel Sportsbook.

June 24 update: Panama beat Jamaica to clinch Group C. Guatemala beat Guadeloupe, which coupled with Jamaica’s loss secured Guatemala the second spot in the knockout bracket. Canada and Honduras won their final matches to secure first and second place in Group B, respectively.

For insurance producers, changing agencies might be as simple as signing a waiver. Other times, a producer changing agencies may leave the producer, agency officials, and even carriers with a legal maze of contracts, agreements, and state reports to navigate.

There’s a variety of reasons this is a tetchy subject—producers want free agency, carriers and agents need some degree of producer buy-in to maintain compliance and have a predictable distribution channel, everyone wants to retain commissions, states need accurate data on responsibility, and, somehow, consumers must be protected, as well.

Balancing these interests is no small feat. Let’s dig into the challenges of changing agencies, some practices stakeholders apply to mitigate issues in their distribution channels, and how modern hierarchy management can help carriers and agencies (but especially carriers) keep it all straight when they’re figuring out commissions.

Culture is also a factor. For many independent agents, the agency is as close as they get to having a built-out team. Having an agency that makes you feel like part of a team can be a serious differentiator. And, of course, some agencies have exclusive relationships with carriers to be the single retailer for certain products.

Whatever the reason, a producer who’s looking to change agencies but keep their carrier appointments will have some considerations before jumping ship.

What do carriers require when their appointed producers change agencies?

Carrier requirements for producers who change agencies vary greatly from carrier to carrier, and also depend on the states where the carrier has appointed the producer.

This may not be a significant issue if the new agency has a completely different set of carrier contracts than the previous one. But, if a producer’s new agency has a contract with their old carriers, it may be difficult to get going under the new agency contract.

Much of the drama in agency changes has to do with a producer’s previous book of business. Often, an agent will see changing agencies as an opportunity to review client coverage. But this can be a sticky wicket—is a producer helping a client upgrade their coverage and contract, or are they churning contracts for the sake of getting a first-year commission and adding the client to the new agency’s book of business?

We’re not here to impugn anyone’s honor; the reality is this situation presents a strong potential for conflict of interest. So, some carriers require producers to get signoff from a previous agency for any contracts they move over to the new agency. Frequently, that includes a form or other verification the agent has to fill out testifying that they explained the contract differences to the client.

Carriers often require a release from the previous agency, as well, verifying the status of the agent. This may be:

The agent is in an open relationship with both agencies—still able to sell through and earn trailing commissions from their old agency book of business while taking advantage of new opportunities with a new agency.

The agent may be terminating their relationship with the old agency and leaving that book of business in favor of an exclusive contract with the new agency.

The agent may be in what we’re going to call a “bad breakup,” where there are some disputes and the carrier will ultimately put them on a sort of probation, decline to allow them to write products through the new agency, or otherwise find a different path for this particular producer partnership.

Since a carrier provides products and is also cutting the check for commissions, being accountable for where the money goes is paramount.

Agency contract—new and old

If a producer doesn’t know what their current agency contract is, they’re gonna have a bad time. Some agency relationships are open—they’ll take what they can get, and if a producer has other lucrative options, they’re free to pursue them. Other agencies are pretty territorial and demand exclusivity for certain products or lines of authority.

Even within these requirements, agency relationships are not binary. Some agencies provide a tier of benefits based on a quota or have a contract with producers that mandates a producer write a certain amount of business to “buy out” the contract.

This means a producer might change to a new agency that has a contract with the same carrier as the old agency, but, if the producer owes the old agency a certain amount of submitted business, the carrier has to be in-the-know. To further complicate things, if the producer is writing through a downstream firm, the agency and carrier may have multiple levels of contracts to consider when cutting up the commissions check.

For agencies, while quotas and contracts are traditional methods for keeping a producer and their business locked in, another option is to keep the producer separate from the book of business from the get-go. So, agencies may employ producers as licensed-only agents or through other contractual relationships that mean the person making the sale isn’t necessarily servicing the consumer’s business.

Carriers and producers moving agencies

To bring the discussion back around to the role of carriers in this system, the issue of a producer changing agencies is tiresome. If the producer is an independent agent, they may want to be affiliated with multiple agencies. Or they may be exclusive to an agency but want to switch for reasons that could make a very real difference in their business and personal life.

Yet, for carriers trying to do their diligence in tracking producers for compliance’s sake, and tracking agency affiliations to effectively pay commissions to the right parties, this shifting structure can be a paperwork nightmare.

The difficulty of tracking and accurately reflecting agency hierarchies to pay out commissions or ensure you’re providing the right person with notices for contract changes isn’t just for carriers. Agencies that work with other firms and business entities up and down the compliance channel have the same needs to understand their complex distribution relationships.

How AgentSync helps when producers change agencies but not carriers: Hierarchy Management

When a producer changes agencies, every other agency or carrier that includes that producer in their hierarchies has a fire drill. From adding them to contracts to adjusting commission payouts to simply reflecting who’s responsible for whom in terms of DRLPs and direct reports, this data management work gets repeated over other systems and software.

AgentSync’s Hierarchy Management eliminates the drama by allowing your operations team to change the producer’s record to reflect their new status. With an API-driven modern solution, once that change is made, every instance of that producer’s data automatically realigns to reflect the new structure. No mistaken commissions payments, no repetitive data entry, no friction with old and new agencies.

Consider: You partner with a series of branch agencies under various doing-business-as relationships in one state while their parent agency is licensed as a resident business entity in a different state, all with downstream independent agent distributors. Mapping those relationships on paper begins to look like the mythical hydra. But with AgentSync Hierarchy Management, you can see who reports to whom and where, so you always know which producers and agencies are connected and in what way.

[Rewritten on July 5, 2025 after the new 2025 Trump tax law was passed.]

Because I’m self-employed and I’m under 65, I buy health insurance from a health insurance marketplace established under the Affordable Care Act (ACA). Every state has one. Some states run their own. Some states use the federal healthcare.gov platform. It’s for the self-employed, early retirees, and others who don’t get health insurance through an employer or a government program such as Medicaid or Medicare.

You may get a Premium Tax Credit (PTC) when you buy health insurance from an ACA marketplace. How much tax credit you get is based on your modified adjusted gross income (MAGI) relative to the Federal Poverty Level (FPL) for your household size. In general, the lower your MAGI is, the less you pay for health insurance net of the tax credit.

MAGI for ACA

Your MAGI for ACA is basically:

Your gross income;

minus pre-tax deductions from paychecks (401k, FSA, …)

minus above-the-line deductions, for example:

pre-tax traditional IRA contributions

HSA contributions

1/2 of self-employment tax

pre-tax contributions to SEP-IRA, solo 401k, or other retirement plans

self-employed health insurance deduction

student loan interest deduction

plus tax-exempt muni bond interest;

plus untaxed Social Security benefits.

Wages, 1099 income, rental income, interest, dividends, capital gains, pension, withdrawals from pre-tax traditional 401k and IRAs, and Roth conversions all go into the MAGI for ACA. Muni bond interest and untaxed Social Security benefits also count in the MAGI for ACA.

Tax-free withdrawals from Roth accounts don’t increase your MAGI for ACA.

Side note: There are many different definitions of MAGI for different purposes. These different MAGIs include and exclude different components. We’re only talking about the MAGI for ACA here.

2021-2025: 400% FPL Cliff Changed to a Slope

Your premium tax credit goes down as your MAGI increases. Up through the year 2020, the tax credit dropped to zero when your MAGI went above 400% of the Federal Poverty Level (FPL). If your MAGI was $1 above 400% of FPL, you would pay the full premium with zero tax credit.

Laws changed during COVID. This cliff became a slope for five years, from 2021 to 2025. The tax credit continued to drop as your MAGI increased, but it didn’t suddenly drop to zero when your income went $1 over the cliff.

Removing the cliff was a huge relief to people with an income higher than 400% of FPL ($81,760 in 2025 for a two-person household in the lower 48 states). The tax credit also became more generous during those five years at income levels below the cliff.

The Cliff Returns in 2026

The new 2025 Trump tax law — One Big Beautiful Bill Act — didn’t extend the slope treatment or the enhanced tax credit after 2025. The 400% FPL cliff is scheduled to return in 2026. The premium tax credit will also drop back to pre-COVID levels at incomes below 400% of FPL.

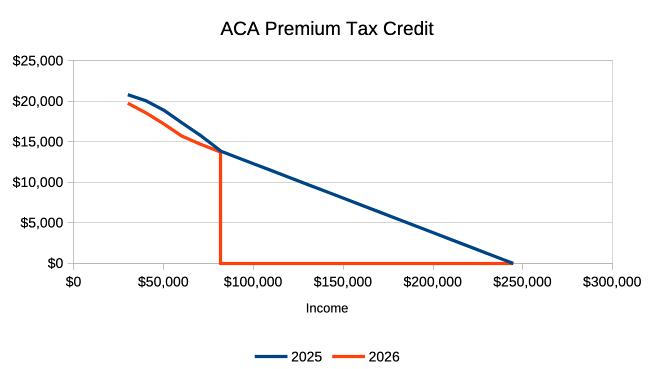

The chart above shows the ACA premium tax credit at different incomes for a sample household of two 55-year-olds in the lower 48 states. The blue line is for 2025, with the slope and the enhanced tax credit. The red line is for 2026, without the enhanced tax credit. The sharp vertical drop is the cliff.

How your premium tax credit will change in 2026 depends on where you are in the chart.

If your income is to the left of the cliff in the chart, your tax credit will drop slightly. It goes down from $18,900 to $17,200 at $50k income in this example. A $1,700 drop in the tax credit translates to an increase of about $140/month for health insurance.

If your income is to the far right in the chart, your tax credit will also drop, but you have the income to afford it. At $200,000 income in this example, the tax credit drops from $3,800 to $0, raising the cost for health insurance by a little over $300/month.

The drop is precipitous immediately to the right of the cliff. We’re talking about receiving over $13,000 in tax credit in 2025 versus $0 in 2026 for a two-person household with an income of $85k. How do you come up with an extra $13,000 for health insurance when your income is $85k?

The data for my example came from a calculator created by KFF. You can enter your specific zip code, household size, and age in this calculator to estimate how much your premium tax credit and your net health insurance premium will change.

Know Your Cliff

The chart I used as an example is for a two-person household. You also have a chart like this. The difference is where your red line drops to the X-axis. You must know first and foremost where the cliff is. The table below shows the 400% FPL cliff for different household sizes in 2026.

If your income is close to the cliff, you should manage it carefully to keep it from going over the cliff.

Manage Your Income

The most critical part is to project your income throughout the year and not to realize income willy-nilly before you do the projection. You can still adjust if you find your income is about to go over the cliff before you realize income. Many people are caught by surprise only when they do their taxes the following year. Your options are much more limited after the year is over.

If income from working will push your MAGI over the cliff, maybe work a little less to keep it under.

Tax-free withdrawals from Roth accounts don’t count as income.

Take a look at the MAGI definition. Minimize anything that raises your MAGI, and maximize everything that lowers your MAGI.

When you have self-employment income, you have the option to contribute to a pre-tax traditional 401k and IRA. Those pre-tax contributions lower your MAGI, which helps you stay under the 400% FPL cliff.

Choose a high-deductible plan and contribute the maximum to an HSA. The new 2025 Trump tax law made all Bronze plans from an ACA marketplace HSA-eligible starting in 2026.

On the other hand, Roth conversions, withdrawals from pre-tax accounts, and realizing capital gains increase your MAGI. You should be careful with doing those when you’re trying to stay under the 400% FPL cliff.

Accelerate Income to 2025

If you’re at risk of going over the cliff in 2026, consider accelerating some income to 2025 when the premium tax credit is still on a slope. If pulling income forward to 2025 helps you stay under the cliff in 2026, you lose much less in premium tax credit from your additional income in 2025 than the steep drop in 2026.

Borrowing

If your need for more cash is only temporary, consider borrowing instead of withdrawing from pre-tax accounts or realizing large capital gains. Spending borrowed money doesn’t count as income.

Instead of selling stocks and pushing yourself over the cliff by the realized capital gains when you buy a new car, take a low-APR car loan to stretch it out. HELOC and security-based lending are also good sources for borrowing.

You can repay the loan when you don’t need as much cash or when you no longer use ACA health insurance.

Income Bunching

If you can’t avoid going over the 400% FPL cliff, consider income bunching. When you’re already over the cliff, you might as well go over big. Withdraw more from pre-tax accounts or realize more capital gains and bank the money for future years.

Spending the banked money doesn’t count as income. Going over the cliff big time in one year may help you avoid going over again for multiple years.

100% and 138% FPL Cliff

There is another cliff on the low side, although that one is easily overcome if you have pre-tax retirement accounts.

To qualify for a premium subsidy for buying health insurance from the ACA exchange, you must have income above 100% of FPL. In states that expanded Medicaid, you must have your MAGI above 138% of FPL. This map from KFF shows which states expanded Medicaid and which states did not.

The minimum income requirement is checked only at the time of enrollment. Once you get in, you’re not punished if your income unexpectedly ends up below 100% or 138% of FPL. The new 2025 Trump tax law added requirements to Medicaid for reporting work and community engagement. You don’t want to have your income fall below 100% or 138% of FPL and be subject to those reporting requirements in Medicaid.

If you see your income is at risk of falling below 100% or 138% FPL, convert some money from your Traditional 401k or Traditional IRA to Roth. That’ll raise your income above 100% or 138% of FPL.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

More men across the United States – from tech CEOs in Silicon Valley to fitness-conscious fathers and retired executives – are seeking cosmetic treatments to maintain a fresh, confident appearance. While the rise in men’s grooming and skincare trends has already been well documented, there’s now a growing demand for more advanced facial rejuvenation options, including facelifts tailored specifically to male anatomy and goals.

This shift marks more than just a trend. It’s a modern revolution in self-care, confidence and proactive aging. Here’s a closer look at why more men are embracing facial rejuvenation and what’s driving this cultural transformation.

Confidence Goes Deeper Than Your Skin

For many men, facial rejuvenation is about alignment – the desire to ensure their outward appearance reflects the energy and vitality they still feel inside. In 2023, they made up 14.3% of all cosmetic surgical procedures worldwide, according to the International Society of Aesthetic Plastic Surgery – a noticeable rise from 13.5% just five years earlier. In the U.S. alone, men underwent over 1.1 million surgical and nonsurgical aesthetic procedures in 2020.

These numbers reflect a decisive cultural shift – more guys are choosing facial rejuvenation not out of vanity but to feel more like themselves again. Double Board-Certified Facial Plastic Surgeon at L&P Aesthetics Dr. David Lieberman explains, “Looking in the mirror each day and being proud of the reflection you see can impact how you carry yourself, how you engage with co-workers and friends, and ultimately how you feel on a deeper level.” In essence, when men feel good about how they look, they often feel better about every other part of their lives.

Modern Facelifts Are Designed For Men

Male-focused facelifts are not simply a version of the same procedure with a masculine label, they’re structurally different. Men have distinct facial anatomy, including thicker skin, denser facial hair follicles and a more angular bone structure.

As a result, modern facelifts for men focus on tightening the jawline, refining the neck area and subtly lifting without softening traditionally masculine features. At clinics like L&P Aesthetics in Palo Alto and Los Gatos, surgeons personalize each procedure to ensure the result looks natural, masculine and undetectable to the casual observer.

Discreet, Natural Results Are The Gold Standard

A desire for subtlety often drives men pursuing facial rejuvenation. They want to look refreshed, not drastically altered. That’s why techniques like the deep plane facelift are gaining traction. This method repositions deeper facial structures instead of simply tightening the skin, allowing for a longer-lasting and more natural result.

Competitive Environments Are Fueling Demand

In high-performance areas like Silicon Valley, youth and vitality are often perceived as professional assets. Many men feel pressured to stay relevant, especially when surrounded by younger colleagues or public-facing roles. A well-executed facelift can reinforce a sense of competence and energy in both boardrooms and digital workspaces.

Holistic Rejuvenation Is On The Rise

Facial rejuvenation isn’t a one-size-fits-all solution, and it’s rarely a one-procedure fix. Many men now pair facelifts with additional treatments like eyelid surgery, brow lifts, or injectables like Botox and dermal fillers to address the full spectrum of aging. The result is balanced, natural-looking enhancement across the entire face, with zero overdone features.

It’s Not About Vanity – It’s About Vitality

One of the most persistent misunderstandings about cosmetic procedures is that superficial desires drive them. In truth, many men seek facial rejuvenation to realign their appearance with their internal feelings. As they age, facial changes like sagging skin, hollow cheeks or deep creases can project fatigue, even if the individual feels energetic and sharp.

This mismatch can affect confidence, motivation and even one’s sense of identity. A successful facial rejuvenation procedure can reestablish that harmony, helping men feel more confident and reconnected with the version of themselves they recognize and value.

It’s A Private But Powerful Choice

Undergoing a facelift is not a decision most men make lightly. It’s personal, often private and incredibly empowering. For many, it marks a reclaiming of confidence and control – an affirmation of the right to care about their appearance without apology.

Male Facial Rejuvenation Is The New Normal

Facial rejuvenation is now part of a broader cultural shift. Men are embracing skincare, wellness and aesthetic procedures without shame. The result is better appearances, health, self-perception and quality of life.

Free NPI Lookup examined data from the Department of Health and Human Services and other sources to explore health care data breaches.

A wealth of information, including Social Security numbers, birth dates, and health insurance details; a reliance on systems connected to the internet; and weak protections. It’s easy to see why health care institutions are such enticing targets for hackers, and they are rising to the challenge.

In 2023, there were 725 large data breaches at hospitals and other organizations, breaking the record 720 breaches the year before, according to a January 2024 report from The HIPAA Journal. In addition, over 133 million records were compromised, more than double the number from the previous year. The problem has become so dire that more than 370,000 records were breached daily in 2023.

What makes health care so attractive to hackers? The stakes.

Should a hospital or other institution be the subject of a ransomware attack, where hackers disrupt operations until they receive a payoff or ransom—patients might suffer or even die. Think of delayed procedures, diverted ambulances, and electronic monitoring equipment going offline. The human cost makes agreeing to hacker demands tempting, even if the FBI advises against it, such as in the case of Change Healthcare, which allegedly paid $22 million in ransom, according to Wired.

Not only is the information valuable, but detection can take a while. As the HIPAA Journal noted, health care data can be used fraudulently for a long time before it is detected. Credit companies constantly monitor unusual spending patterns and can quickly close an account, but health care data cannot be changed so easily. It may also be bundled with other information and sold to identity thieves.

Free NPI Lookup

Hackers increasingly targeting health data

The HHS calls hacking and ransomware “the primary cyber-threats” to the health care sector. They are becoming more frequent and more sophisticated as the industry relies heavily on digital technology, whether electronic records, telehealth, internet-connected devices, or connections to insurance companies and vendors. Older equipment might be incompatible with security measures but too expensive to replace.

In 2023, ransomware attacks against the health care sector worldwide nearly doubled over the year before, according to the Office of the Director of National Intelligence. There were 389 victims in 2023 compared with 214 in 2022. Over the past five years, large breaches involving hacking increased 256% while ransomware shot up 264%, according to the HHS. Attacks can affect millions in one fell swoop.

Among the recent large breaches involved the Kaiser Foundation Health Plan and its 13.4 million members. What Kaiser Permanente described to TechCrunch as “online technologies” installed on its website and applications manifested into members’ searches being forwarded to the likes of Google, X (formerly Twitter), and Microsoft. No Social Security numbers, financial information, or credit card numbers were shared, the company told the Los Angeles Times, but IP addresses—which identify a particular computer—might have been.

Concentra Health Services, in contrast, affected about 4 million individuals, a third as many people as Kaiser Permanente’s breach. The company used a medical transcription company called Perry Johnson & Associates, which was hacked in 2023 and already compromised about 9 million at the time. Patient data divulged included names and addresses, birth dates, Social Security numbers, and other information.

A&A Services, which does business as Sav-Rx, appears to have paid a ransom when it was hit with ransomware, according to The HIPAA Journal. The journal based that assessment on the company’s statement that data taken from its system was destroyed. A&A Services, a pharmacy benefits management company based in Fremont, Nebraska, said it was able to get its systems running the next day with no delay in prescriptions.

Sometimes, not only health care companies but even the affected patients themselves are contacted, as was the case for INTEGRIS Health’s Oklahoma patients. Hackers emailed individuals directly and demanded $50 from each; otherwise, they threatened to sell the data on the dark web. To prove they actually had the data, the hackers included addresses, phone numbers, birth dates, and Social Security numbers in their emails.

ARMMY PICCA // Shutterstock

What’s being done to boost security?

The challenges facing the health care industry are significant. Health care breaches remain the most expensive across all industries, according to IBM’s 2024 Cost of a Data Breach report. The average cost of a health care data breach did fall over the last year, from $10.93 million in 2023 to $9.77 million in 2024, but that’s still twice as expensive as the average for all industries.

Critics in the industry say hospitals and other health care institutions are often far behind other sectors in boosting their cybersecurity, even with such simple steps as installing patches for known vulnerabilities. Moreover, financially strapped organizations may struggle to pay for cybersecurity professionals.

What is being done to help the industry tackle the problem? The HHS is trying new requirements balanced by voluntary measures and seeking funds to incentivize hospitals to meet cybersecurity goals. It has proposed rewriting the HIPPA rule—or the Health Insurance Portability and Accountability Act, which requires protecting patient information—to address cybersecurity. It could also tie Medicaid and Medicare funding to heightened cybersecurity, according to the Associated Press.

The Biden administration launched the Universal Patching and Remediation for Autonomous Defense, or UPGRADE, program, to create IT tools that can better fend off cyberattacks in hospitals. It also announced efforts from the private sector.

Microsoft has agreed to provide grants giving smaller organizations up to a 75% discount on security products and free cybersecurity training and assessments for eligible rural hospitals. Google will also provide advice for rural hospitals and nonprofits, as well as discounts for its suite of tools. In the meantime, New York proposed cybersecurity changes for its hospitals and allocating funds to help pay for the improvements.

No matter what, the efforts will need funds. Former health official Iliana Peters told The New York Times, “Without additional resources to raise the bar, those health care providers and those health care payers are going to continue to make choices to pay for treatment or for cybersecurity.”

Story editing by Carren Jao. Additional editing by Kelly Glass. Copy editing by Paris Close. Photo selection by Clarese Moller.

This story was produced by The Data Project and was produced and distributed in partnership with Stacker.

Recent efforts to curb federal spending – particularly massive proposed cuts to several major federal science agencies and numerous FEMA grant programs – drew concern from panelists at Triple-I’s Joint Industry Forum in Chicago.

Slated to lose around half of their original budgets, organizations like the National Oceanic and Atmospheric Administration (NOAA) and the National Science Foundation (NSF) provide insurers with much of the research data needed to model climate risks, at no cost to insurers nor the broader public. Abolishing this research, which also enables daily weather and natural disaster forecasting, will increase underwriting costs and those associated with various other industries, including transportation, agriculture, and energy.

“Federal science agencies probably facilitate more economic activity in the country than any other federal agency,” said Frank Nutter, president of the Reinsurance Association of America (RAA). “Fully funding and restaffing those agencies is pretty critical.”

A host of cancelled FEMA mitigation programs have left dozens of catastrophe-prone communities without aid – including projects that were approved before the cuts. Ending the Building Resilient Infrastructure and Communities (BRIC) program, for instance, rescinded approximately $882 million in climate resilience funding — “money we could have spent on mitigation, so we don’t have to spend so much after a disaster,” said Neil Alldredge, president and CEO of the National Association of Mutual Insurance Companies (NAMIC).

Nutter added that “weighing against safety, teacher salaries – all the kinds of things that communities grapple with,” most former grantees lack the resources for “risk reduction or municipal projects and infrastructure” without federal investment.

Population growth in high-risk areas exacerbates the issue, Alldredge said.

“If you look at a map of this country and the population changes from 1980 to today, we have moved the entire population to all the wrong places,” he explained. Building properties capable of withstanding these weather patterns – let alone insuring them – has launched the industry into “a new era of risk.”

While the panelists agreed that opportunities to improve FEMA operations exist, they questioned President Trump’s consideration to disband it entirely by shifting to a state-based relief system.

David Sampson, president and CEO of the American Property Casualty Insurance Association (APCIA), noted that “the very nature of a natural disaster means that it overwhelms the local entity’s ability to respond,” rendering any state-based solution “unworkable.”

“I think we as an industry know where the low-hanging fruit for reforms are,” Sampson continued, because “we interact with FEMA on the ground after disasters.”

State-level legislative momentum

Though the Trump administration’s current plans do not bode well for the future of disaster resilience, insurers celebrated many state legislative wins this year regarding tort reform, notably in Georgia and Louisiana.

“Even at the federal level, there is a growing sense of awareness of the negative impact that an out-of-control tort system is taking on the economy and the American consumer,” Sampson said, highlighting a new bill that would impose taxes on third-party litigation funding.

Florida also successfully resisted challenges to its 2023 and 2024 reforms, which have already helped stabilize the state’s insurance rates and attracted new insurers after a multi-year exodus. Charles Symington, president and CEO of the Independent Insurance Agents & Brokers of America, pointed out that industry advocacy is crucial to tort reform survival.

“Once you get these beneficial pieces of legislation passed,” he said, “we have to fight the fight in every legislative session.”

Symington then contrasted Florida’s recovering market with California’s enduringly hostile regulatory environment, propelled by the 1988 measure Proposition 103.

Insurance Commissioner Ricardo Lara has implemented a Sustainable Insurance Strategy to mitigate the effects of Prop 103 – such as by authorizing insurers to use catastrophe modeling if they agree to offer coverage in wildfire-prone areas – but the strategy has garnered criticism from legislators and consumer groups.

“California doesn’t have the assessment ability like Florida does,” agreed moderator Fred Karlinsky, shareholder and global chair of Greenberg Traurig, LLP. “California is three decades behind.”

As insurers adjust their risk appetite to reflect these constraints, more property owners have been pushed into California’s FAIR Plan – the state’s property insurer of last resort.

“Our members are having to cobble together coverage,” said Joel Wood, president and CEO of the Council of Insurance Agents & Brokers (CIAB), who noted that the FAIR plan’s policyholder count has more than doubled since 2020.

Natural disasters like January’s devastating wildfires underscore California’s need for premium rates that adequately reflect the full impact of these risks, which is essential to the continued availability of private insurance in the state.

“When you have the right leadership in place – the governor, the state legislature – and you have the industry being effective in our advocacy, then we can improve these difficult marketplaces,” Symington concluded.

Everyone has financial dreams—some are right around the corner, like taking a much-needed vacation or buying a new gadget. Others, like planning for your child’s education or retiring comfortably, take years of effort and planning. These aspirations, big or small, shape our financial goals.

But not all goals are created equal. To manage your money wisely and make real progress, it’s important to understand the difference between short-term and long-term financial goals. Each type serves a unique purpose and demands a different approach when it comes to saving and investing

In this blog, we’ll explore what are short term and long term goals, how to prioritize them, and why aligning them with the right investment strategy matters.

What Are Short Term and Long Term Goals?

Financial goals can be broadly categorized based on the time horizon required to achieve them. Here’s a simple breakdown of what are short term and long term goals:

Short-Term Financial Goals: These are goals you want to accomplish in the near future—typically within less than three years. They’re often essential, time-sensitive, and require liquidity.

Long-Term Financial Goals: These goals are set for the distant future, generally seven years or more. They usually involve significant life milestones and require long-term planning and disciplined investing.

Understanding the difference between short term and long term goals helps you plan your savings and investments accordingly.

Examples of Short-Term Financial Goals

Short-term goals are often immediate financial priorities that support your stability and security. Some common examples include:

Creating and maintaining an emergency fund

Paying off high-interest debt (like credit cards or personal loans)

Purchasing insurance (life, health, vehicle)

Planning a vacation within the next year

Buying a two-wheeler

Covering education fees or rent deposits

These goals are typically less capital-intensive but extremely important for your financial foundation. They require investments with high liquidity and low risk.

Examples of Long-Term Financial Goals

Long-term goals are generally centered around major life aspirations or commitments. Common long term financial goals include:

Saving for retirement

Funding a child’s higher education or wedding

Buying a home or repaying a long-term mortgage

Achieving financial independence or early retirement

Building a large corpus for a dream business or project

Since these goals have a long horizon, they allow you to take calculated risks and leverage the power of compounding.

Key Differences Between Short Term and Long Term Goals

Now that you know what are short term and long term goals, let’s look at how they differ in approach, planning, and execution.

Aspect

Short-Term Financial Goals

Long-Term Financial Goals

Time Frame

Less than 3 years

More than 7 years

Purpose

Manage immediate needs and stability

Achieve future aspirations and milestones

Urgency

High

Moderate to low (initially)

Risk Appetite

Low (to preserve capital)

Moderate to High (allows growth over time)

Investment Options

Liquid funds, fixed deposits, recurring deposits

Equity mutual funds, PPF, NPS, EPF, SIPs

Monitoring

Frequent

Periodic

Flexibility

More flexible

Less flexible (needs long-term commitment)

Understanding the difference between short term goal and long term goal helps you avoid using long-term investments for short-term needs or vice versa, which can derail your financial journey.

How to Prioritise Your Goals

Given the limited financial resources most people have, you can’t chase all goals simultaneously. Here’s a logical sequence to follow:

1. Clear High-Interest Debt

Before anything else, repay high-interest debt like credit cards. These eat into your savings and delay progress toward any goal.

2. Secure the Basics

Protect your family with term life insurance and health insurance. Then build an emergency fund worth 3-6 months of expenses. These are non-negotiable short term financial goals.

3. Fund Essential Short-Term Goals

Cover any immediate, time-bound needs such as rent advances, school fees, or planned vacations. These should be well-planned to avoid dipping into your long-term investments.

4. Start Investing in Long-Term Goals Early

Even if your primary focus is short-term, begin small investments toward long term financial goals like retirement or education. The earlier you start, the better you benefit from compounding.

How to Invest Based on Goal Type

Tailoring your investment strategy based on the goal duration is the key to success.

Prioritize growth over time through high-return instruments.

Investment avenues: Equity mutual funds (via SIPs), National Pension System (NPS), Public Provident Fund (PPF), Employees’ Provident Fund (EPF), stocks, long-term ETFs.

Remember, the difference between short term and long term goals also determines your risk appetite and investment product selection.

Common Mistakes to Avoid

Mixing Funds Across Goals Don’t use long-term funds for short-term needs—it disrupts compounding and might result in losses due to market volatility.

No Goal Clarity Not knowing the time horizon or exact requirement can lead to under-investing or investing in the wrong product.

Ignoring Inflation Especially for long term financial goals, not accounting for inflation can severely impact your corpus.

Starting Late The earlier you start with long-term goals, the less you’ll need to invest monthly. Delaying them makes the journey harder and more expensive.

Why Goal Categorisation Matters

Knowing the difference between short term and long term goals allows you to:

Allocate your funds better

Avoid unnecessary financial stress

Stay on track even during emergencies

Use appropriate investment tools

Maximize returns over time

At Fincart, we work closely with individuals to understand their financial aspirations and help them categorise, prioritize, and plan accordingly.

How Your Life Stage Influences Financial Goals

While time horizon is a key factor, your life stage also plays a crucial role in determining your financial goals—and how you approach them. The definition of short term financial goals or long term financial goals may vary depending on where you are in your journey.

Early Career (20s–30s)

This is the stage where individuals are just starting out with limited income and possibly education loans. At this stage:

Short-term goals include building an emergency fund, repaying student loans, or buying health insurance.

Long-term goals may start with retirement savings via EPF/NPS or a small SIP.

The key is to develop strong financial habits and avoid lifestyle inflation early on.

Mid-Career (30s–40s)

This stage brings higher income and greater responsibilities (family, children, EMIs).

Short-term goals include school fees, vacation funds, or insurance top-ups.

Long-term goals revolve around children’s education, homeownership, and retirement planning.

You should aim for a balanced portfolio and protect your assets with adequate insurance coverage.

Late Career (50s and above)

With major goals either met or nearing, the focus shifts to wealth preservation and health expenses.

Short-term goals may include travel, medical funds, or helping children start out.

Long-term goals now focus entirely on retirement income, estate planning, and financial freedom.

Understanding how your life stage influences your short and long term financial goals ensures that your planning remains relevant and efficient.

Blending Short and Long-Term Planning

You don’t have to wait to complete short-term goals before working on long-term ones. A blended approach often works best:

Allocate a higher percentage of income to short-term goals initially

Begin with small SIPs for long-term goals

As short-term goals get completed, divert freed-up money toward long-term investments

This method ensures that you stay prepared for today while securing your tomorrow.

How to Track and Adjust Financial Goals Over Time

Setting financial goals is not a one-time activity. It’s an evolving process that requires ongoing review. Markets change, incomes shift, priorities evolve—and your plan must reflect those changes.

Here’s how to effectively track and adapt:

1. Use Goal-Based Tools or Apps

Use platforms that allow you to assign values, time horizons, and track progress. Many robo-advisors offer visual dashboards that show how close you are to your targets.

2. Annual Review of Goals

Revisit your financial goals every year:

Has your income increased?

Have your expenses gone up?

Are there new goals to be added or existing ones to be updated?

Adjust your SIP amounts, rebalance your investments, or shift your allocations based on these insights.

3. Emergency Adjustments

Life is unpredictable. If an emergency arises, pause some low-priority goals and redirect funds to more pressing needs.

4. Celebrate Milestones

Achieving a goal—short-term or long-term—is a big deal. Reward yourself modestly. This reinforces positive financial behavior and keeps you motivated.

By actively tracking your financial progress, you’re more likely to succeed in fulfilling both your short and long-term ambitions.

The way forward

In summary, the difference between short term goal and long term goal lies in the time frame, purpose, risk profile, and investment strategy. Both are essential components of a solid financial plan. While short-term goals provide immediate security and stability, long-term goals help you achieve major life milestones.

By understanding what are short term and long term goals, and aligning your savings and investments with them, you can walk the path of financial wellness more confidently.

Whether you’re just starting your financial journey or looking to streamline existing goals, Fincart’s financial advisors can help you create a customized plan that balances your short-term needs and long-term dreams.